The world is at boiling point.

You might feel the same.

And in 1930, writing from a fascist prison cell in Italy, Antonio Gramsci described a condition that has become uncomfortably familiar:

‘The crisis consists precisely in the fact that the old is dying and the new cannot be born; in this interregnum a great variety of morbid symptoms appear.’

Nearly a century later, Gramsci’s words have begun to circulate again. It reflects how we feel reading the nightly news. From Ukraine, Iran, and Venezuela. To Epstein, Prince Andrew, and Trump.

You’ve probably encountered the bastardised version doing the rounds: ‘The old world is dying, and the new world struggles to be born: now is the time of monsters.’

It’s dramatic, evocative, and (I think) analytically useless.

The distinction matters. Monsters are inexplicable.

While supernatural manifestations shut down deeper inquiry. Morbid symptoms are clinical. They can be traced, diagnosed, and understood.

These differing framings determine whether the present moment is seen through a lazy lens of conspiracy or the deeper malaise of structural failure.

The global economy is in an interregnum. The old is dying.

Four decades of frictionless globalisation in which capital moved freely to the lowest-cost producer and goods flowed back without interruption — is in its twilight.

The new order, governed by physical constraint, strategic rivalry, and the reassertion of geography, has not yet consolidated.

Western institutions continue to operate under the assumptions of the old world. They apply financial remedies to physical problems. They interpret structural decay as cyclical disruption. They reach for the defibrillator when the patient’s organs were sold off years ago.

What follows is not a gape at monsters but a catalogue of morbid symptoms, and an attempt to understand what produced them.

The Two Ledgers

The central pathology of the current moment is a divergence between two systems of accounting that were once assumed to be the same.

|

The first is the Financial Ledger — The record of prices, credit, liquidity, and nominal wealth. It is the reality that governs central banks, equity markets, and corporate balance sheets.

In this ledger, the US dollar is king. Assets are fungible. Deficits can be financed. Problems are solved by adjusting interest rates, expanding credit, or restructuring debt.

The second is the Material Ledger — the record of physical reality. It tracks stockpiles, industrial capacity, energy density, skilled labour, logistics throughput, and chemical feedstocks.

For decades, these two ledgers have drifted apart together. Starting with the period economists call ‘The Great Moderation’.

With hindsight, it would be more accurate to call this period from 1980 to 2008 ‘The Great Financialisation’.

Under the banner of multilateralism came an era of IMF/World Bank-lead Globalisation under the ‘Washington Consensus’.

Capital could flow freely to wherever returns were highest, and goods could be sourced from wherever they were cheapest.

The ‘great moderation’ of inflation was largely thanks to the effective doubling of the labour pool. The fall of the Soviet system and the economic liberalisation of Asia brought 1.5 billion workers into the system over 15 years.

The taming of structural inflation led to the great US bull market of 1982, cementing the US dollar as the world’s reserve currency.

With global trade booming and inflation low, physical assets lost their lustre. Instead of saving in physical assets, like gold, central banks turned to the US.

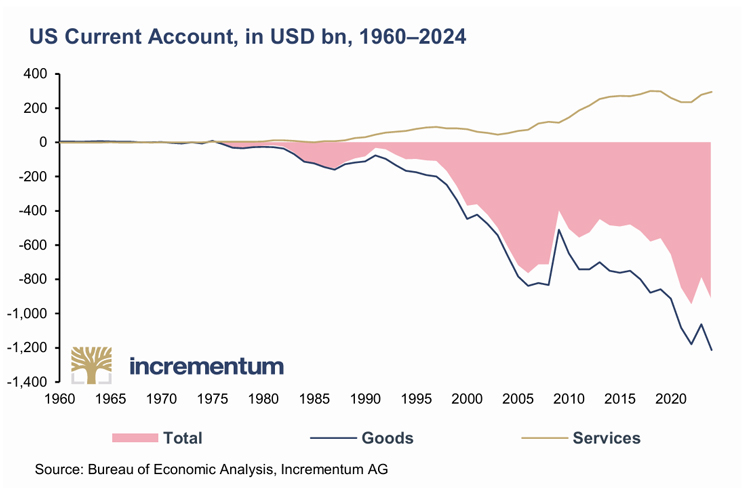

Asian and petro-state current account surpluses were recycled into US Treasuries and Western financial products.

This ‘exorbitant privilege’, allowed the US to run an ever-growing trade and current account deficit which facilitated the massive inflow of cheap goods.

Source: Incrementum

[Click to open in a new window]

Thus, the financial ledger grew in power over the material ledger.

Money bought matter with minimal friction. In fact, it was so reliable that the distinction between the two ledgers ceased to be meaningful.

Financial depth became a proxy for productive power. GDP was treated as equivalent to capacity. Market capitalisation was confused with strategic capability.

That decoupling between the material and financial ledger is now ending.

The divergence between the monetary and physical economies is now stretched.

And the physical economy is powering ahead – what’s happening in Iran right now proves the point.

This is exactly what my colleague Lachlann Tierney is talking about in his new investment thesis.

It’s called Pax Silica. Click here to view his presentation.

Tomorrow, I dive deeper into what happens when the Material Ledger takes the reins of markets.

Regards,

Charlie Ormond,

ATLAS and Altucher’s Investment Network Australia

Comments