There’s a long-held view in the world of finance that a flurry of business activity in the form of mergers and acquisitions, affectionately known as M&As, often mark the top of a long-drawn-out bull market.

It’s a signal that traders and savvy fund managers sometimes use to determine a market tipping toward the edge of being dangerously overvalued.

A phase in the business cycle that calls for discipline.

However, for the majority, M&A activity is usually a trap that pulls investors in at just the wrong time.

Directors, CEOs, and executives are equally vulnerable as the small-time investor when it comes to poorly timed investments.

FOMO is a powerful force across the business arena.

And in the corporate world the stakes are far, far greater when it comes to buying at the top.

The curse of the multibillion-dollar write-offs

I’d like to share with you an example from the tech world so we can relate this to where we sit in the upcoming commodity boom.

Buying at the top of a market has become the fabled legacy for many a prominent CEO.

He (or she) who decided to go ‘all-in’ at precisely the wrong moment will hold that stain for the remainder of their corporate career.

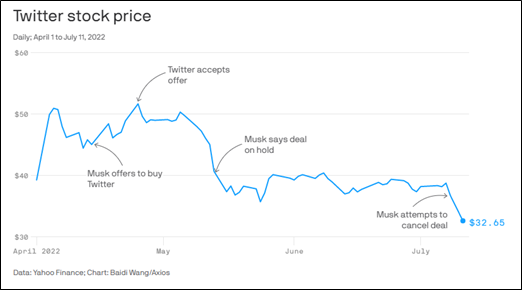

And in recent times there’s been no better example than the US$44 billion takeover of Twitter.

On 14 April, Tesla CEO Elon Musk offered a 38% premium to Twitter’s 1 April closing price.

And just nine days later, in his usual self-publicised style, Musk triumphantly ‘tweeted’ the deal had gone through with the Twitter board unanimously accepting his offer.

However, humility soon took hold…

On the backdrop of a Ukrainian crisis and rising interest rates, Twitter’s share price fell hard.

Adding weight to this was an industry that was starting to flounder as investors started to feel the pinch of holding overvalued assets that sat somewhere ‘in the cloud’.

Reality was starting to bite.

Buying for ‘future’ momentous profits was no longer a sound strategy.

And, as Twitter continued to fall, Musk attempted to scramble his way out of the takeover.

The chart below neatly summarises the events that took place against the Twitter share price, from April to July of this year:

|

|

| Source: Yahoo! Finance |

Right now, the deal sits with the US courts as Musk tries to disassemble the mess.

But the tech giant billionaire certainly isn’t alone in his poorly timed acquisition.

And stunningly, it’s one of the most trusted computer brands we’ve all relied upon at some point that seems to have completely dropped the ball.

In January 2022, Microsoft agreed to buy a gaming company called Activision Blizzard for a staggering US$68.7 billion!

This was Microsoft’s largest deal ever.

And there’s no backing out like a regular investor.

Once the contract is signed, the deal is done.

Is this the end for tech?

Major tech buyouts have been a theme throughout 2021 and 2022.

So does this mark a top for this six-year-plus bull market?

Perhaps.

Recent market events are only adding to this outlook.

A repeat of the 2000 dotcom bust is certainly on the cards.

I’m sure the board at Microsoft will be holding on for dear life over the coming months.

The chart below, if it plays out, will be the stuff of nightmares for years to come for tech CEOs.

Major company buyouts are a sure sign that things are about to turn ugly…

Monthly Chart NASDAQ-100 Technology Sector Index

|

|

| Source: ProRealTime Charts |

Mining suffered the same fate a little more than 10 years ago

Step back in time to the last commodity boom, and you may remember multibillion-dollar buyouts happening virtually every single month amongst the major mining companies.

This was most prolific around the peak from 2010–11.

Companies were aggressively out-bidding each other on $20, $30 billion deals!

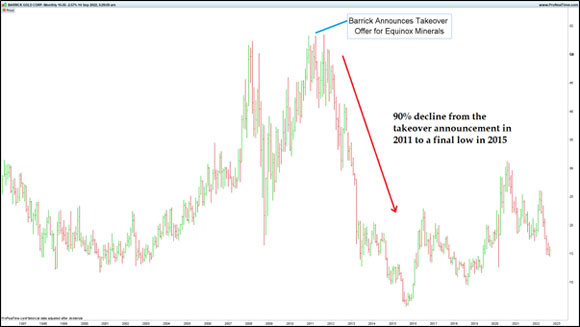

I sat in the middle of this action as a geologist working for one of the darlings during this time, Equinox Minerals.

Equinox was an Australian-owned copper producer operating in Zambia that grew from a penny stock in the early 2000s to a $7 billion giant.

Was it worth $7 billion?

Well, in 2011, Barrick Gold thought so.

Barrick was the world’s largest gold producer at the time.

Despite teams of in-house analysts, accounts, lawyers, and economists, the company had little idea it was making a major acquisition at the very peak of the market.

The company was left reeling after the asset it purchased underwent a $6 billion write-off little more than 12 months after the deal went through.

As so often is the case in frenzied corporate FOMO, proper due diligence was replaced with getting the deal done at all costs.

And the deal certainly got done.

While Equinox shareholders rode off into the sunset, Barrick managers and executives were left shaking their heads.

They simply couldn’t comprehend how they got it so wrong.

The CEO was fired.

Barrick never recovered from this ordeal, as the chart below illustrates…

Monthly Chart Barrick Gold [NYSE:GOLD]

|

|

| Source: ProRealTime Charts |

What was once the world’s largest gold miner now languishes in the background as a relatively insignificant minnow.

I was able to witness, first-hand, one of the costliest of all corporate stuff-ups, buying at the very peak of a multiyear bull market.

It showed me how companies are just as likely to do this as the everyday investor.

The Barrick example was just one of many at the time…

In 2010, Rio Tinto acquired Riversdale Mining for around $3.7 billion.

Three years later it disposed the asset for about 2% of the purchase price!

Again, in 2011, Rio Tinto continued to buy into the market euphoria and purchased a company called Coal & Allied Industries.

Later selling it for about a third of the original price.

While in 2012, Glencore, another major in the industry, agreed to buy Xstrata for a blowout figure totalling more than $38 billion.

This was one of the biggest deals ever in mining at the time.

Less than 12 months later, Glencore published its first results from the merger announcing that it had taken a $7.6 billion write-down.

The list is endless.

The Financial Review, looking back on the transactions that took place over that crazy period, neatly summarises:

‘Unfortunately, mining industry executives have a tendency to lose their sense of perspective and judgement when confronted with the prolific cash flows generated in the up cycles in commodities.’

Indeed, they do.

Which is why we need to be on our guard as investors.

M&A activity in mining — are the cracks starting to show?

We can use these lessons to guide our future investing.

M&A activity gives us one such tool.

If you’ve been reading the news of late, you may have noticed that BHP recently made a bid for the South Australian-based copper producer, Oz Minerals.

It was bringing the ‘A’ back into M&A activity.

Something the industry hasn’t seen much of, of late.

But is this a cause for concern?

Not really.

The recent BHP deal was a conservative attempt to strategically merge the Olympic Dam infrastructure with OZ Minerals’ nearby copper-gold deposits.

In other words, it made logistical sense based on sound perspective and reasoning by the BHP board.

In fact, it’s a positive sign, while still tempered, that we are seeing some M&A activity brewing in the sector.

The feeling on the ground is buoyant but nowhere near the euphoria of 2010 and 2011.

This is YOUR opportunity to ride the next major bull market.

I’ll have more to say about that next week…

Until then,

|

|

James Cooper,

Editor, The Daily Reckoning Australia