In today’s Money Morning…cash versus profit: the academic debate…earnings metrics versus cash flow…the importance of systematic analysis…and more…

‘Cash is a fact, profit is an opinion.’

Alfred Rappaport

‘Our ultimate financial measure, and the one we most want to drive over the long-term, is free cash flow per share.’

Jeff Bezos

‘It is much easier for investors to utilise historic P/E ratios or for managers to utilise historic business valuation yardsticks than it is for either group to rethink their premises daily.’

Warren Buffett

The reporting season is well underway.

And as company after company lines up to release its accounts, investors are confronted with the perennial question — profit or cash?

More specifically, when analysing a firm’s performance, what’s more important as a metric — a firm’s reported profit or its cash flows?

As companies continue to release their full-year results, attention gravitates towards the bottom line of the income statement.

Has this firm made a profit? Have its earnings grown? Is the profit margin healthy?

Less attention is paid to cash. How much cash is the firm generating from operations? Is it free cash flow positive?

Cash versus profit: the academic debate

Analysts and finance scholars have debated the usefulness of cash over profit for years.

Back in 1998, Alfred Rappaport, in his book Creating Shareholder Value, proclaimed that ‘Cash is a fact, profit is an opinion’.

Rappaport argued that cash is harder to massage than accounting profit, which relies on accounting conventions and assumptions more prone to adjustment.

This can lead to major discrepancies between reported profit and reported cash flow.

In a research note, respected financial analyst Michael Mauboussin wrote that the difference between earnings and cash flow is ‘significant’.

Studying Dow Jones Industrial Average data, Mauboussin and colleagues found:

‘The range of cash flow/earnings ratio within the DJIA fluctuated from negative 0.08 to positive 2.6.

‘This means that earnings and P/E comparisons can be highly misleading because they do not offer insight into a business’s underlying economics.’

Earnings metrics versus cash flow

A key argument in favour of prioritising the analysis of cash flows over earnings is the fundamental valuation principle that a business is worth the present value of its expected future free cash flows.

But while market participants may remember the valuation theory that places importance on discounting future cash flows rather than earnings, it is earnings that dominate the discussion.

Earnings per share and price-to-earnings are ubiquitous metrics — widely shared and frequently communicated.

But earnings metrics are flawed, especially if we use them as shorthand for assessing value.

As Stephen Penman wrote in Accounting for Value, when we ‘calculate value to challenge price, beware of using price in the calculation.’

Relatedly, earnings metrics could also mislead us into thinking a business is sound and improving.

Earnings growth is not always a good thing.

As Mauboussin explained in a piece for the Harvard Business Review:

‘EPS growth is good for a company that earns high returns on invested capital, neutral for a company with returns equal to the cost of capital, and bad for companies with returns below the cost of capital. Despite this, many companies slavishly seek to deliver EPS growth, even at the expense of value creation.

‘Theory and empirical research tell us that the causal relationship between EPS growth and value creation is tenuous at best. Similar research reveals that sales growth also has a shaky connection to shareholder value.’

A worked-through example of Mauboussin’s point can be found in a shareholder letter penned by none other than Jeff Bezos.

In his time helming Amazon, Bezos advocated free cash flow per share as the defining metric of Amazon’s financial performance.

Echoing Mauboussin, Bezos noted:

‘Though some may find it counterintuitive, a company can actually impair shareholder value in certain circumstances by growing earnings. This happens when the capital investments required for growth exceed the present value of the cash flow derived from those investments.’

You can read Bezos’s example in depth here.

Elsewhere, in a research note for investment bank Credit Suisse, Mauboussin affirmed Amazon’s valuation methodology, arguing investors should think harder about future cash flows:

‘Investors must focus on the key value drivers and the resulting cash flow a business generates to identify investment opportunities.’

Harder to do than playing around with earnings multiples but closer to the heart of the matter.

Investment metrics should not confer value on a business. Instead, investment metrics should reflect a business’s underlying and future performance.

Metrics are derivative, not determinative.

After all, as Penman further elaborated in his book:

‘Value, and indeed risk, lies in the businesses that make up the market portfolio, so examine those businesses. One does not buy a stock, one buys a business and when buying a business, know the business.’

That said, while many studying the financial sector prefer focusing on cash flows to determine value, cash flows are now immune to manipulation.

While advocates of cash flow argue earnings can all too often be smoothed, adjusted, and managed — giving rise to the quip that profit is opinion, cash is fact — cash flow can fall victim to financial massage, too.

Accounting professor Baruch Lev, in his 2016 book The End of Accounting, had some bad news:

‘Although the ending balance in cash and the change in cash from one period to the next are not readily subject to manipulation, the components of total cash flow, the operating, investing, and financing amounts are more susceptible to management…

‘Free cash flow is generally defined as operating cash flow minus capital expenditures and, for companies that pay them, preferred dividends. Thus, while analysts, investors, and creditors might be led to believe that operating cash flow and free cash flow are somehow above the creative accounting fray, that belief is unfounded. Operating cash flow and free cash flow are subject to manipulation, which, unfortunately, occurs often.’

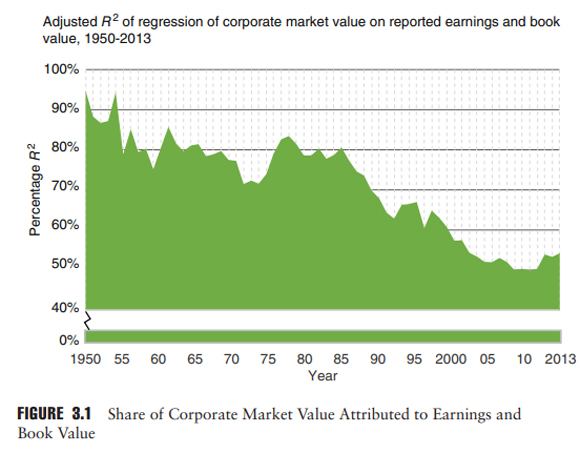

It’s likely that the corrosion of the reliability of both earnings and cash flow has led to a declining correlation between financial statement information and stock performance.

In Baruch Lev’s book on the state of modern accounting, Lev reported that the relevance of corporate financial information to investors fell from 90% to around 50% in the past 60 years:

|

|

| Source: Baruch Lev, 2016 |

The importance of systematic analysis

Imagine a visit to the doctor after you have done thorough blood work and other tests.

You wait nervously to hear the doctor’s interpretation of the data.

Instead, the doctor simply grunts, ‘Your cholesterol level is 195. Good enough. Next patient.’

Perplexed and peeved, you storm off.

Clearly, you wanted the doctor’s assessment to involve more than just one number. How can one figure explain my overall well-being?

But that, in a nutshell, is what many investors do with stocks, argues accounting professor Lev.

We often focus on a single indicator, thinking it can tell us all we need to know about the current and future performance of a stock.

But just as a terse doctor’s visit would leave us wanting, so too should only one metric leave us wanting more insight.

In the end, there is no magic number or metric.

And even though cash flows are vital in coming to a business’s long-term value, calculating future cash flows involves plenty of thought, analysis, and number crunching — no magic number here.

As Lev concluded:

‘Analysing a complex, often global business organisation, subject to competition and fast-changing technologies, requires a comprehensive system of well-integrated indicators and contextual information. It’s a mosaic; no shortcuts.’

Good investing involves no shortcuts.

Regards,

Kiryll Prakapenka,

For Money Morning