It’s getting late in April, and Q1 hedge fund letters are starting to land.

Read enough of them back-to-back, and they start to blur. The correspondence reads like a support group meeting.

Fund managers with different mandates and strategies all arriving at the same place — an apology.

Each explained, with only slightly different adjectives, how their overweight AI bets had been weighed down by the heavier burden of bad news.

The numbers back them up. Global hedge funds posted their worst monthly drawdown since January 2022 this quarter.

The S&P 500 fell close to 10% from its January peak by late March. The AI trade, which had carried three consecutive years of strong returns, suddenly had no one in the passenger seat.

Then, before the ink was dry, the whole thing reversed.

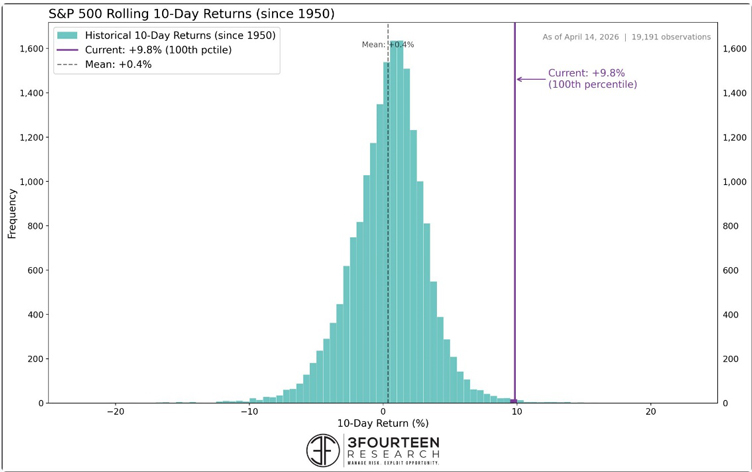

Yet another V-shaped buy-the-dip recovery. The round-trip from correction territory was among the quickest on record.

The S&P 500 rose in 13 of 16 trading sessions through April so far, putting on more than 12% and surging to fresh record highs.

That puts this run in the 99.8th percentile of gains going back to 1950.

Source: 3Fourteen Research

[Click to open in a new window]

The ASX 200 has somewhat tagged along for the ride. Local super balances are happily back in the black.

So the ‘smart money’ mea culpa letters read strangely now.

It’s as if the hedge funds are saying sorry because the market zombie just keeps getting back up and charging up the charts.

They don’t even know how it’s possible…

A post-mortem of a body that got up and walked back up the stairs.

The Bulls and the Bears

Both Have Receipts

It is hard to remember a moment when each side of the argument had such a compelling case to make.

Bulls can point to the numbers:

- Early US Q1 earnings are running ahead of consensus

- The Fed will soon have ‘market-friendly’ leadership

- US unemployment is low

- Global liquidity is on the rise

- Capex into AI keeps flowing

Anyone who bought the dips since 2022 is richer for it.

Bears have their own version of events. Valuations on the S&P sit stretched against almost every historical yardstick.

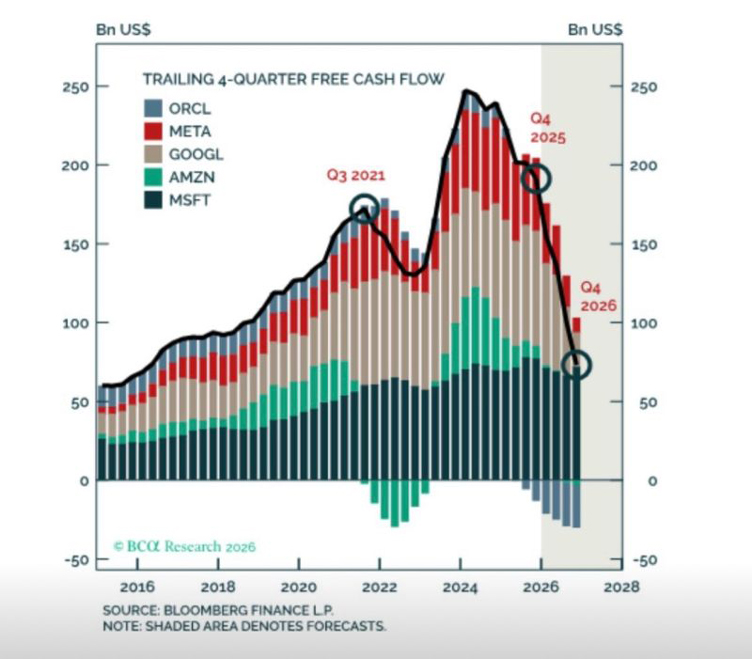

Big tech’s capital spending is eating into its free cash flows at a rate comparable only to late-1990s telcos.

Source: Bloomberg

[Click to open in a new window]

The Strait of Hormuz is an ‘on-and-off’ faucet in the media, and a slow drip in reality.

Oil is no longer approaching the crunch point — it’s arrived.

All while private credit continues to reel amid low investor confidence. Big banks are now trading credit default swaps, betting against the largest private credit funds.

And to top it off, we have a US president who treats trade policy like a hostage negotiation, and war negotiations like a campaign rally.

Both sides have good points. But neither explains why the market is subject to such violent moves.

The missing variable isn’t fundamentals. It’s market structure.

An Ackman Answer

So far, the best explanation I have seen for this moment comes from billionaire investor Bill Ackman’s Pershing Square Holdings, letter to shareholders back in 2024 (full letter here).

Here, the blame is laid at the feet of the growing share of passive traders — and the leveraged traders it leaves to dominate price action:

‘We believe that the growing index ownership as a percentage of stock market float has increased the impact that short-term, highly leveraged investors can have on price discovery, as they now comprise a growing percentage of the market cap and daily trading of companies…

…As highly leveraged market participants, these investors’ tolerance for mark-to-market losses is small, which contributes to stock price volatility as they can become effectively forced sellers when companies disappoint, even in the short term…

This phenomenon of massive short-term volatility in even the largest, most well-capitalized and most closely followed companies has only increased over the last two years.

As a result, the stock market at times feels ‘broken;’ that is, stocks can trade in, what appears to us, a completely irrational fashion in the short term when a company fails to meet and/or exceed analysts’ or investors’ expectations…

The market increasingly appears like a casino where money is wagered over the course of a day, hours, minutes or even seconds.’

What this leaves you with

In broad portfolio-wide terms, there are three reasonable responses to a market like this one for the longer term.

The first is to close your eyes and buy. Dollar-cost average into a well-balanced portfolio or a broad ETF. Ignore the noise and trust the compounding.

Optimists would rightly point out that history has rewarded this more often than not. Although I’d caveat that I’m personally sceptical of this strategy when I feel like we’re nearing a new market regime.

The second is to step down the risk curve or sit on your hands. Cash pays around 4.5% and a little better in term deposits.

HALO stocks are another ‘low risk’ strategy that’s captured attention this year.

Heavy Assets, Low Obsolescence.

That means owning ‘old economy’ stocks that combine large amounts of physical capital with long-lived economic relevance. Think utilities, airlines, mining, energy.

The third is to engineer a hedge. This is mostly institutional territory, or those with a deeper grasp of options. Most quietly underperform, waiting for some big event, but can offer some insurance.

I’d say this moment of confusion offers you permission to hold a “boring” portfolio.

Franking credits, a respectable yield, and a basket of commodities should do.

If the market’s own signals aren’t giving you a clear view, the most honest trade is the one that does not require one.

Having a second opinion on a trade can be invaluable in a moment like this.

If you have a stock in mind, but you’re unsure if it’s the right time, the decision can be agonising.

We’ve heard your requests here at Fat Tail and have opened a new service called Murray’s Trading Room.

Submit a stock you are looking at and get live feedback from chief trader here at Fat Tail Investment Research, Murray Dawes.

With his veteran insight you can feel secure about knowing when to get in — or out of your trades.

Regards,

Charlie Ormond,

ATLAS and Altucher’s Investment Network Australia

Comments