The Strait of Hormuz is just 33 kilometres wide at its narrowest point. Right now, it’s the most dangerous stretch of water on the planet.

Since US and Israeli strikes on Iran last Saturday, the Strait has shifted from the world’s busiest energy highway to a no-go zone.

Around 200 tankers are now stranded. At least five have been hit by Iran. Two crew members are dead. One tanker is still on fire.

On Monday, Iran’s Revolutionary Guard declared the Strait ‘closed’, warning that any vessel attempting to pass would be ‘set ablaze’.

The US responded in turn by sinking 11 ships and claiming Iran’s navy is all but gone from the Gulf.

But you don’t need a navy to shut a shipping lane. You just need to make it uninsurable.

Premiums have spiked from 0.2% to 1% of a vessel’s value, adding between US$375k and US$1 million per voyage. Without insurance, the route has ground to a halt.

Conflict in the region usually means one thing for markets: Oil prices.

The Strait of Hormuz carries roughly one-fifth of the world’s seaborne oil. That’s around 20 million barrels per day.

Source: AA

[Click to open in a new window]

But oil is only half the story. The bigger risk may be gas. LNG.

If the disruption proves temporary, markets can absorb it.

If it extends into weeks or months, we’re talking about something far more serious.

LNG’s Biggest Disruption in Half a Century

Qatar is the world’s second-largest LNG exporter. It shipped around 83 million tonnes last year. Nearly all of it leaves the Strait from the massive Ras Laffan complex.

On Monday, QatarEnergy shut the entire complex down after Iranian strikes.

Two Shahed drones — costing roughly US$30,000 each — have taken about 20% of global LNG supply offline in a single day.

The US and allies may hold the waters, but the risk from the skies could take much longer to solve. For now, shipping is on ice.

Source: Westpac | Martin Whetton

[Click to open in a new window]

Oil is up 13% since Saturday. Gas prices in Europe have jumped 50% amid low inventories after a harsh winter.

As of this morning, Asian gas prices are up 40%, but many are bracing for a violent reprice once inventories run lower.

If this crisis rolls into months, the pain could soon be at our doorstep.

Unlike Saudi oil, which can be partially rerouted via pipeline, Qatari gas has little alternative. And the threat of further Iranian strikes on Gulf energy infrastructure is real and ongoing, even if no navy stands against US forces.

This is the new reality in the age of drone warfare.

Low-cost drones have caused the largest disruption to global LNG infrastructure since the 1973 oil crisis reshaped energy markets.

And here’s where it becomes a broader economic issue.

Who Gets Hurt

Asia takes the first punch. More than four-fifths of Qatar’s LNG exports go to Asia.

Source: Bloomberg

Taiwan generates over 40% of its electricity from LNG and sources a third of its supply from Qatar.

Japan and South Korea are currently scrambling for spot cargoes. India is already talking about rationing gas.

Europe won’t be far behind. Since Russia’s invasion of Ukraine, land-based pipeline gas flows to the continent have effectively ended.

Since then, Europe has become deeply reliant on seaborne LNG. About a quarter of Europe’s gas supply now arrives as LNG.

There are alternative sources. The US is the world’s largest LNG exporter, and Australia has significant capacity.

But you cannot replace 20% of the global gas market overnight. There simply isn’t enough spare capacity or shipping to absorb a shock of this magnitude.

Energy → Food → Inflation

Natural gas isn’t just fuel. It’s the primary feedstock for ammonia and nitrogen fertiliser production globally.

Around one-third of internationally traded urea passes through the Strait of Hormuz. If we include LNG’s final use at its destination, that number exceeds 50%.

A sustained Qatari shutdown will see fertiliser prices double from here. That feeds directly into agricultural production costs. Then into food prices. Then into CPI prints.

The lag is typically six to nine months from energy shock to supermarket shelf.

We saw this back in 2022–23. After Russia invaded Ukraine, European fertiliser plants shut down, and food security became a buzzword in European capitals.

Urea was up 14% yesterday. Could we be about to see that green gap below filled?

Source: TradingEconomics

[Click to open in a new window]

For Australia, the situation isn’t much better. We’re still getting over the hangover of the 2022–23 energy crisis.

Back then, Australian household gas and electricity prices jumped 27% and 43% respectively. The government spent billions on subsidies to cushion the blow.

Our latest inflation reports show just how much we’re struggling to contain costs as those 2023 energy rebates roll off.

Now it looks like we’re back to square one. A major supplier knocked offline. Fragile supply chains. And central banks in a bind.

A renewed energy shock could further push out rate-cut cycles and prolong restrictive monetary policy.

Gold’s hefty fall yesterday reflects exactly this fear. The longer this situation drags on, the later those interest rate cuts may be.

Australian Opportunity

This is where some positive opportunities for Australia enter.

Australia is one of the world’s largest LNG exporters, with major projects in Western Australia and Queensland supplying Japan, Korea and China.

If Middle Eastern supply stays impaired, Australian LNG becomes a critical swing supply into Asia.

Long-term contract volumes would hold, but spot cargoes could see much higher prices.

On the ASX, that directly benefits LNG-exposed producers such as Woodside Energy and Santos.

LNG infrastructure operators and shipping providers could also see improved margins. Flex LNG on the NYSE has historically been a winner in these moments.

Many US LNG exporters are already moving on expectations of higher prices and diversion flows toward Europe and Asia.

But freight constraints could favour our companies as closer suppliers to Asia.

There are caveats. Much of Australia’s LNG is largely contracted under long-term agreements. A lot of upside depends on spot exposure.

Of the two, Woodside, with its higher uncontracted volumes, seems to have greater leverage to spot prices for this moment.

However, domestic policy risk also lingers in the background here. If energy prices spike, the government may have to step in to ensure more local gas supply if this drags.

Still, in a world where 20% of global LNG trade is at risk, a secure Pacific supply becomes strategic.

In the end, if the Strait of Hormuz disruption lasts only a few more days, markets will shrug it off.

If it lasts months, we are looking at the largest structural shock to LNG markets in decades. With second-round effects on fertiliser, food prices and inflation globally.

This isn’t just about oil hitting US$100. It is about whether energy becomes the inflation story of 2026.

Regards,

Charlie Ormond,

Small-Cap Systems and Altucher’s Investment Network Australia

***

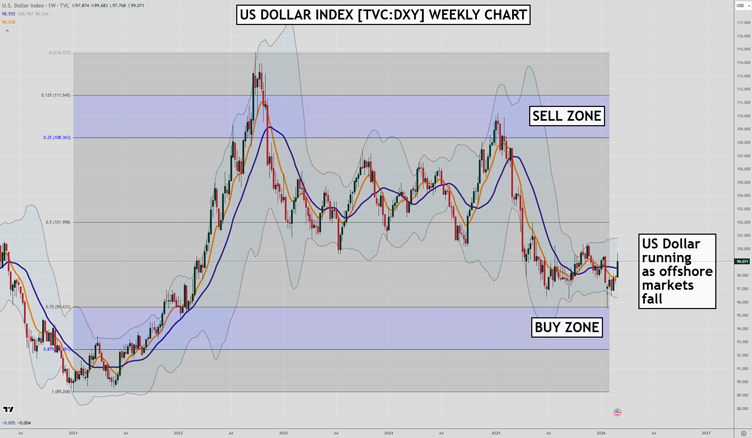

Murray’s Chart of the Day – US Dollar Index

Source: TradingView

Last night Trump announced he would cover insurance for vessels braving the Strait of Hormuz.

The S&P 500 was down nearly 200 points prior to Trumps announcement. Then stocks rallied into the close, falling just 65 points on the day.

But the S&P/ASX 200 [ASX:XJO] didn’t get the memo, and we opened our trading day down a whopping 140 points (1.5%).

The German Dax fell 3.5% and the South Korean Kospi index dropped a massive 7% in their day session yesterday.

Meanwhile the US dollar is spiking.

I think investors are repatriating money back to America while risk levels remain high in the early days of the Iran war.

Oil prices continue to rise and spiked above my US$83 line in the sand for Brent crude oil last night. But it fell below that level by the close on the back of Trumps insurance announcement.

So the oil market is now flirting with danger and a move towards US$93 isn’t out of the question in coming days.

Everything hinges on the war of course, and that is impossible to predict.

The highest odds are that things calm down over the next month or so. But there is still a chance things continue to deteriorate before they get better.

You can see in the chart above that the US dollar has bounced from the top of the buy zone of the last five years trading.

If we see the US Dollar heading above 101.00 (currently 99.17), there is a chance we see a sharp spike towards 103.00. That could make it difficult for commodities to continue their rally, and gold and silver would probably see another correction unfold.

Regards,

Murray Dawes,

Retirement Trader and International Stock Trader

Comments