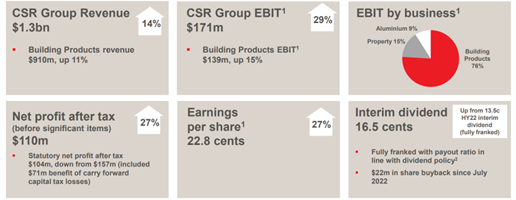

Building products supplier CSR Ltd [ASX:CSR] reported a 27% increase in after tax net profit for the 2022 financial half, totalling $110 million.

Trading revenue was also up 14%, bringing in a total of $1.3 billion, while EBIT came to $171 million, another increase of 29%.

CSR shares are down 20% year to date.

Source: Trading View

CSR’s half-year results

On Friday, the building supplier reported solid results over the past six months ending 30 September 2022.

Highlights included a 27% increase in net profit after tax compared to the same time in 2021, a total of $110 million.

CSR reported statutory net profit (after tax) totalled $104 million, including revenue from the company’s software-as-a-service segment, of $6 million.

The company also reported $1.3 billion in trading revenue, a 14% increase on the previous year, as well as a boost of 29% in EBIT (totalling $171 million).

CSR achieved the EBIT-boost, namely in two of its main three business categories: building products and property. The company’s aluminium business was not as lucrative this half-year.

For the company’s building products segment, CSR was able to achieve a 15% increase in EBIT ($139 million). It put the improvement down to well-managed costs and prices.

CSR also managed a significant climb for property’s EBIT, from $7 million in 2021, to a total of $28 million for 2022. This result included its most recent tranche at Horsley Park, NSW.

As mentioned, the aluminium segment didn’t perform quite as well as the others, with EBIT decreasing by $1 million. CSR attributed the lacking result to higher aluminium pricing and raw material input costs.

CSR posted a dividend of 16.5 cents a share for the half year, keeping in with its 60–80% of net profit after tax promise to shareholders.

Source: CSR

The company’s CEO, Julie Coates, said it has been forced to adapt to systems like its Hebel lightweight concrete — which is recognised as faster to build — in order to mitigate labour pressure, rising costs, and supply chain issues.

CSR has also invested in three key sites in NSW and Queensland, and future earnings should be supported by property assets, a ‘core strategy’ that has increased to $1.5 billion in value on an ‘as-is basis’.

Coates commented:

‘CSR’s businesses have performed very well over the last six months. In Building Products, we continue to see strong execution with our teams working hard to deliver for our customers. The result was also supported by price and cost discipline reflecting our ability to manage the business in an inflationary environment.

‘CSR’s strong balance sheet provides the capacity for ongoing investment, strong dividend payments, with an interim dividend declared of $79 million as well as $22 million completed in the on-market share buyback since July 2022.’

CSR strategises around inflation

The company believes its building products business travels with ‘good momentum’ and is confident in product demand and a solid pipeline.

Despite inflationary pressures buffeting markets right now, the company is assured of its abilities to manage these factors.

CSR expects its 2023 EBIT in property to be around $68 million and its 2023 aluminium EBIT to be in the range of $8–24 million. However, current elevated costs are expected to last up to 18 months.

A forecasted EBIT for 2023 was not provided for the company’s building products segment but CSR stated the outlook is a strong one.

Top five retirement-worthy stocks

There has been a growing sense of unease in global markets.

Households and businesses have been squeezed as inflation continues to remain elevated.

Yet, some businesses can deal with inflation better than others.

Just look at the record cash generation by Santos and Whitehaven.

Our Editorial Director Greg Canavan has just released a research report profiling five steady stocks with strong cash generation.

Greg thinks these stocks have the potential to outperform in today’s volatile market and be ‘inflation busters’, despite the current bear market.

Regards,

Kiryll Prakapenka,

For The Daily Reckoning Australia