Building supplies manufacturer Brickworks [ASX:BKW] released its FY23 results today, showing a 54% drop in profits across its Australian and American divisions as it faced ‘challenging conditions’ in both markets.

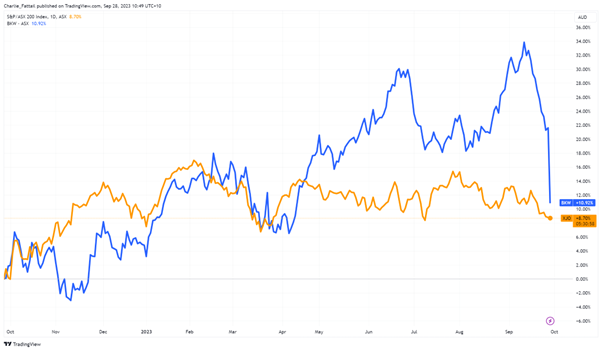

Australia’s largest brick manufacturer saw its shares drop by 8.55% this morning, trading at $23.52 per share as investors digested the tough operating environment, which has seen significant falls in new building projects and ballooning costs.

Despite these challenges for the 12 months ending 31 July, Brickworks reported an 8% in revenue to $1,181 million.

Shares of the company are still up 11% in the past 12 months, as its previous pipeline of work kept shareholders onboard and investors interested. However, as things change, what is next for the company’s stock?

Source: TradingView

Brickworks FY23 Results

Brickworks released its annual report this morning, showing the company has seen a considerable profit drop across all its divisions.

Brickworks champions its diversified operations with four divisions; however, results across the board highlight the challenging year with:

- Building Products Australia: EBITDA $100 million, down 13%

- Building Products North America: EBITDA $40 million, down 18%

- Industrial Property: EBITDA $506 million, down 21%

- Investments: EBITDA $159 million, down 12%

These profits totalled a 54% drop from last year, with a statutory net profit of $395 million. This number is slightly skewered by the large one-off sale of its Washington H Soul Pattinson [ASX:SOL] shares upon its merger with Milton [ASX:MLT] in 2021.

Excluding significant items and discounted operations, the underlying net profits in FY23 were $504 million, down 32%.

The results raise questions about comments made earlier in the year by Brickworks managing director Lindsay Partridge, who admitted to a sharp slowdown in housing and construction in March this year but had promised investors that there was still a ‘six-month pipeline still running’.

The company’s Australian Building Products business comprises Austral Bricks, Austral Masonry, Bristile Roofing, and Austral Pre-Cast Concrete Walls.

While building slowdowns have hurt the group, the company blamed the lion’s share of its falling profits on squeezed margins from inflationary pressures, widespread labour shortages and raw materials supply issues.

Across all combined divisions, margins fell 22% from the previous year to an EBIT margin of 7.2%, highlighting the tight nature of the building supply industry.

The worst among these cost blowouts were seen in the North American division, which saw borrowing costs rise 163% to $53 million from interest rates and heavy one-off cost due to brick plant relocation and commissioning costs.

Brickworks chairman Robert Millner said he was pleased with the joint venture property trust results with Goodman Group [ASX:GMG], which saw its second-largest profits ever.

While revenue was substantial in this area, profits were still down 21% yearly as lowering valuations and development yields cut into profits.

Despite these various cost challenges, Brickworks’ managing director, Lindsay Partridge, was optimistic about the company’s outlook, saying:

‘Within our Property Trusts, the development pipeline is strong, and we expect a significant increase in rental income over the coming years as new developments are completed and rent reviews are undertaken. Across Building Products, order intake is now softening, and we are anticipating a decline in demand in the months ahead. Offsetting the impact of lower sales, unit margins will be supported by price increases and previously implemented plant rationalisation and upgrades. In addition, the exit of the loss-making Austral Bricks Western Australia business will provide a positive impact on earnings.

Having modernised our plant fleet and expanded scale over the past five years through our significant investment program, our priority has now turned to maximising the returns delivered by the enlarged asset base and improving cash generation. With our diversified portfolio of high-quality assets, Brickworks is well placed to meet any future challenges and continue to deliver good performance for shareholders.’

Outlook for Brickworks

The high-interest rate environment has clearly hurt Brickworks significantly across the board.

Within Austral Bricks for example, unit electricity costs were up 28% year on year, labour was up 13%, and maintenance was up 12%.

Within a ‘higher for longer’ interest rate environment, the company must embark on a disciplined year to try maximise profits across its divisions.

Thankfully, the completion of the new brick plant at Horsely Park and the masonry plant in Oakdale East should mean the company can now bring unit costs back under control.

Another significant concern for the company in the shorter term is energy costs. A 28% spike in electricity costs will be difficult for the company to maintain with such razor-thin margins.

From 2025, these issues should come under control as the significant deal with Santos to supply gas for 11 years will come into effect.

While these new prices are around $12 a gigajoule–higher than the current five-year deal— by 2025, these prices should seem paltry in comparison.

The supply agreement will feed into the Brickwork’s east coast brick-making operations and allow those thin margins to exist from the 500 million bricks it makes annually.

Overall, despite the macroeconomic headwinds, the company’s saving grace may be its diversified model in the longer term. For now, cost pressures will hurt the company in the shorter term and push investors away despite the substantial dividends.

While earnings nosedived, the company maintained its decade-long dividend increase, with a 2% increase in its final dividend of 42 cents. This brings total dividends for the year to 65 cents per share, up 3%.

But in challenging markets, savvy investors need to find more than just straight dividend payers.

Finding the right dividends

The market has roiled stock investors for the past year — the ASX200 is down -0.09% in 2023.

With things looking uncertain in the stock market, and the ASX going sideways, maybe it’s time to change tactics.

Defensive investors are focusing on quality stocks that can provide safety and pay dividends.

But only buying the ‘best dividend payers’ could be a losing position beyond the short term.

That’s why our investing expert and Editorial Director, Greg Canavan, has spent his time finding the right balance.

He calls it the Royal Dividend Portfolio, and he believes it’s the sweet spot between growth and dividends.

If you think you’re overexposed in uncertain times or simply too defensive with cash and bonds, you may want to consider making smarter investments.

Click here to learn more about what that looks like.

Regards,

Charles Ormond

For Money Morning