Earlier this week, my colleague Kiryll Prakapenka put together a fantastic article on ‘Buy now, pay later’ companies. Or BNPL stocks, as most people know them.

You can check out the full article for yourself right here if you missed it.

But essentially, the gist of the piece was dissecting whether or not BNPL businesses will ever make actual profits. Because when you study and analyse the way these stocks operate, as Kiryll has done, you start to doubt whether it is actually possible.

As he bluntly concluded:

‘But if Afterpay is possibly generating more than 50% of ROC per annum on its most active users but still operating at a (growing) loss, what does it say about the sustainability of the BNPL business model?’

It certainly is something investors need to keep in mind when investing in this sector. Particularly as Afterpay is often considered the best that BNPL has to offer…

Thinking short and thinking long

I followed and kept tabs on Afterpay for years. It was easily one of the best — if not the best — recommendations we made in our small-cap-focused paid newsletter.

I won’t disclose any specific details, but I can tell you that subscribers who followed our advice walked away with a four-digit percentile gain. It’s the kind of return that every small-cap investor dreams of.

But, of course, much of this was due to the speculative frenzy surrounding the stock at the time. Before COVID, all people wanted from BNPL stocks was growth amongst users, merchants, and transactions.

Profit was the least of their concern. That was something that would come later down the line…

Today, though, in our inflation-fixated world, things are different. Cheap capital and unlimited growth are no longer the staples they once were. Instead, investors have started to care about respectable cash flow, earnings, and of course, profit.

It shows that no matter how popular a trend may be, market cycles and sentiment are still king.

No one knows how long this bearish cloud will hang over markets either. I can only imagine it will require inflation to be tamed and the Fed to tone down its tightening rhetoric, at least. And even then, by the time that happens, who knows what the state of the global economy will be…

In this context, the short-term outlook for BNPL will almost certainly be rocky.

But one could also argue that many of these risks have already been priced in. After all, we’ve seen BNPL stocks suffer massive share price declines over the past year.

The challenge for them now is to prove whether they will sink or swim.

Because no matter how bad the market may get, good businesses will find ways to deliver on long-term potential.

Learning from the best

To give you a real example of what I’m talking about, I want you to look at the following chart:

|

|

| Source: Trading View |

What you’re looking at is a particular stock’s share price movement over roughly four years. As you can see, the company went from trading at around 30 US cents per share all the way up to about US$5.40 per share. All in the span of about two and a half years.

But then came the crash…

And just as quickly as this stock made its gains, so too did it lose them.

Look at any BNPL stock on the ASX today from the past five years, and you’ll see a chart almost exactly like this one. It’s almost uncanny how perfectly they match.

So what company does this chart belong to?

Amazon.

This four-year snippet from Amazon’s early trading years amidst the dotcom bubble is merely a footnote in what has become one of the most successful and profitable businesses ever.

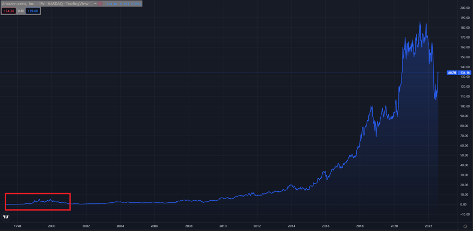

Here is their full chart (with the previous section highlighted) to give you proper context:

|

|

| Source: Trading View |

From its IPO in late 1997, it took Amazon seven years before it posted its first annual profit. And even then, it would take six more years before its share price got close to that US$5.40 figure.

Today, a quarter of a century since it first went public, Amazon has delivered a 148,966% return.

But do you think the market cared about that potential after the dotcom bubble burst?

No, of course not.

Their focus was on the short-term viability of the business and its ability to generate a profit — a focus that was and is by no means wrong but undeniably short-sighted.

I’m not going to suggest BNPL stocks will necessarily be able to do the same thing. Amazon is very much an outlier amidst a sea of failed peers.

What it should tell investors, though, is that it is possible.

Only time will tell what sort of potential BNPL can truly deliver. But I certainly wouldn’t write them off completely just yet.

Regards,

|

Ryan Clarkson-Ledward,

Editor, Money Morning

Ryan is also co-editor of Exponential Stock Investor, a stock tipping newsletter that hunts down promising small-cap stocks. For information on how to subscribe and see what Ryan’s telling subscribers right now, click here.