AGL Energy [ASX:AGL] reported a statutory loss of $1.26 billion this morning after a volatile year of trading and the write-down of one of its coal power plants.

Despite the grim headline, AGL showed some healthy signs with underlying profits of $281 million, up by 25% from FY22. This shows some sign of life as the company eked gains from the massive volatility in wholesale energy markets seen this year.

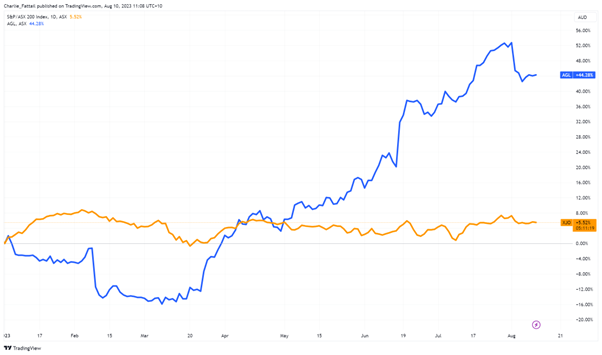

The company’s shares have remained relatively flat in early trading on Thursday, currently up by 0.17%, trading at $11.60 per share.

It’s been a relatively positive year for the company as it gains momentum in transitioning from its coal-heavy past. Leadership and shareholders now appear back on the same page after the previous CEO and board were butting heads with majority shareholders about the path forward for the company.

AGL has seen steady share price gains of 35.66% in the past 12 months with the only significant downturn in June. This comes after AGL was served with a class action lawsuit alleging energy price manipulation in the southeastern states.

Source: TradingView

Net loss, but underlying profit beats estimates

AGL Energy, Australia’s largest electricity retailer, has reported an annual loss of $1.26 billion due to the previously earmarked write-down of one of Australia’s largest carbon-emitting coal power plants.

This totalled a $680 million write-down hit from its power stations and a $890 million loss on the value of derivative contracts.

However, the company’s underlying profit beat analysts’ estimates thanks to a solid second half.

Underlying profit after tax for the year ended June 30 rose by 25% to $281 million, up from $225 million in the previous year.

Underlying EBITDA jumped by 12% to $1.36 billion — reaching the top end of guidance already raised in June — partly thanks to rising wholesale energy prices.

It’s been a volatile couple of years for wholesale energy prices which have seen 60% price swings this year.

AGL CEO Damien Nicks said the company had a ‘strong’ second half, with improved plant availability and strong performance from its gas portfolio and customer businesses.

‘We expect this positive momentum to continue into FY24, as indicated by our earnings guidance which is unchanged from our announcement in June 2023.’

The move to close several coal power stations a decade before planned was a significant turning point for the 185-year-old company.

AGL leadership bowed to pressure from shareholders, particularly billionaire Mike Cannon-Brookes, who owns 11.28% through Grok Ventures.

The activist shareholder has led a successful campaign of forcing the early closure as well as scuppering a planned demerger in May last year.

Since then, AGL has seen a CEO change and a board reshuffle that has leaned the company more towards renewable energy.

Outlook for AGL

The outlook for AGL’s future will largely depend more on individuals’ views on net-zero transitions than underlying figures.

While these eye-watering losses are headline news, AGLs books show that the company is not struggling.

This is, in part, due to the sky-high wholesale energy prices that are currently hitting Australians.

These are expected to moderate in the coming years as transmission reinvestments come through and capacity begins to pick up.

Source: Australian Energy Regulator

The hanging question is whether AGL can successfully transition its generation to renewables with sufficient output without huge capital expenditure.

Mark Samter, senior research analyst at MST Marquee, was one of those questioning this future, saying:

‘The quantum of capital needed to even partially replace the coal capacity is eye-watering.

‘Just how much of those earnings you are happy to see evaporate as a shareholder will determine how much equity you are willing to give to retain part of that earnings stream.

‘It is entirely unfathomable to me that AGL won’t be asking you for equity in the near term.’

I remain less sceptical than Mr Samter — AGL recently secured a $500 million sustainability-linked loan on top of its existing debt facility.

Further subsidies and support during the transition should make the path forward more manageable for AGL and shareholders than some expect.

However, current analyst targets don’t show significant share price growth from here, and dividends sit at 23 cents per share.

Finding dividends that are worth your time

The market has roiled stock investors for the past year — steady ground has been rare.

With things looking uncertain in the stock market, maybe it’s time to change tactics.

Smart investors are focusing on quality stocks that can provide safety and pay dividends.

But blindly buying the ‘best dividend-payers’ could be a fruitless move beyond the short term.

That’s why our investing expert and Editorial Director, Greg Canavan, has spent his time finding the smart move.

He calls it the Royal Dividend Portfolio, and it’s the sweet spot between growth and dividends.

If you think you’re overexposed in uncertain times or simply too defensive with cash and bonds, you may want to consider a different strategy.

Click here to learn more about what that looks like.

Regards,

Charles Ormond,

For Money Morning