China just told BHP to take a hike.

Well, temporarily at least. But when the world’s largest iron ore consumer freezes out one of the big three miners, markets listen.

This week, Beijing’s state-run iron ore buyer, China Mineral Resources Group (CMRG), instructed domestic steel mills to halt all new purchases of BHP ore cargoes.

We don’t know how long this will last, but for now, the ban covers everything from ore sitting in Australian ports to the millions in shipments already crossing the Pacific.

Yesterday, iron ore futures jumped 1.8% to $105 a ton on the news, while BHP shares tumbled 5% in London and 2.8% on the ASX.

Not catastrophic, but a 6-ish billion haircut to their market cap is still notable.

Many have dismissed this as a short-term negotiating tactic and moved past the story. But here is why you should consider it again.

The Real Story Behind the Curtain

Yes, it’s fair to say this is likely temporary. China needs BHP — and vice versa.

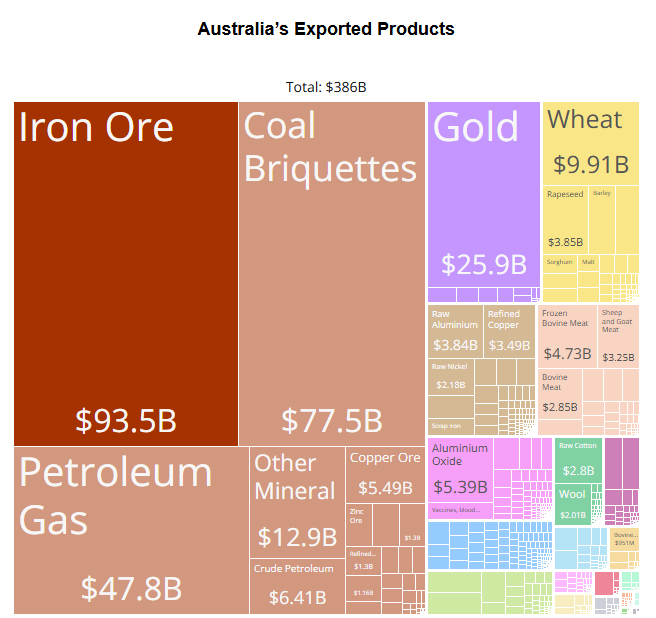

BHP exports an estimated US$23 billion worth of iron ore to China each year. That’s roughly 3.5% of our total exports, a truly monstrous sum that keeps both our economies ticking.

Source: OEC – 2023 Australian Exports

But this isn’t just about iron ore pricing disputes. For China, it’s about something far bigger.

Yes, CMRG wants better pricing on long-term contracts. But this move is part of China’s broader ‘anti-involution’ campaign.

That’s a sweeping policy shift that could reshape everything from commodity markets to the ASX.

So what exactly is ‘involution’?

In Chinese, it’s Neijuan (内卷), roughly translating to excessive, self-defeating competition.

Picture this: ten ice cream shops on the same street, all cutting prices to steal customers. Eventually, they’re all selling at a loss, nobody’s making money, but none can afford to stop.

That’s involution. A destructive competition where everyone works harder just to stay in the same place.

This has become the buzzword in Chinese leadership circles recently, as the phenomenon has slowly infected China’s entire economy.

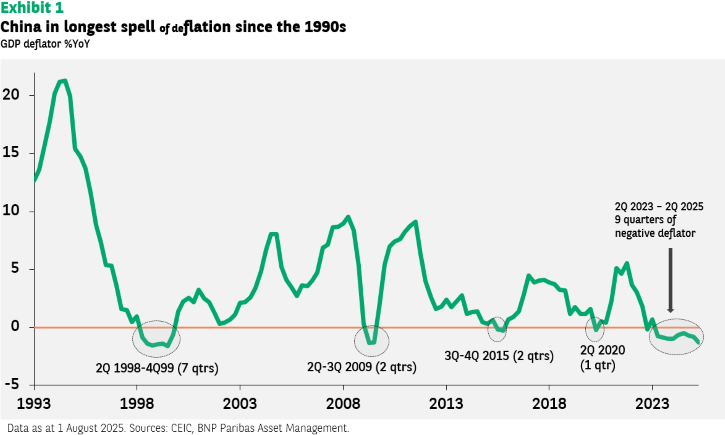

Industrial profit margins have collapsed to 5%, their lowest since 2010. Producer prices have been negative for 35 straight months.

Deflation has been China’s central struggle while we’ve battled inflation.

Source: BNP Paribas

The solution? Beijing is forcing consolidation across industries. And they’re starting with the big ones.

Why Iron Ore Matters

China accounts for 70% of global iron ore demand. While BHP, along with Rio Tinto and Vale essentially control supply. It’s been a cosy arrangement… until now.

You see, the timing is no accident. China’s steel demand is moderating.

Combine that with the new iron ore supply about to flood the market (Rio Tinto’s massive Simandou mine in Africa).

Suddenly, Beijing has leverage it hasn’t had in decades. It’s no longer the captive buyer of the past.

Its central planners also want to move beyond an economy of infrastructure projects.

I think the ban serves more than just trying to influence price:

- Price discipline: Force miners to reconsider their pricing power

- Market consolidation: Accelerate the shutdown of inefficient domestic steel mills

- Supply diversification: Signal to African suppliers that China is open for business

But there’s a fourth, unspoken goal: reflation.

The Deflation Dilemma

China’s economy is stuck in a deflationary spiral. Overcapacity has led to price wars across industries from EVs to solar panels to, yes, steel.

The 2025 anti-involution campaign aims to break this cycle. By restricting supply and forcing weaker players out, Beijing hopes to restore pricing power and profitability.

Consider China’s auto industry. Since 2020, EV sales have exploded tenfold. But total industry profits fell 33%. Why?

Too many players, too much capacity, and a vicious price war that nobody could win.

Source: Deutsche Bank

Sound familiar? It’s the same story in steel, solar panels, lithium batteries — virtually every industry China dominates.

This is why CMRG was founded in 2022. Before then Australia made hay while the Chinese domestic steel mills outbid each other.

What Does This Mean for Us?

Obviously, in the short term, it’s not great. But the longer-term implications are more nuanced.

First, the good news: if China succeeds in reflating its economy, commodity demand could surprise to the upside.

A healthier Chinese economy means stronger demand for everything Australia digs up.

Second, the reality check: Beijing is serious about reducing dependence on the West (as we are them).

African supply is coming online, and Brazil is building back. The days of Australian miners dictating terms are numbered.

Yes, they’ll likely still rely on WA iron ore for the next decade, but Beijing is playing a longer game.

The anti-involution campaign represents China’s attempt to transition from quantity to quality, from growth at any cost to sustainable profitability.

It’s messy, disruptive, and probably necessary.

Will it work? History suggests these top-down campaigns often create more problems than they solve. But with factory usage rates at a slack 74% and profits evaporating, Beijing doesn’t have many options.

For Australian investors, the message is clear: the China trade isn’t what it used to be.

Time to get selective. Time to diversify. And time to stop assuming China will always need what we’re selling.

Because if there’s one thing this BHP ban shows, it’s that Beijing is willing to endure short-term pain for long-term gain.

And they’re just getting started.

Regards,

Charlie Ormond,

ATLAS and Altucher’s Investment Network Australia

Comments