You might have read the book by Robert Kiyosaki called ‘Rich Dad, Poor Dad.’

It’s been a while since I read it, but it holds some sage and straightforward advice:

Kiyosaki contrasts two father figures—his biological father, the “Poor Dad,” a well-educated but financially struggling employee, and the “Rich Dad,” a savvy entrepreneur with a keen understanding of money.

I don’t know if these fatherly figures were made up, but the message is clear enough…

Kiyosaki lays out the importance of financial education and developing passive income streams over traditional employment.

The book encourages readers to cultivate financial independence and emphasises the power of entrepreneurship and financial literacy.

But coming across the book again recently reminded me that I’ve had my own ‘Rich Dad, Poor Dad’ experience!

Equinox: The Rich Dad Experience

In the early 2000s, I worked for the copper explorer and producer Equinox Minerals.

That’s where I cut my teeth as a field geologist in the remote north-west province of Zambia, just near the DRC border.

By 2010, the sector was melting up; copper was the main game in town, and the world’s largest miners were looking to establish themselves in emerging copper frontiers.

Sensing the euphoria, the Equinox board began fishing for a buyout offer.

The Chinese-owned MMG was the first to throw in an offer in late 2010.

At the time, most of us working at Equinox were under the belief that we’d soon be working for a new Chinese boss!

But the deal-making wasn’t over…

Given the market’s jubilation, the Perth-based Equinox board bided its time and fished the market for a higher bid.

And it didn’t take long in that manic commodity market.

Soon after MMG’s offer, the Equinox board struck a surprise deal with the Canadian-owned miner Barrick Gold in early 2011.

Barrick offered a whopping US$7.2 billion for this mid-cap miner without much wrangling, trumping MMG’s offer.

This was my ‘Rich Dad’ experience.

I watched Equinox grow rapidly from a smallish mining outfit to a multi-billion-dollar beast.

It was one of the biggest success stories from the last mining boom.

Management understood the commodity cycle.

They expanded and ramped up their copper mine in Zambia as conditions turned bullish. Then, they timed their exit precisely at the top in 2011.

But rather than depart, I decided to stick around and see what would happen under Barrick’s management.

And that experience was just as valuable…

Barrick: The ‘Poor Dad’

Equinox successfully crafted billions in shareholder wealth.

But Barrick did the opposite.

It managed to erode billions in shareholder value in less than a decade.

The gold major made its multi-billion-dollar bet at the very peak of the market… Demonstrating that it had no understanding of the commodity cycle.

But, with FOMO setting in and the rush to get a deal done, it was also blatantly obvious that it had failed to do any due diligence in the deal.

Barrick had no idea what it was buying.

It grossly overpaid for Equinox’s assets.

And to make matters worse, by 2012, conditions began to deteriorate across the resource sector.

Copper prices were collapsing.

Across the globe, buyer’s remorse was setting in for the dozens of mining firms that bought at the peak of the market.

But this was especially bad for Barrick.

By 2013, just two years after its takeover, Barrick announced a humiliating US$4.2 billion write-down on the Equinox deal.

At a shareholders meeting, Barrick’s CEO admitted that he’d grossly overpaid in the race to nab Equinox’s prized copper asset.

A few months later, he was fired!

Watching this from the inside as a geologist at Equinox, then Barrick, was a fascinating and rich learning experience.

I witnessed the rise of one of the biggest success stories from the last mining boom. Then the demise of the world’s largest gold miner.

So, what did I learn?

The key message from this story was that the hubris in 2011 left a deep scar on the mining industry.

And that’s carried through with essential implications today.

Bullish emotions that culminated in 2011 made a powerful decade-long reversal.

That brought on historic underinvestment, mass layoffs, and mining fire sales.

A few years after the 2011 peak, the sun had set on the early 2000s commodity boom.

Like never before, major mining firms tightened their purse strings and focused exclusively on cash preservation.

Investment in growth vanished.

But this was precisely the time to invest… The downturn years that extended from 2013 to 2020.

That’s what Equinox did in the last commodity downturn, in the late 1990s.

Buying cheap assets when no one was interested.

Anyway, what happened to the world’s largest gold miner, Barrick?

In its former glory, Barrick was once a North American gold giant that featured on the Fortune Global 500 list.

But despite gold prices surging over the last 18 months, Barrick has continued its long-term terminal decline.

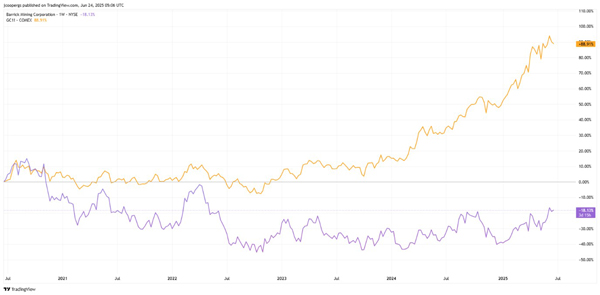

Here’s a chart of gold futures versus Barrick’s share price (purple):

| |

| Source: TradingView |

It’s a sorry sight indeed!

Over the last five years, gold has surged 89% while Barrick shares have fallen over 18%!

And almost 60% since the 2011 Equinox takeover deal.

I’ve worked for plenty of mining and exploration companies over the years, each has its own discovery tale, takeover deal or miserable demise.

That’s the nature of being in a boom and bust industry that can take you anywhere in the world!

Now, I’m sharing those experiences with readers and using it as the foundation for my resource stock portfolio.

Finding companies that understand the commodity cycle and are looking to re-create that ‘Rich Dad’ or Equinox story.

If you’d like to find out more, you can do so here.

Regards,

|

James Cooper,

Editor, Mining: Phase One and Diggers and Drillers

Comments