This week you and I are going on a mission of learning and discovery.

The Laffont brothers say AI is taking the economy toward a productivity boom that will reshape the global economy

Have you heard of these two men? Probably not. Don’t worry. Neither had I until last week.

They run a massive tech hedge fund called Coatue with US$84 billion under management.

When they put a bet on, it’s a big one. They’re placing their bets now.

Your money and your lifestyle could look a lot different if they’re right or wrong. So will mine.

What’s the next big trend in tech?

Hey, you already know…AI, of course!

These two gents just shared their ideas on this massive theme.

There’s a whole lot to unpack here, from US deficits to stock market valuations to – for us here in Australia – the current valuation of CBA shares.

We’ll cover it all this week.

Just on that…

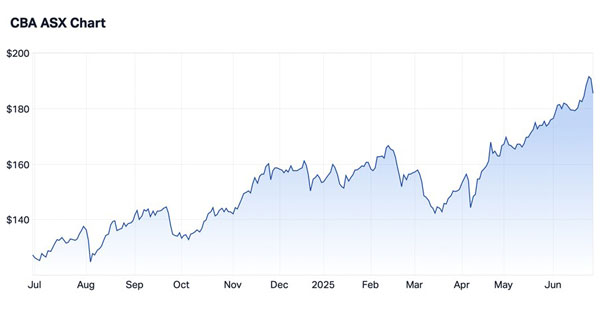

Here’s the chart of CBA over the last year:

| |

| Source: Market Index |

I follow the markets every day.

Let me tell you…I did not see anyone call CBA a strong buy 12 months ago, at least publicly. The brokers said it was overvalued and had no earnings growth.

In fact, I saw the same case against CBA as I did against Tesla years ago.

The analysts compared both to their peers in each industry.

The gripe? Tesla was the most expensive car company. CBA was the most expensive bank. Both were way over the others in relative terms. It didn’t make sense, according to conventional analysis.

But the market did not look at them this way. It still doesn’t. It values them differently. The difference is around technology.

Blue chips like CBA aren’t my beat. But I went along with the broker argument without thinking that much about it. It seemed intuitive.

Intuitive, indeed – but wrong. CBA is up 46% over the last year. It’s now valued at $310 billion.

The usual explanation for this CBA outperformance is the rise of passive money flowing into the market.

Well…maybe…at least in part. But really? Don’t you think there’s more to it than that?

I sure do.

The Laffont brothers have a better explanation.

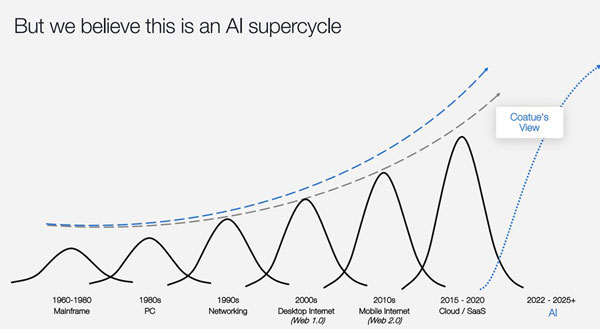

The men and women at Coatue say we’re now in an AI supercycle that will eventually eclipse all previous tech booms.

You can see that visually here…

| |

| Source: Coatue |

Business and consumers are adopting AI apps like ChatGPT at a pace never seen before.

“AI agents” are driving the next phase of this cycle as their reasoning capability expands.

Coatue argue that this means companies are entering a golden age of margin expansion.

Why?

Because companies can add big growth without adding additional costs via headcount.

The new tech metric is “revenue per employee”.

Here’s the rub for CBA: about 60% of their cost base is wages and staff expenses, according to Perplexity.

Clearly, the more work CBA can outsource to AI, the more profitable the bank will be. This is why CBA trades on a P/E of 30.

We keep hearing this is nuts. Maybe it isn’t. There’s nothing to say it doesn’t go to 40 or 50. That all depends on where AI takes us.

We already know that CBA is the leading bank in Australia when it comes to technology. CBA chief Matt Comyn is deep into AI too.

There are hundreds of use cases where the bank can use AI as well – from customer service to fraud detection to risk assessment. The list is almost endless.

CBA shares may look “expensive” viewed against history. Here’s the thing. It’s not 2006 or 2016 anymore. It’s an AI world now.

AI isn’t part of the conversation. It IS the conversation.

The AI revolution is going to fundamentally reshape the bank into something unrecognisable in 5 years, at least operationally.

What’s true for CBA is true for companies the world over.

Similarly, those that nitpick that the ASX trades on an “expensive” P/E of 19 or so are also missing the point.

There’s a potential bonanza of productivity and profits ahead for world markets, Australia included.

If you’re not following this, you’re missing a massive chance to turbocharge your wealth in the next decade.

This is also why my colleague James Altucher is howling from the rooftops that AI is the biggest, but also the last, US tech boom you’re likely to get a crack at in your lifetime.

Don’t sit around dilly dallying. Go here NOW to see how to take advantage of this EPIC “wealth window”.

As an example, James and I said quite clearly to scoop up Nvidia in the recent sell off. AI was always going to trump the tariff issue.

Nvidia is up 50% in 2.5 months. It’s now the most valuable listed firm in history again.

Don’t you see? The AI revolution is NOW.

More tomorrow!

Best wishes,

|

Callum Newman,

Editor, Small-Cap Systems and Australian Small-Cap Investigator

Murray’s Chart of the Day –

Brent Crude Oil

| |

| Source: Tradingview |

As the end of the month approaches, I think it is instructive to have a look at how Brent Crude Oil will be finishing the month after a wild ride in June.

The Israel/Iran war put a rocket under the oil price, but with the worst fears unrealised the price has crashed back to Earth.

A look at the monthly chart above, shows the situation clearly.

The oil price remains in long-term downtrend despite the big run during the month.

The high of the move in June hit stiff resistance at the 20-month simple moving average.

If the long-term downtrend is ongoing that is where you would expect a short-term rally to fail. It also retested the point of control (middle) of the whole rally between 2020-2022 and was rejected from there.

The month will finish with the price falling back below the 10-month EMA (Exponential moving average). That is not a great sign for future price action.

There remains a big line in the sand at US$58.00 which is 15% below the current price of US$68.00.

As long as the price remains above there, we may be in the early stages of a recovery in the oil price. Another run above US$80.00 from here would be quite bullish.

But if we see continued weakness and US$58.00 doesn’t hold, then watch out below as the next target for Brent crude oil would be US$45.00.

Regards,

|

Murray Dawes,

Editor, Retirement Trader and Fat Tail Microcaps

Comments