Last week, ANZ Bank Chief Executive Shayne Elliott warned that some Australian households are about to face some stern tests as rising interest rates push up mortgage repayments and threaten to exceed some household’s buffers.

Elliott said the Reserve Bank of Australia’s latest 25 basis point hike meant that in some cases customers will pay more than the buffer ANZ built in when it first calculated customers’ ability to meet repayments.

Speaking to 3AW radio, Elliot elaborated:

‘The lowest rate we ever gave anyone was 1.94 per cent as a fixed rate.

‘We assumed rates could go up to 5.25%, so we built a buffer which is about where we are now, so that buffer has worked.

‘[W]e are at a very difficult pivot point.

‘Up to now people have been managing OK…but it’s really from here on it gets very difficult because we are over that buffer, and it starts to really bite into people’s savings.’

Households approaching buffer limits is one way to track the stress a mortgage-heavy economy is under. What about others?

Reserve Bank crawls Twitter

In December, the Reserve Bank released a bulletin on measures to assess financial stress.

The central bank admitted ‘high-frequency and timely indicators of emerging signs of financial stress are not readily available’.

But the RBA is developing ‘novel measures’ to counteract this, including using social media data.

Twitter and Google Trends are two sources of data the RBA is now tracking (emphasis added):

‘We construct measures of financial stress based on Twitter data by tracking the proportion of all tweets from Australian users that contain keywords suggesting financial difficulties. The queries are constructed to capture both the relevant topic and negative sentiments. We do so by counting all tweets that contain pair-wise combinations of words related to household or business debt with associated negative connotations. For example, the tweet “feeling overwhelmed by my mortgage” would be counted in our indicator.’

The central bank’s research found that the Google Trends and Twitter data correlated highly with the bank’s chosen measure — the mortgage arrears rate.

News coverage did not correlate well and was too sensitive to overseas stories.

Interestingly, RBA’s research team found that Google Trends data often acts as a good leading indicator (emphasis added):

‘These results suggest that the Google Trend and Twitter indices could help provide an early-warning indicator of the overall level of household financial stress that is relevant both for financial stability and in anticipating how households may respond to income shocks. The Bank’s new Google- and Twitter-based measures of household stress are strongly associated with, and for Google Trends lead, the household arrears rate.’

|

|

| Source: RBA |

The question of savings

A confounding variable in assessing the impact of rising interest rates is our large pandemic savings.

Couped up at home with little to do, we began to accumulate cash.

In some cases, our cash balance was also propped up by generous government help.

The money we would have spent on travel, holidays, pubs, theatres, and so on, was instead piling up in our accounts.

At one point during the pandemic, the saving ratio of Australian households reached multi-decade highs:

|

|

| Source: RBA |

Now, of course, with the pandemic and lockdowns a hazy memory, we are drawing down our savings.

High inflation is also leading us to draw down our savings faster than usual.

But while the saving ratio has come well down, it still finds itself at pre-pandemic levels.

Our personal finances are still in familiar territory.

We are feeling the pain of higher prices and rising mortgage repayments, but the pain is so far being dulled by excess savings.

|

|

| Source: Bloomberg |

Falling consumer sentiment

What’s interesting is that despite our saving ratio still hovering at pre-pandemic levels, we’re more pessimistic than we’ve been in more than a decade.

Consumer sentiment is lower than the nadir hit during the height of COVID-19:

|

|

| Source: RBA |

Why is sentiment so low if savings are still holding up?

Well, why not put the RBA’s newfangled measures of financial stress to work?

In the December bulletin note, the RBA found that new measures suggested a ‘pick-up in financial stress’ not yet reflected in the arrears rate:

‘All three indices — particularly the more zeitgeist-driven news and Twitter indices — have risen over 2022, despite limited signs in official data of a pick-up in financial stress across Australian households as a whole. This may reflect that the new indicators capture early-stage financial stress and that the impact of the combination of higher interest rates and inflation varies significantly across households. It could also be driven by anticipation of future financial stress based on overseas news and events.’

And while Australia’s net wealth is elevated, it has tracked in the wrong direction lately.

Are Australians sensing more pain to come? Is the low consumer sentiment a result of a pessimistic outlook for the year ahead?

|

|

| Source: RBA |

Australia’s net wealth is tied in a big way to property.

And property prices aren’t exactly strong at the moment…not to mention the swarm of households about to transition from low fixed-rate loans to high variable loans.

Here’s The Sydney Morning Herald reporting on the looming fixed-rate cliff yesterday:

‘Analysis by KPMG suggests those people who took advantage of record-low fixed interest rates in 2020 and 2021 will this year confront a financial hit so large it will slow the economy more than expected by the RBA.

‘Hundreds of thousands of homeowners with fixed-rate mortgages face a $16,500 repayment cliff this year that, along with further interest rate rises from the Reserve Bank, could punch a $20 billion hole in the economy.’

How are the retailers doing?

If discretionary spending is slowing, that’s a good indicator of the wider mood and financial health of the consumer.

So how is discretionary spending going?

In its latest Statement on Monetary Policy released earlier this month, the RBA said ‘growth in household consumption was strong, underpinned by the ongoing rebound in spending on international travel and other discretionary services’.

But this growth is slowing.

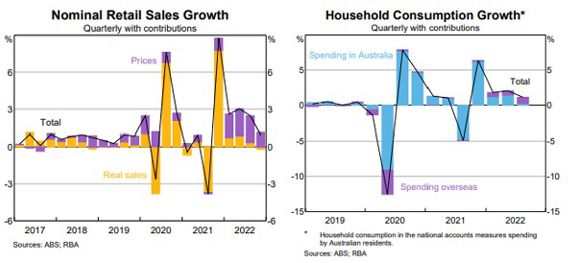

Real household spending moderated in the December quarter, with retail sales declining:

‘Growth in retail sales values slowed, with declines in household goods, department stores, and clothing and footwear. Retail prices increased strongly and the volume of retail sales declined in the quarter. This weakness was concentrated in discretionary goods categories and was partially offset by solid growth in spending on food and at cafes and restaurants.’

|

|

| Source: RBA |

We can glean further clues from retailers.

Yesterday, huge retailer JB Hi-Fi [ASX:JBH] closed 5% lower after admitting sales began to soften in January.

CEO Terry Smart told investors (emphasis added):

‘While we are pleased with the January trading result, with sales continuing to be well above pre Covid January 2020, we have seen sales growth start to moderate from the elevated levels seen in the first half of FY23. As we enter an uncertain period, our business is well placed with a proven ability to adapt to any changes in the retail environment and trusted value-based offerings that will continue to resonate with our customers and grow our market share.’

Furniture retailer Temple & Webster [ASX:TPW] released its half-year results today, with revenue down 12% year-on-year and profit down

47%.

Importantly, Temple & Webster said sales between January and 5 February this year were down 7% on the prior comparable period.

TPW’s peer Nick Scali [ASX:NCK], while growing revenue in its latest half, was not confident about trading conditions to provide guidance, only saying 2H23 result will depend on trading during February to April.

You don’t say.

So, what does it all mean?

Our savings are currently at pre-pandemic levels. Seemingly, that suggests we are in a solid place.

But the pessimistic consumer sentiment suggests Aussie households don’t believe their savings will remain at those levels for long.

The huge jump in mortgage repayments about to hit households exiting fixed rates is also set to add to pressure on savings.

Room for discretionary spending is shrinking.

Retail spending is slowing as a result.

Our Editorial Director Greg Canavan didn’t mince words when he wrote yesterday:

‘So while consumer spending is healthy on the surface, keep in mind that it’s not sustainable at the current pace.

‘[C]onsumer sentiment is in the toilet. In fact, it’s worse than it was in 2008. And with more interest rate rises coming, it’s hard to see any improvement on the horizon.

‘The Aussie consumer is cooked!’

What does that mean for stocks?

Falling earnings.

The US shows what could be in store for Australian companies.

As Reuters reported overnight:

‘Expectations for U.S. earnings to decline in the first and second quarter come amid weaker-than-expected fourth-quarter results for 2022, which Credit Suisse estimates will be the worst earnings season outside of a recession in 24 years.

‘With fourth-quarter 2022 earnings estimated to have fallen from a year ago, a subsequent decline in the first quarter of 2023 would put the S&P 500 into a so-called earnings recession, a back-to-back decline in earnings that hasn’t occurred since COVID-19 blasted corporate results in 2020.

‘Fourth-quarter results are in already from 344 of the S&P 500 companies, and the quarter’s earnings are estimated at this point to have fallen 2.8% from the year-ago period, according to IBES data from Refinitiv.’

Investor, beware.

Regards,

|

Kiryll Prakapenka,

For Money Morning

PS: Jim Rickards’ new book SOLD OUT! depicts an even more gruesome tale for the common consumer: one of high prices, bare shelves, energy shortages, fuel panics, and low growth. It’s a must-read for anyone wanting to survive and thrive in this new world. You’ll hear about it more tomorrow. Stay tuned.