Qantas Airways [ASX:QAN] is in the headlines for all the wrong reasons this morning as the horror week continues for the embattled company as all sides collapse on the airline company’s activities this past year.

The mounting pressure appears to have spurred significant action at the top as Qantas CEO Alan Joyce announced his early departure from the company.

With the ink barely dry on its ‘turnaround’, $1.7 billion in profit last week, the company has now faced questions about its tactics to achieve the results, starkly contrasting the previous year’s $1.86 billion loss.

The company faces allegations of illegal ticket sales, undue influence over the government, high ticket costs, and poor performance as the pile-on intensifies this month.

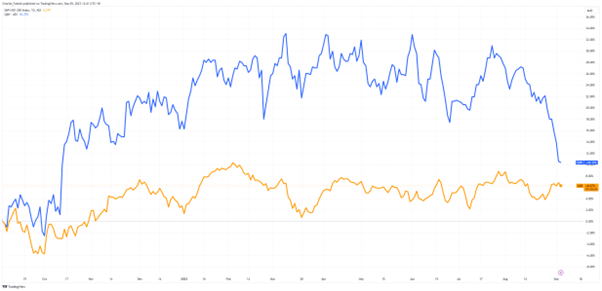

Shares have had a bumpy morning but remain up by 0.35%, trading at $5.67 per share after the decision to leave.

The airline’s shares have dipped 11% in the past month but have still seen a healthy 11% gain overall in the past year as the company has fought hard to regain profitability, although now it appears at some cost to its reputation.

Source: TradingView

Qantas’ scandals multiply

Qantas CEO Alan Joyce will step down from the top job two months earlier than planned after weeks of public and regulatory pressure mounts on the national carrier.

Mr Joyce has been CEO for 15 years and has seen the company through the challenging COVID period but has been seen as a divisive figure for rigid cost controls and headcount reductions in the past.

His remuneration package is expected to total $24 million this year, with the company announcing on Friday that Mr Joyce had received 1.74 million shares valued at just more than $10 million.

The package has caught the ire of the Aviation Union, which has called on the board to scrap bonuses as part of its ‘reset’.

The negative press continued as competition watchdog ACCC threatened a potential record fine of $250 million for selling approximately 8,000 tickets to cancelled flights throughout 2022.

As of yesterday, the company refused to say if the practice had stopped, while pilots and engineers are quoted as saying it remained in place.

Another major scandal rocking the company is the alleged government interference in the decision to block an additional 21 Qatar Airways flights into Australia.

Coalition transport spokeswoman Bridget McKenzie said the government’s decision to block Qatar was ‘anti-competitive’ and made airfares more expensive, and the whole process should face a Senate inquiry.

In a statement, Joyce said he was stepping down ‘to help the company accelerate its renewal.’ He said he was leaving Qantas ‘fundamentally strong’ with a ‘bright future’.

Joyce’s successor will be Vanessa Hudson, the current chief financial officer. Hudson will face the challenge of restoring public trust in Qantas and navigating the airline through a period of significant capital expenditure.

Outlook for Qantas

It will be a long road for the company to restore its reputation in the eyes of the Australian people.

In the 2023 World Airline Awards, Qantas fell to number 17 from rank five last year, as customer complaints mounted from everything from late flights, lost baggage and devious COVID flight credit practices.

It seemed Qantas chose profits over reputation as the carrier battled higher costs last year and the slow recovery of flights returning to pre-pandemic capacity.

With the changing of the guard, shareholder concerns will move to the ballooning costs that will inevitably come as the carrier addresses the myriad of concerns being raised.

Customer views of poor service combined with high fares will likely mean a tough number of years for the company to get back into the public good books, which will likely involve pulling out the chequebook.

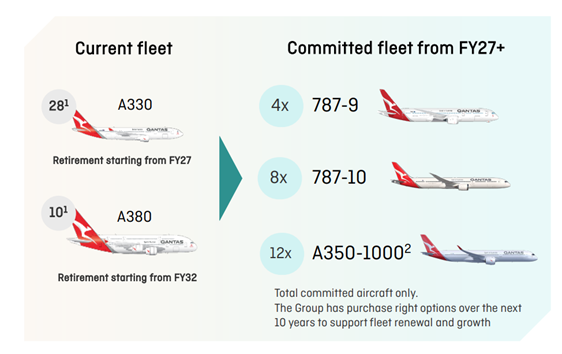

Another factor that will push costs higher is the efforts to restore the company’s ageing fleet to working order.

Source: Qantas FY23 Report

COVID-19 delays and cancellations in aircraft deliveries have already added pressure to the fleet, which is now clearly affecting the carrier’s performance in an untenable way.

Early forecasts peg the cost at approximately $15 billion over the next five years, a significant change from the $7 billion it has spent in the previous five.

For shareholders and investors, the past week should give pause for big moves as further inquiries and scrutiny are likely before the dust settles.

Australia’s largest companies will remain in the spotlight as investors seek bigger fish for security in uncertain times, but not all big players are suitable investments right now.

Royal dividends

The market is facing another bumpy day as seasonal weakness combines with China’s property market woes to cause underperformance in the ASX.

Maybe it’s time to change tactics when things are looking weak.

Intelligent investors are focusing on quality stocks that can provide safety and pay dividends.

But only buying straight dividend-payers could be a losing move in anything but the short term.

That’s why our investing expert and Editorial Director, Greg Canavan, has spent his time finding a balance.

He calls it the Royal Dividend Portfolio, and it’s the sweet spot between growth and dividends.

If you think you’re overexposed or simply too defensive, you need to consider something that can provide you with an income but also has a chance to grow.

Click here to learn more about what that looks like.

Regards,

Charles Ormond,

For Money Morning