Do stocks outperform government bonds?

The answer seems obvious. Given the equity risk premium and the earnings growth potential, stocks clearly outperform.

How could they not?

But as a highly cited finance paper showed a few years ago, most stocks don’t.

While the stock market can outperform safe assets like Treasuries, not every individual stock is destined to do the same.

In fact, the majority of stocks are duds.

Do stocks outperform Treasury bills?

It’s not often that a paper in the Journal of Financial Economics gets widespread media coverage and causes a stir in the professional investment community.

But that’s exactly what happened to a paper written by Arizona State University finance professor Hendrik Bessembinder.

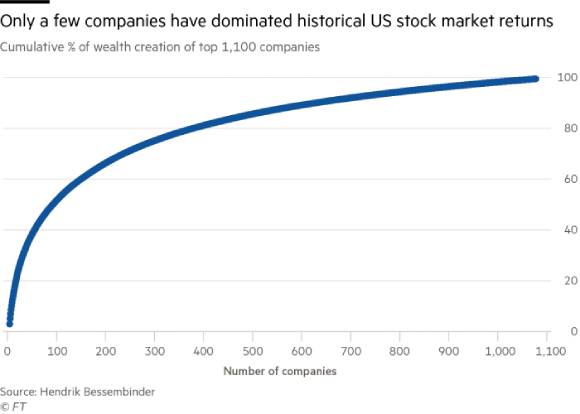

Bessembinder’s 2017 paper ‘Do Stocks Outperform Treasury Bills?’ looked at 26,000 companies listed between 1926 and 2016 and tracked their performance.

Bessembinder’s findings were stark.

Just 86 stocks accounted for US$16 trillion in wealth creation — half of the stock market total — over the past 90 or so years.

It gets even starker.

All the wealth creation can be attributed to the 1,000 top-performing stocks, while the remaining 96% of stocks collectively only managed to match one-month T-bills.

|

|

| Source: Financial Times |

In Bessembinder’s words:

‘While the overall US stock market has handily outperformed Treasury bills in the long run, most individual common stocks have not. Of the nearly 26,000 common stocks that have appeared on CRSP from 1926 to 2016, less than half generated a positive lifetime buy-and-hold return (inclusive of reinvested dividends) and only 42.6% have a lifetime buy-and-hold return greater than the one-month Treasury bill over the same time interval. The positive performance of the overall market is attributable to large returns generated by relatively few stocks.’

|

|

| Source: WP Carey School of Business |

The average stock isn’t much good

Morningstar’s John Rekenthaler aimed to replicate Bessembinder’s findings in an April 2021 research note.

Rekenthaler freshened up Bessembinder’s data by analysing the results of US stocks over the most recent decade ending December 2020.

Rekenthaler’s dataset ‘clearly supports Bessembinder’s argument’.

Once again, data showed that the majority of stocks either underperform…or simply vanish.

Rekenthaler found only 42% of US stocks in the preceding decade finished up. 36% posted 10-year losses. The final 22% disappeared.

Crucially, Rekenthaler summarised that ‘even during a decade marked by an almost uninterrupted bull market, the average stock wasn’t much good’.

Larger stocks fare better

Interestingly, Rekenthaler found that the trend was weaker for larger stocks.

Of all the US stocks, only 42% posted a positive return over the decade.

But when disaggregated for size, Rekenthaler found 77% of the biggest 1,000 stocks ended the decade higher.

The success ratio for the next 4,000 stocks by size dropped to 33%.

But even the larger firms don’t have much to be proud of if pitted against conservative performance benchmarks like bonds.

As Rekenthaler pointed out:

‘Although equities thrashed bonds for the decade, by the whopping cumulative margin of 267% to 49%, only half of the biggest 1,000 stocks beat the bond index. Against the stock index, their winning percentage plummeted to just 20%. In other words, four out of five large U.S. stocks trailed their own performance benchmark.’

Venture capital and moonshots

So if most stocks are duds over time and only a tiny portion of stocks account for the majority of gains, what’s the takeaway?

What strategy should investors adopt?

It depends, of course.

Show Bessembinder’s findings to two people, and you might get two different strategies.

One might see in Bessembinder’s data the futility of active investing.

‘If so many stocks fail, what are the chances of me finding the generational performers? I might as well buy an index tracking the whole market,’ says the pessimist.

The optimist might reply, ‘Precisely! When so many stocks fail, why would you subsidise that failure by buying a broad index? Why not take calculated risks and seek out stocks with outsized returns potential?’

I don’t think the dispute can be settled. It’s a matter of risk and return. Investors’ risk and return settings are calibrated differently.

Venture capitalists, however, do see in Bessembinder’s research a way to riches…albeit laden with risk.

Sebastian Mallaby describes this well in his book, The Power Law: Venture Capital and the Art of Disruption (emphasis added):

‘Now consider the returns in venture capital. Horsley Bridge is an investment company with stakes in venture funds that backed 7,000 startups between 1985 and 2014. A small subset of these deals, accounting for just 5 percent of the total capital deployed, generated fully 60 percent of all the Horsley Bridge returns during this period.

‘Other venture investors report even more skewed returns: Y Combinator, which backs fledgling tech startups, calculated in 2012 that three-quarters of its gains came from just 2 of the 280 outfits it had bet on. “The biggest secret in venture Capital is that the best investment in a successful fund equals or outperforms the entire rest of the fund,” the venture capitalist Peter Thiel has written.” “Venture capital is not even a home-run business,” Bill Gurley of Benchmark Capital once remarked. “It’s a grand-slam business.”’

A grand slam is the maximal four-run baseball play when a home run is hit with all three bases occupied.

Bessembinder is aware of his work’s influence on moonshot investing, telling the Financial Times in 2021:

‘I think I have provided some ammunition for the people who say it’s their business to chase moonshots. The skewness shows just how big the pay-offs can be if you’re good at this.’

But it’s important to note Bessembinder’s conclusion to his seminal paper:

‘The results in this paper imply that the returns to active stock selection can be very large, if the investor is either fortunate or skilled enough to select a concentrated portfolio containing stocks that go on to earn extreme positive returns. Of course, the key question of whether an investor can reliably identify in advance such “home run” stocks, or can identify a manager with the skill to do so, remains.’

Finding the Amazons and Apples of the stock world is hard.

I think it’s hard for at least two reasons.

One, only very few stocks account for most of the wealth creation. So the search is hard purely on the numbers alone.

And two, finding the great wealth accumulators takes analytical skill, foresight, patience, and luck.

Finding great stocks isn’t like finding a needle in the haystack but like finding a needle among hundreds of haystacks.

Faced with the enormity of the task, some decide simply to exit the search and buy up all the haystacks.

One of them, surely, has the needle.

I didn’t know this about central bank digital currencies

Before I go, I wanted to share a very interesting stat I came across.

According to the Atlantic Council think tank, 105 countries are exploring or have already created a central bank digital currency (CBDC).

These 105 countries represent 95% of global gross domestic product!

I was taken aback. I didn’t think it would be that many countries.

Clearly, I underestimated how big a development CBDCs are. And I got another reminder last week.

Last Friday, the Biden administration inched closer to developing a CBDC.

Back in March, President Biden issued an executive order calling on various agencies to investigate digital assets. Last week, the agencies released their reports and recommendations.

One recommendation from the US Treasury was for the US to ‘advance policy and technical work on a potential central bank digital currency, or CBDC, so that the United States is prepared if CBDC is determined to be in the national interest.’

Treasury Secretary Janet Yellen seemed to favour advancing a CBDC, telling the press, ‘Right now, some aspects of our current payment system are too slow or too expensive.’

It certainly seems like we’ll be hearing more about CBDCs from our politicians and financial regulators.

So if you want to learn more about CBDCs and their implications, our Editorial Director, Greg Canavan, has put together this thorough presentation on the matter.

I highly recommend you watch the briefing, as it offers a nice breakdown of all things CBDCs.

Until next week,

|

Kiryll Prakapenka,

For Money Morning