ASX News LIVE | XJO to Fall, US Markets Closed for MLK Day, Iron Ore Falls

Market close update

The ASX 200 closed down 1.09% today, trading at 7,414.8 as the benchmark reached a four-week low and is down -2.32% for the year to date.

All sectors closed in the red today, with Telecoms faring the best, down -0.54%, while Utilities (-1.76%) and Energy (-1.53%) faced the largest losses at the closing bell.

For individual companies, the biggest losses on the ASX 200 were Lovisa Holdings, down -5.22%, and Ansell, down -4.47%.

Iron ore miners also dragged down the index as iron ore futures continue to tumble after further bearish news from China weighs on markets.

Meanwhile, Contact Energy +4.80% and Orora +2.28% were the biggest gainers on the ASX 200.

Trump wins Iowa caucus, further instability possible

Donald Trump has won the Iowa caucuses today (AEST), with his two rivals, Nikki Haley and Ron DeSantis, trailing far behind.

Trump won 56% of the vote, with DeSantis at 19% and Haley at 18%.

The win is a critical first step for the former president’s run to what looks to be smooth sailing for him to another showdown with President Biden.

Looking ahead to the general election can be a mixed bag for markets and US voters as further instability is likely in the heated and sometimes shakey elections in a divided America.

“He is totally destroying our country,” Trump said of Biden. “We were a great nation three years ago, and today, people are laughing at us.”

The language of divisiveness will add to what is already shaping up to be a mixed year of political instability; from the war in Ukraine to tensions in the Middle East and Taiwan, there is plenty to watch for 2024.

Here is a good article summarising what is likely to be shaky for geopolitics and markets in the coming months.

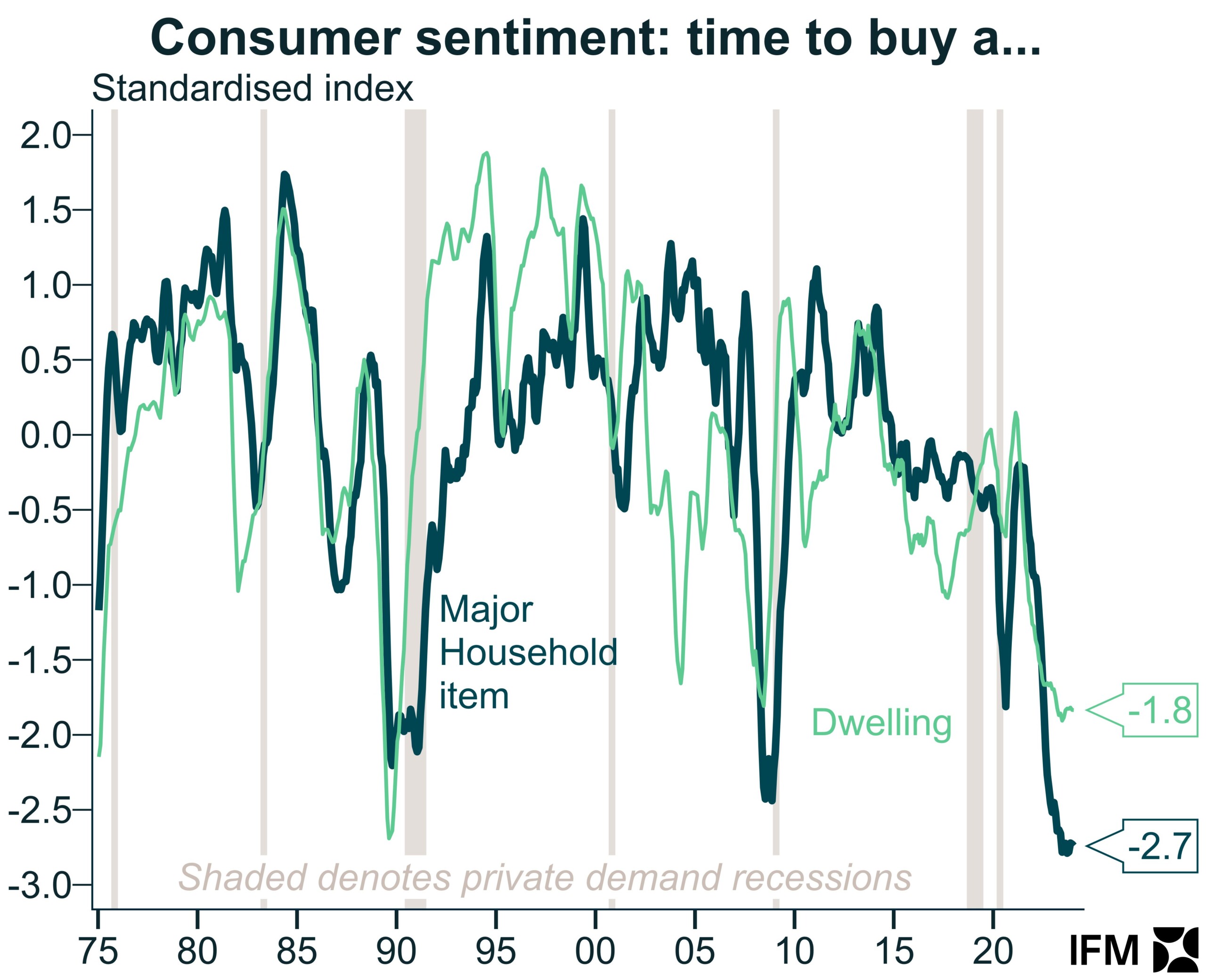

Consumer sentiment takes a hit

After some recoveries to sentiment in the December period, things are looking grim again in the eyes of consumers.

This survey asked consumers what they felt about ‘the timing to buy a dwelling or major household item‘.

The results were not great, with the Westpac Consumer Sentiment falling 1.3% to 81.

The bank described the results as the ‘Weakest January read outside of the early-90s recession‘

Source: IFM – Westpac

Inflation battle continues

The Melbourne Institute’s latest Australian monthly trimmed mean inflation data shows we still have a ways to go before getting inflation under control.

Their monthly inflation gauge rose 0.9% in December 2023, pushing inflation from 3.8% in November to 5.2% in December, the biggest jump since May 2023.

The unfortunate reality that is likely to come from this is interest rate cuts far later than many had hoped and bet on.

Unless we see serious shifts in unemployment figures, it is likely that the first cuts to the 12-year high-interest rates will be sometime closer to September than the market’s earlier hopes of between May and April.

The @MelbInstUOM Australia monthly trimmed mean inflation gauge jumped by a record equalling 0.9% in December 2023. The annual growth rate soared from 3.8% in November to 5.2% in December, the biggest lift since May 2023. #ausecon #auspol @CommSec pic.twitter.com/jobNwxHXQH

— CommSec (@CommSec) January 15, 2024

Midday market update

The ASX 200 is down 0.91% at 7,428.2 around 1:30pm AEST. The continued sell-off has put the ASX 200 down -2.14% for Janurary so far and up +0.54% for the past 12 months.

The ASX benchmark follows weakness in European markets as Wall St remains closed for MLK day.

Near midday all sectors are firmly in the red, with the worst peforming sectors Utilities (-1.43%) and Materials (-1.42%).

The All Ords index is down -0.90% while major miners trend down. BHP (-1.37%), Rio Tinto (-1.38%), Fortescue (-1.69%).

In other news the major supermarket retailers Coles (-1.52%) and Woolworths (-1.02%) are also down after the competition watchdog ACCC said it was considering suing a big supermarket chain for breaching consumer law on false discount pricings.

Pilbara deal puts spotlight on spodumene price expectations

Many traders are throwing around theories and getting hot under the collar after details of the Pilbara Minerals [ASX:PLS] deal have come to light.

Pilbara has signed a new offtake agreement with China’s Gangfeng. Under the deal, Pilbara will sell up to 310,000 tpa of spodumene concentrate to Gangfeng between 2024 and 26 under a long-term supply agreement that adds to the previous 2017 deal of 160,000 tpa.

An additional 100-150k can be added to the deal each year by Pilbara if they wish, but that will probably be conditional on improving prices, which are down 80% in the past 12 months.

Pilbara’s Managing Director, Dale Henderson, told investors the demand for its concentrate from the EV battery supply chain remained strong.

“This increased supply with Ganfeng builds on our established partnership as we work together to further extend our position in the growing market for lithium products.”

“This increase demonstrates the demand for Pilbara Minerals’ spodumene concentrate while preserving optionality for the company as we assess long-term downstream opportunities in-line with our growth strategy.”

“The long-term outlook for the industry remains incredibly exciting. Both Ganfeng and Pilbara Minerals remain focused on extending our respective positions as major, low-cost producers in the burgeoning lithium market. We look forward to further collaboration with Ganfeng and many more successful years working together.”

Here’s an example of a recent post on Twitter (X) highlighting traders’ concerns about the transparency of the spodumene spot prices.

There is some conspiratorial thinking about market manipulation of price here that will be interesting to watch as lithium prices trend throughout this year.

Iron ore prices front and centre

Iron ore prices have been under pressure in recent weeks.

Iron ore has continued its slide today, falling 1.7% to US$127.50 a tonne overnight as a confluence of events weigh on the futures market.

The price has seen continued downward pressure after falling over -6% last week as traders eye China’s economy and tensions in Taiwan and the Red Sea.

For commodity analysts, the problems, first and foremost, were around demand. ‘Prices fell amid a deteriorating outlook,’ said ANZ senior commodity analyst Daniel Hynes. He noted stockpiles in China have risen for six straight months.

For CBA’s commodity analyst Vivek Dhar, the recent fall is squarely from the shifting margins of Chinese steel mills, saying in a note today that he thinks the peak was US$144 a tonne and that it’s only down from here:

Mr Dhar says a correction is ‘underway‘ and ‘likely has more to go‘.

“China’s steel mill margins have slumped as iron ore prices have increased.”

“Typically negative steel mill margins will weigh on iron ore prices, albeit with some lag historically, as the economic incentive to produce steel and consume iron ore is reduced.”

“The last time that steel margins in China were this negative or lower for a sustained period in late June 2022, iron ore prices eventually dipped below $US100/t. The current downward correction in iron ore prices could threaten the same level temporarily too.”

“However, once steel mill margins stabilise, we think iron ore prices are likely find support in the $US100-$US110/t range, waiting in anticipation for China’s policy direction for 2024.”

“China’s ‘Two Sessions’ policy meetings in March, where policymakers announce China’s economic growth targets for 2024, is shaping up to be a key event for iron ore and other commodities. We think policymakers will announce an economic growth target of around 5% in 2024, similar to its target last year.”

Many traders had expected movements from officials at the PBOC to alter the reserve requirement ratio (RRR) for banks, allowing them to hold less in their coffers and lend more to help prop up the ailing property market.

The current weighted RRR stands at around 7.4% after multiple cuts in 2023, but officials last week had hinted that they were thinking about reducing it again. That failed to materialise this week.

It seems traders were hoping for further stimulus to come from China to maintain those higher iron ore prices. Adding to the woes were the Taiwan elections that took place last weekend.

The winner of the election, prior vice president William Lai Chine-te, is considered a ‘troublemaker through and through‘ and separatist by the mainland.

Tensions in both the Taiwanese Straight and Red Sea have been enough for traders to price in the concern.

Rio Tinto also gave an update on its iron ore production today, showing its iron ore exports have rebounded, delivering their best volume in five years.

They also held their guidance for Pilbara iron ore shipments for 2024 after shipping 86.1 million tonnes in the final quarter of 2023.

Fourth-quarter shipments were down 1% on the PCP, but overall Rio shipped 3% more for 2023 than 2022, at 331.8 million tonnes.

The held target for 2024 is 323-338 million tonnes.

Morning market update

Good morning. Charlie here

The ASX 200 opened down -0.27 % to 7,475.8, as European markets also show signs of weakness as the US enjoys Martin Luther King Day.

The biggest news out of European markets was the German GDP numbers that showed an anaemic -0.3% shrinking in 2023.

High energy prices and poor exports were to blame for the poor growth, but at least the latest stats show it narrowly avoided a technical recession, although, for many in Germany, it may not feel that way.

Iron ore prices fell again overnight, now down over -6% since last week, as weak data from China and tensions in the Red Sea have pushed prices down.

Chinese officials also surprised the market by deciding to leave a key banking rate on hold rather than reducing the requirements on their big banks.

Known as the Reserve Requirement Ratio (RRR) many people were hoping the PBOC would lower the requirement ratio by 25 basis points to allow further lending.

By holding back this option, many Iron ore traders were concerned about the knock-on effects for the Chinese property market, adding to the downward pressure.

Wall Street: Closed

Overseas: FTSE -0.39%, STOXX -0.57%, Nikkei +0.90%, SSE +0.15%

The Aussie dollar fell -0.43% to US 66.57 cents.

US 10-year bond yields flat at 3.94%.

Australian 10-year bond yields +6bps to 4.13%.

Gold up +0.40% to US$2,055.41. Silver rose +0.28% to US$23.22.

Bitcoin rose +1.26% to US$42,574, while Ethereum rose +1.33% to US$2,514.

Oil Brent rose +0.37% to US$78.58, while WTI Crude fell -0.36% to US$72.42.

Iron ore fell -1.7% to US$127.50 a tonne.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988