ASX News LIVE | ASX to Fall as Rising Bond Yields Push Down Markets; Gold Sets Fresh High

Market close update

The ASX 200 closed down -1.34% to 7,782.5. A sharp corrective drop for the index as almost all sectors were down today as markets readjusted their expectations for rate cuts in the year.

Only Energy and Utilities avoided the worst of the selloff, with both sitting a little above flat for the day as Origin closed up +0.65% and oil prices lifted Energy stocks.

The biggest falls were seen in the interest rate-sensitive stocks of Tech (-3.94%) and Real Estate (-3.22%), with sharp falls in the major caps in both.

In tech, Wisetech fell -5% to $90.20 as the company announced the retirement of one of its non-executive board members, while Xero was down -5.69% to $125.01 per share.

While on the broader index, the biggest faller was Westgold Resources, falling -14.80% to $2.36 per share after the company cut its full-year production guidance for 2024.

Commodity News

With bond yields rising and equity markets pulling back for now, I thought we could look at some major commodity markets to see what is happening in the space.

Oil markets saw Brent crude rise nearly 2% on escalating geopolitical tensions in the Middle East and Ukraine-Russia.

Iran vowed retaliation today to the drone strike that killed Iranian generals at the Iranian Embassy in Damascus yesterday.

While Ukrainian drones struck the Taneko refinery deep inside Russia. The strike was located over 1,115km from the Ukrainian border and is one of many strikes carried out in the past months that have affected nearly 15% of the Russian oil refining capacity.

Source: S&P Global

Also affecting oil prices this week, Mexico’s Pemex cancelled supply contracts for its Maya crude blend ahead of the June elections, jolting supply.

While looking forward the focus now shifts to the upcoming OPEC ministerial meeting, expected to address individual member compliance with agreed output cuts. According to a Bloomberg poll, Iraq, UAE, and Gabon have been collectively exceeding their quotas by several hundred thousand barrels per day.

To metals and silver spiked today, with its spot price up +5.3% to US$26.43 per ounce, while gold continues to look strong, up by +1.61% to US$2,285.31 per ounce.

Base metals also rallied, with copper and aluminium gaining around 1.5%. Improved sentiment stemmed from stronger U.S. ISM data and better-than-expected China PMI figures. Meanwhile, China’s Ministry of Industry and Information Technology met with top steelmaker executives to analyze current challenges and promote “stable operations” and “healthy development” within the sector.

Meanwhile, U.S Treasury Secretary Janet Yellen has announced she will return to China this week to discuss the country’s growing industrial overcapacity.

Midday market update

The ASX 200 is down -1.26% at 7,788.6, now well down from its near-record high, following significant losses on Wall Street overnight.

US markets were dragged down by doubts about the timing of the Federal Reserve’s upcoming interest rate cut and heavy losses by major players like Tesla, which fell nearly -5%.

Other Asian markets have fallen in a reaction as well today, with the Nikkei 225 falling -0.81% and all of Europe’s indices following suit overnight.

On the ASX only the gold explorers remain a bright spot in the market as the price of gold continues to sit near record highs, trading at US$2,278.94.

The price of gold is now up 23.3% in the past six months and looks to continue to shrug off interest rate concerns as geopolitical risk runs high.

On the index, only the Utilities and Energy sectors remain barely holding onto the green, while all other nine sectors are down today, the worst being Real Estate (-3.25%) and Technology (-3.78%).

Westgold seperates from broader gold explorer boom

Gold explorers are the major gainers on this red day, with companies like West African Resources up +5.10% and Rameluis Resources up by nearly 10%.

Meanwhile, the biggest ASX faller so far today is Westgold Resources [ASX:WGX] down by -12% as the company released its revised full-year 2024 production guidance downward.

The Western Australian gold miner now expects to produce between 220,000 and 230,000 ounces at an all-in sustaining cost ranging from $2,100 to $2,300 per ounce.

According to Westgold’s latest quarterly production update, the company produced 52,100 ounces of gold during the quarter, with an average sale price of $3,137 per ounce.

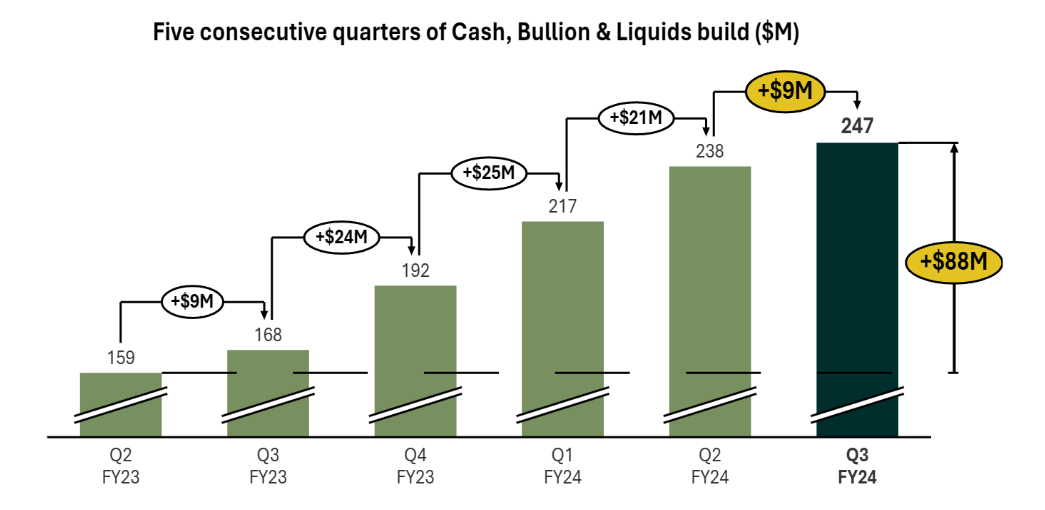

The company’s managing director and CEO Wayne Bramwell commented on the results, arguing that investors should focus instead on the cash build by the business, saying:

‘Westgold has now delivered five consecutive quarters of cash build, adding $9M to our treasury in a very trying quarter. Several factors negatively impacted our physical outputs but corporately our prime driver is free cash flow – not maximising total production at all costs.’

Source: WGX

With shares now trading at $2.44, now 33 cents down today, It seems investors were unconvinced.

Morning market update

Good morning. Charlie here,

The ASX 200 opened down -0.21%, to 7,871.6 following falls overnight on Wall Street as interest rate cuts remain on the mind of markets. This is the second consecutive day of a pullback, as high bond yields put downward pressure on the market’s growth-focused sectors.

Some jitters in the US for when the timing of interest rate cuts has been the major focus of this pull-back, with notes such as Cleveland’s Fed President Loretta Mester saying that she needs “more data to raise my confidence [of cuts this year].”

Here’s the spike in Australian and US-10-year treasury bonds putting pressure on equities.

Source: TradingView

Tech and discretionary are seeing sell-offs, as well as yield-sensitive areas like real estate and riskier assets like crypto are also seeing a pullback.

Overnight, Tesla saw its share price fall nearly -5% after reporting a huge fall in deliveries, even after analysts slashed expectations several times. The company’s deliveries followed the same falls as major rival BYD, which also saw its sales drop heavily.

Maintaining their highs are gold and oil, which are both up overnight as geopolitical tensions rise in the Ukraine-Russian conflict and the Middle East.

Gold set another record high of US$2,280 an ounce, finishing overnight sessions at best levels.

The major geopolitical shift rising tensions is the US$100 billion ‘Trump-proof’ fund package for Ukraine. The proposed five-year military aid package seems to pre-empt a trump election to lock in funding and take a more active role in the conflict with Russia.

As one of the diplomats at the meeting said:

“This will be crossing a Rubicon. Nato will have a role in co-ordinating lethal support to Ukraine.”

Wall Street: S&P 500 -0.72%, Dow -1.0%, Nasdaq -0.95%.

Overseas: FTSE -0.22%, STOXX -0.81%, Nikkei flat, SSE flat.

The Aussie dollar rose +0.47% to US 65.20 cents.

US 10-year bond yields +4bps to 4.35%.

Australian 10-year bond yields +14bps to 4.12%.

Gold rose +1.47% to US$2,282.41, while Silver jumped +4.33% to US$26.17.

Bitcoin fell -5.67% to US$65,797, while Ethereum fell -5.93% to US$3,295.

Oil Brent rose +2.0% to US$89.17, while WTI Crude rose +2.05% to US$85.43.

Iron ore rose +0.2% to US$101.35 a tonne.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988