Après moi, le deluge.

(French for: after me, the deluge)

Normally it’s a bit of a nihilistic expression, but today I’m going to lay out a thesis about markets that is bizarrely positive.

Here’s the thesis in a nutshell…

Crazy AI rally…pullback on (insert mini-panic reason)…rate cuts…money flood through to later on in 2026.

Let’s start with what’s happening on the AI front.

By some measures AI is better than sliced bread AND the Internet:

Source: Financial Times

The current AI-driven stock market rally has all the hallmarks of a boom that looks “unstoppable”.

Until, suddenly, it’s not.

A short-term loss of momentum could hit.

Maybe a classic mini-panic, reminiscent of April’s tariff meltdown.

But here’s the twist.

This could trigger a shakeout before paving the way for the next, even bigger, phase of the run-up through 2026.

Leaky faucet or dam about to break…

The thesis is counterintuitive.

Rather than marking the end, a shakeout could provide precisely the fuel needed. The AI rally would broaden. It would mature.

A correction is natural after months where just a handful of large techs dominated gains.

Look at what’s happening already.

Last week, I highlighted the dull memory makers that have made a killing in the last year.

And before that I pointed to the metals side of the story – the rocks that the AI data centres rely on.

Point is: I think the rally’s “plumbing” is still being built.

40% of US GDP Growth: What could go wrong?

A great recent Financial Times article noted that “AI spending by companies now accounts for a 40 per cent share of US GDP growth this year.”

That’s nuts.

It could also prove to be totally unsustainable.

So it’s tricky to predict what will spark the next wobble.

It could be another escalation in global trade tensions. Tariffs. Geopolitical standoffs.

Just like the April tariff shock that wiped out trillions in global market cap in 48 hours.

Maybe Fed policy surprises. Delayed rate cuts. Smaller-than-hoped cuts.

Particularly if inflation proves sticky.

Or AI euphoria running into reality. Disappointing earnings from major chipmakers. A high-profile AI startup implosion.

Infrastructure bottlenecks are possible too. Power grid issues. Chip shortages.

Regulatory shocks. Even a cyber incident highlighting new vulnerabilities.

Or a combination of all of those with the threat of a private credit unwinding event (that’s a long story).

The well is nowhere near dry

Here’s the thing about market “accidents.”

They rarely spell the end.

History shows this. As liquidity returns — think emergency rate cuts or government backstops — investors flood back in.

This time seeking refuge in laggards. Small-caps. Overlooked sectors poised to benefit from the next wave.

Following the tariff shock, the Federal Reserve moved aggressively. Emergency rate cuts. Liquidity injection.

Markets whiplashed higher. Breadth improved.

It wasn’t just the big stocks anymore.

By mid-May, the S&P 500 and NASDAQ had recovered. By June they hit new all-time highs.

The rally was led by a wider range of stocks. Not just tech’s megacaps.

A parallel could play out for AI’s “second wind.”

As expectations reset, investors could look beyond the narrative “front-runners” like Nvidia, AMD, OpenAI etc.

They will start to hunt aggressively for the enablers. Memory companies. Power infrastructure. Security plays.

Specialist software. And commodities too.

I’ll leave you on one final thought…

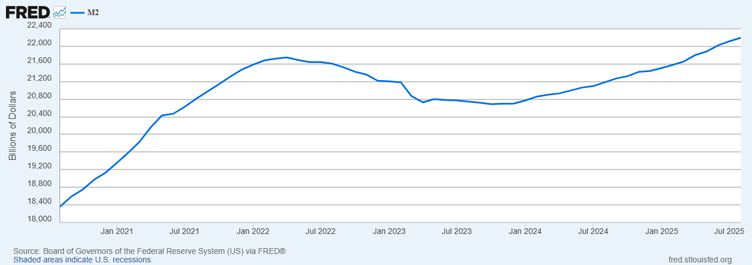

This is M2 Money Supply in the US over the last 5 years:

M2 is a measure of the money supply. It includes cash, checking deposits (M1), plus savings deposits, small time deposits, and retail money market mutual fund shares.

In my eyes, that’s a rough measure of US money that’s available to be pushed into the market.

That big hump in the middle left is the 2021-2022 market peak.

Relative to that peak M2 is up about 2%.

And the US Federal reserve is yet to start a major rate cut cycle.

They just need an excuse.

There may be a brief stretch where our greedy gullets get parched along the way.

But I say – bring on the great money flood of 2026.

You ain’t seen nothing yet.

Best Wishes,

Lachlann Tierney,

Australian Small-Cap Investigator and Fat Tail Microcaps

***

Murray’s Chart of the Day – Copper

Source: TradingView

Conditions are ripe for a serious rally in copper.

After five years bumping its head against the brick wall at US$5.00/lb, we may be close to seeing that resistance level become support moving forward.

Trump caused a serious spike and failure in the copper price with his tariff threats.

But the price action since his TACO backdown proves that buyers are lined up at major support levels.

The big picture remains supportive with a clear uptrend in place based on wave structure since 2016.

Based on moving averages a long-term uptrend has been in place since December 2023.

Retests of the 20-month simple moving average (blue line above) has seen strong buying support every time.

After the scare a few months ago saw copper plunge back to the 20-month simple moving average we have seen steady buying support. Prices are now testing US$5.00/lb once again with the odds looking good that buyers will finally overwhelm the sellers and a solid uptrend will take place.

Interest rates are on the way down and there is plenty of fiscal stimulus in key markets, especially China.

Copper needs to fall below US$4.00/lb to switch of the current bullish set up. So any weakness can be seen as a buying opportunity until that happens.

Regards,

Murray Dawes,

Retirement Trader, International Stock Trader and

Murray’s Trading Room

Comments