‘You only find out who is swimming naked when the tide goes out.’

— Warren Buffett

There’s a risk event building.

Last week, a private credit giant permanently halted redemptions from one of its retail-facing funds and began liquidating it.

Blue Owl Capital had offered quarterly redemptions since 2017. Now investors are being told: you’re locked in. Promising to distribute 30% of the assets in a fire sale.

The firm spun the lockdown as orderly.

The market wasn’t buying it. Blue Owl’s stock has halved over the past year.

Their Technology fund saw investors pull more than 15% of net assets in January alone. Its larger US$34 billion Credit Income fund lost a billion dollars in the final quarter of 2025.

This isn’t just a Blue Owl story. Debt is piling up in private credit. And it’s the tip of the iceberg when it comes to AI-linked bets.

These are the firms making deals with hyperscalers to build mammoth data centres and the infrastructure to run them.

At the same time, these firms are also heavily leveraged investors in software companies.

In other words, private credit effectively finances both AI expansion and the earnings streams AI may disrupt.

The timing mismatch between these two forces is where the risk lies.

Shares in Blackstone, KKR, and Ares have all dropped roughly 25% over the past month. The entire private credit complex is under pressure.

Source: WSJ

[Click to open in a new window]

The question is whether this is an isolated tremor or the first crack in something much bigger.

The $2.5 Trillion Experiment

Private credit grew into a US$2.5 trillion-plus market by filling the void left when banks pulled back from risky lending after 2008.

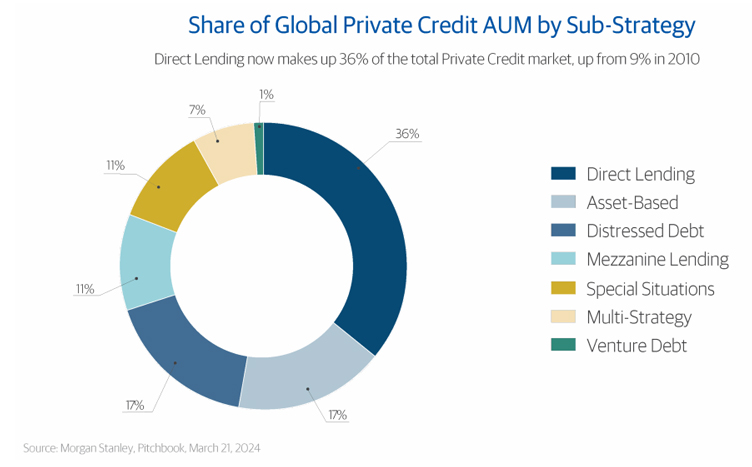

In 2010, direct market lending (like a bank would traditionally make to a company) accounted for only 9% of private credit; now it’s over 36%.

Source: Pitchbook

[Click to open in a new window]

Higher yields than public credit. Lower volatility than stocks. Better risk management through direct relationships. That was the pitch.

To sustain the growth, the industry made two structural bets.

First, it leaned into ‘permanent capital’, funds structured so money theoretically never has to be returned.

Blue Owl’s leadership spent years talking about the ‘layer cake’ of permanent capital underpinning their business.

Second, it poured money into software and technology companies where traditional banks wouldn’t lend.

Often, with opaque and complex loans based on revenue growth rather than profitability.

Both bets are now under severe stress.

The Leverage Multiplier

There’s another layer of risk embedded in private credit: leverage inside sponsor-backed deals.

What does that mean?

Private equity doesn’t buy companies with cash alone. It buys them with borrowed money.

A Blue Owl or a KKR might acquire a business for $100 million using $40 million of equity and $60 million of debt.

If the company later sells for $140 million, the equity return is magnified because the debt is repaid first and the residual flows to shareholders.

A 40% increase in enterprise value becomes a 100% gain on equity. That is the classic leveraged buyout model that has propelled KKR and Blackstone.

That leverage is precisely why private credit has grown so quickly.

They also act as direct lenders, providing leverage, professional oversight, and managing tight reporting standards. In theory, that is meant to reduce risk.

In practice, it concentrates it.

These kinds of deals have expanded across markets. Companies are now borrowing an average of 5 to 8 years’ worth of their annual profit.

That works beautifully in stable or growing earnings environments. It becomes dangerous when cash flows wobble.

The Software Lending Problem

The second vulnerability amplifies this risk.

Private credit’s aggressive expansion into tech lending looked brilliant when rates were low and valuations were soaring. Now the sector faces a double shock.

Rising rates from 2022 onward pressured variable-rate borrowers (precisely the companies private credit loaded up on).

And AI disruption is now threatening the revenue models of the very software companies that private credit backed.

Their rosy recurring revenue assumptions are now being stress-tested big time.

The GFC Parallel

The structural parallels with the mid-2000s housing market are uncomfortable.

Back then, lenders made loans they didn’t intend to hold, packaged them into complex securitised vehicles, and brought retail investors in to hold the bag.

The underlying assumption — that house prices would keep rising and borrowers would keep paying — went unquestioned until it was too late.

Private credit rhymes with that pattern.

Loans are being sliced into complex collateralised vehicles.

Insurance companies and super funds provide the capital base. Retail investors are joining the fray in Australia through ASX-listed stocks, such as Qualitas and Metrics Credit Partners. Often, without fully understanding the risks.

The credit metrics themselves echo the loosened standards that preceded the housing bust. Just as subprime loans were repackaged into CDOs by the big banks, private credit has its own sausage factory.

2008 wasn’t just about housing. It was based on the assumption that borrowers would keep servicing debts.

When credit tightened and jobs fell, that assumption broke. The loans repriced. Then it all went pear-shaped.

Private credit carries a similar risk. If AI dents the white-collar jobs that fund software subscriptions, cash flows shrink.

And when cash flows dry up, ‘permanent capital’ doesn’t seem so permanent.

What to Watch

Private credit won’t blow up overnight. It’s a slower-moving and more diversified behemoth than I have time to get into here.

But the liquidity mismatch is real. The technology lending exposure is real. And the opacity is extreme.

ASIC’s recent surveillance of 28 private funds found that ‘inconsistent disclosures, weak conflict management, and questionable valuation methods,’ were rife.

For Aussie investors, the risks are worth considering. Our super funds and institutional investors have been increasing allocations to private credit in recent years.

If this sector enters a downturn, the unwind will be messy.

Keep an eye on redemption data. Watch the default rates. Watch the insurance company capital ratios.

Because in a crisis, the last thing you want to hear is that the exit is shut.

Regards,

Charlie Ormond,

Small-Cap Systems and Altucher’s Investment Network Australia

Comments