What is investing’s holy grail? What principle or approach yields the best returns?

I’ve come at this question from several angles here at Money Morning.

I’ve covered finding quality stocks via the inspection of business moats.

Or how barriers to entry are the key to understanding competitive advantage.

Or how cash matters more than profit.

Or how companies create value through returns on equity that exceed their cost of capital.

What I haven’t spoken much about is growth.

Could growth be the blade to cut the Gordian Knot of investing?

Investing: don’t over-complicate it

Investing lends itself to complexity.

Dare I say it, one easily succumbs to complexity, thinking the more intricate and convoluted one’s investment methods, the better the results.

Not always so.

Sometimes complexity is just a cacophony of noise crowding out signal.

In Richer, Wiser, Happier, a popular book on top investors, William Green profiled namesake William Danoff.

Danoff is the vice president of the Fidelity Contrafund and trained under Peter Lynch.

In the book, Green said Danoff’s edge lies in his ‘consistent refusal to over-complicate’:

‘[When] I look at a company, I just ask myself: “Are things getting better or are they getting worse?” If they’re getting better, then I want to understand what’s going on.’

Nice and simple.

Danoff’s friend and fellow prominent investor Bill Miller came around to Danoff’s thinking later in his career after spending his early years building elaborate financial models.

These days, Miller focuses on ‘three or four critical issues that he believes will drive the business’:

‘For every company, there are a few key investment variables and the rest of the stuff is noise.’

One of the key variables is growth.

Investing in growth stocks

What businesses should you invest in at the end of the day?

Growing businesses. More specifically, businesses that can sustain growth.

Consider the famous investor Philip A Fisher, author of the popular Common Stocks and Uncommon Profits (Warren Buffett was a fan).

Fisher is synonymous with growth investing. He thought growth stocks offered the greatest potential, not bargain or value stocks:

‘[In] the case of even the genuine bargain, the degree by which it is undervalued is usually somewhat limited. The time it takes to get adjusted to its true value is frequently considerable. So far as I have been able to observe, this means over a time sufficient to give a fair comparison — say five years — the most skilled statistical bargain hunter ends up with a profit which is but a small part of the profit attained by those using reasonable intelligence in appraising the business characteristics of superbly managed growth companies. This, of course, is after charging the growth-stock investor with losses on ventures which did not turn out as expected, and charging the bargain hunter for a proportionate amount of bargains that just didn’t turn out.’

Obviously, growth is crucial to the success of a stock.

A company not growing sales is stagnant, and its share price will likely tread sideways.

This firm could improve efficiency and drive costs down to boost profitability but the level to which this is possible is capped. You can’t reduce costs to zero.

Such companies usually decide to return profits to shareholders via dividends and investors begin to treat these firms as income stocks where capital gains are a minor consideration.

Clearly, growth is necessary for any significant capital appreciation.

After all, Apple didn’t become a US$3 trillion-dollar stock without it.

Apple’s total net sales in 2002 were around US$6 billion. Two decades later, total net sales were just shy of US$400 billion.

Growth matters.

But it’s hard to forecast. Especially years in advance. I’m talking beyond five years.

As Fisher said in his book (emphasis added):

‘Correctly judging the long-range sales curve of a company is of extreme importance to the investor. Superficial judgement can lead to wrong conclusions.’

Peloton is a great example of the difficulty in judging a company’s long-range sales.

Management — and many investors — were led to superficial assessments of Peloton’s sales trajectory during the pandemic.

So the importance of growth is obvious. What really matters though, is forecasting that growth accurately.

Investment edge lies with those keen of sight. The further one can accurately see into a business’s future, the larger their edge.

Prominent hedge fund manager Philippe Laffont offered an example a few years back:

‘The art of growth investing is realizing a stock that appears expensive today can be dirt cheap 5–7 years later. In 2007 Apple traded at 30x EPS but only 3x five years out.’

Some think investing is about finding the stocks with a history of growing earnings or revenue ~20% a year.

But the past is not the right direction an investor should be facing.

It’s the future growth that matters.

Yes, a stock has grown revenue by 20% a year for the last five years. But can it sustain that for the next five?

Hedge fund manager Brett Caughran summarised this idea well when he wrote why it’s the ‘future state’ that matters:

‘Often, but not always, the current fundamentals of the business are reflected in the stock price (this isn’t 1960 and we aren’t Warren Buffett reading a 10-K, seeing some key metrics, and buying the stock…the game has changed).

‘What ultimately matters is a combination of a vision for the future and asymmetry in the odds embedded in the current price.

‘Ultimately, what will matter is not where the business has been, but where it is going.’

Profitable growth — the middle way

We can agree that growth is necessary for hefty stock returns. We can also agree, I hope, that growth on its own is insufficient.

Unprofitable growth is deadly.

Not to mention that unprofitable growth has a shelf life determined by money already in the bank and the patience of investors and creditors.

Patience may be a virtue but it wears thin eventually.

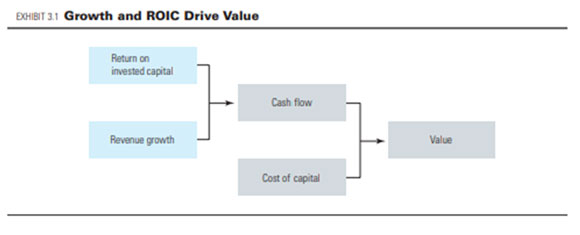

The reason why growth can be so lucrative is because it increases value if the business is profitable.

An unprofitable growing business grows nothing but losses.

|

|

| Source: McKinsey |

As business professor Joan Margetta quipped:

‘There is no honour in size or growth if those are profitless. Competition is about profits, not market share.’

The hard part is when a business is unprofitable now but is expected — through growth — to be profitable later.

Buy now, pay later companies, like Afterpay, are emblematic of this view. Along with ride-share companies like Uber.

But even though Afterpay has grown sales exponentially, its losses rose in tandem.

Growth, therefore, must be at the service of a sound business model.

Growth compounds sound unit economics and unsound unit economics alike. The former is value accretive…the latter is destructive.

Kind regards,

|

Kiryll Prakapenka,

Editor, Money Morning