‘What we have been anticipating for some time is now here. It is the other side of the bubble mountain.’

Paul Singer

(US hedge fund manager and the Founder,

President, and co-CEO of Elliott Management)

‘The universe is under no obligation to make sense to you.’

Neil deGrasse Tyson

Recent action on Wall Street may have you questioning whether the everything bubble is actually deflating.

Short answer to that question? Yes, it is deflating.

What’s happening is normal, the other side of the ‘bubble mountain’, behaviour.

Memories of the bubble era are still fresh.

Hope springs eternal.

Thoughts of, ‘perhaps the worst is over, and it’s back to the good old days’ are entertained.

The ‘risk-ON/risk-OFF’ switch gets flicked to on.

Buying power surges through the indices — catching those with bets on the market going down unawares.

The ‘shorts’ scramble to cover positions.

Momentum kicks index fund algorithms into gear, and markets appear to be on the ‘UP’ again.

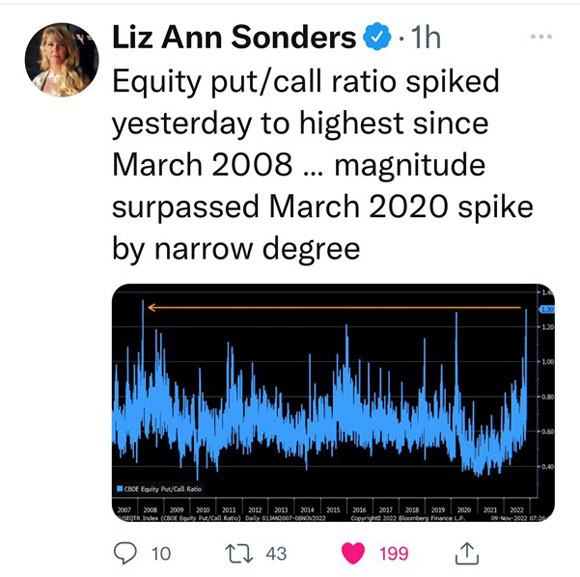

This 9 November 2022 tweet from Liz Ann Sonders (Managing Director and Chief Investment Strategist at Charles Schwab) showed just how much short interest there was in the US market last week.

The CBOE put/call ratio is a measure of investor betting positions.

‘Put’ options make money when the market goes DOWN, and ‘call’ options make money when the market goes UP.

|

|

| Source: Twitter |

On 9 November 2020, there was a lot of money betting on a down market.

When did the (slightly softer) US CPI number (the one that got investors all excited about the worst being over) come out?

The morning of 10 November 2022.

What followed was the classic ‘short squeeze’…turbo-charging the Nasdaq to a one-day gain of 7%.

This ‘head turning’, ‘toing and froing’ action is par for the course in this phase of the cycle.

Knowing this helps to make (a little) sense of the investing universe.

Which, I must confess, can be beyond challenging at times.

When you think you have it (somewhat) worked out, something happens to turn your view on its head.

Don’t investors know (insert what you think is known)?

Why is this happening when (insert your reasoning)?

Eventually (and believe me, that eventuality can take longer to make its appearance than you think), if something cannot continue, then it won’t.

Defiance of this reality (by those suffering from FOMO or unwilling to accept the cycle has turned) helps understand why markets are going up…when all the data dictates the opposite should be happening.

The headwinds are many

Global recession warnings, high inflation, Big Tech corporate layoffs, flagging confidence, persistently high energy costs, and shrinking profit margins. On this last point…

|

|

| Source: Barron’s |

To quote the article…

‘…something else is going to matter much more to investors in the coming year: shrinking profit margins. The writing is on the wall, evident in this season’s outlooks.’

The writing may well be on the wall, but not everyone is reading it — at least not yet.

Earnings are under pressure…and, in the fullness of the cycle, it’s (a multiple of) earnings that eventually determines price.

For now, this reality is being ignored.

Flick the risk-ON switch and go for it.

But you cannot turn a blind eye to what’s happening under the surface indefinitely.

Big Tech (the modern-day ad agencies) is under pressure…as Professor Scott Galloway (Professor of Marketing at NYU Stern) reported on 4 November 2022:

‘Meta’s [formerly Facebook] meltdown is shocking, but not singular. Google is down 40% this year, Amazon 45%, and Snap 80%. These losses are unprecedented in the Big Tech era.

‘As with bankruptcy, the sell-off happened gradually, then suddenly. Last week was a turning point. Amazon, Google, Meta, and Snap all missed big on earnings. The common theme? Ads. Or lack thereof.’

Apple is bucking the trend…however, the other tech behemoths are experiencing declining revenue growth:

|

|

| Source: Profgalloway.com |

Ad revenues are an indication of underlying economic activity.

To quote from Business Insider (emphasis added):

‘Advertising agency revenues are interesting for anyone who cares about economic growth because the large holding companies…have hundreds of clients representing a broad range of companies which sell goods and services to both consumers and other businesses.

‘Ad budgets tend to be set as a portion of sales at each company, or expected sales, and thus rise and fall as companies expect to contract or grow. Ad agencies take a slice of that money as it passes into ad buys, often about 10 percent, and that is their revenue.

‘If companies increase their ad budgets because they are experiencing or expecting revenue growth, it shows up almost immediately in ad agency revenues. Agencies, therefore, are a proxy for corporate economic activity as a whole.’

Falling ad revenues is an indication of economic contraction…and job losses:

|

|

| Source: Twitter |

Why do earnings matter in the ‘bear’ phase of the market?

To quote from the January 2020 issue of The Gowdie Letter:

‘The market’s RED, AMBER, and GREEN signals were identified by Robert Rhea in his 1932 book, The Dow Theory (emphasis added)…

“There are three principal phases of a bear market: the first represents the abandonment of the hopes upon which stocks were purchased at inflated prices; the second reflects selling due to decreased business and earnings, and the third is caused by distress selling of sound securities, regardless of their value, by those who must find a cash market for at least a portion of their assets.”’

The next leg in this bear market is…selling due to decreased business and earnings.

On the other side of ‘bubble mountain’ is a descent into a deep valley.

How slippery, jagged, or lasting this descent might be is the question being asked by many an investor.

One of whom is Lacy Hunt…an almost 60-year veteran of fixed-interest investing.

What he doesn’t know about markets and the economy is NOT worth knowing.

Every quarter, Lacy Hunt pens the must-read ‘Hoisington Investment Management Co. Quarterly Review and Outlook’.

An officially recognised recession is coming

In his latest ‘Review and Outlook’, Lacy Hunt made the following observations:

‘A significant reduction in the current account deficit is a sign of future economic weakness even though it is a plus in terms of the GDP calculation.

‘Such disparities are a common occurrence at the turn from expansion to recession.

‘Other troubling signs confirm this view, including an across the board weakening in rail, trucking and ocean-going freight and a long and diversified list of corporate profit warnings.

‘The index of leading economic indicators [LEI] peaked in February and has declined for six consecutive months, resulting in a year over year decrease in the LEI.

‘These developments point to a recession around the turn of the year. Additionally, the yield curve has inverted, a development consistent with a recession next year.’

In their rush to rejoice, risk-ON investors have missed the bigger picture.

What the softer number indicates is a slackening in the level of demand.

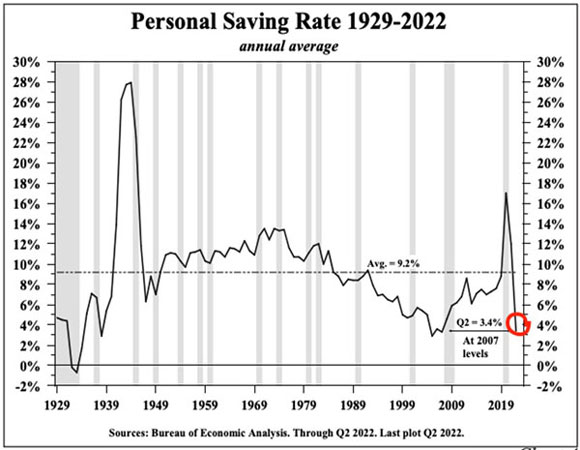

US consumers are cautiously trimming household budgets AND savings are being depleted to maintain consumption:

|

|

| Source: Hoisington Investment Management Co |

The conclusion of Lacy Hunt’s ‘Review and Outlook’ provides plenty of food for thought (emphasis added):

‘The FOMC [Federal Open Market Committee] greatly damaged their credibility when they allowed inflation to race far above their target.

‘Sadly, the deteriorating economic prospects are a direct consequence of the Fed’s failure to execute their fiduciary responsibility to the American public.

‘Almost universally, the other members of the FOMC have supported the Fed chair’s position that low inflation is of paramount importance to deliver a rising standard of living for all.

‘If the Fed were to abandon its commitment to the inflation target, the FOMC would suffer a major double blow to its integrity, which would be increasingly more difficult to restore as Volcker so cogently argued.

‘Failure of the Fed to achieve its target would also have the consequence of allowing an emergent money/price/wage spiral to become entrenched, causing a dismal replay of the two decade span from the early 1960s to the early 1980s.

‘The Fed’s mettle will be tested because highly over leveraged institutions will fail as they historically have done in such situations. Bad actors or their enablers should be directed to bring their collateral to the discount window or, if necessary, to the bankruptcy process rather than be given bailouts that have severely widened the income and wealth divides in the U.S. while causing the Fed to sacrifice price stability that’s so essential for broad-based economic gains.

‘These considerations suggest that the Fed’s current stance should continue. The long-term Treasury market is in the zone of digesting the rapid inflation of the past several quarters, and future Fed rate hikes.

‘Barring any capitulation in the determination to quell inflation by the Fed, long Treasuries will increasingly reflect the looming recession and its deflationary circumstances.’

Here’s a quick summary:

- In failing to act responsibly, the Fed’s reputation is hanging by a thread.

- If the Fed DOES NOT remain committed to its fight against inflation, what’s left of the Fed’s reputation will be destroyed.

- If the Fed DOES NOT remain committed, we risk the scenario outlined in last week’s issue…price/wage spiral of the mid-1960s to early-1980s.

- Staying the distance will NOT be easy in the face of corporate bankruptcies (and the damage this will do to US pension fund balance sheets).

- Lacy Hunt suggests the Fed will continue to raise rates and crush demand.

- Resulting in a recession and deflationary consequences.

I’m not so sure the Fed has the mettle to withstand the pressure that’s bound to come from Washington and Wall Street.

It’s just not in the Fed’s DNA…a reminder from last week’s issue:

‘In October 1987, Greenspan issued a statement declaring “[the Fed] affirmed today its readiness to serve as a source of liquidity to support the economic and financial system.”

‘In 2002, Ben Bernanke stated, “I’d throw dollars out of helicopters if I had to, to stimulate the economy.”

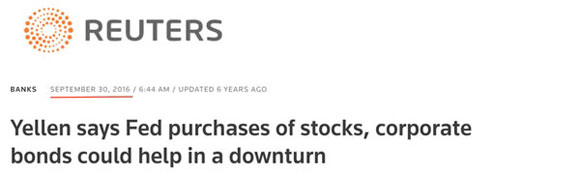

‘Then, in 2016, Janet Yellen gave us a peek into her utopian vision…if only the law would allow it.

|

|

| Source: Reuters |

“The Federal Reserve might be able to help the U.S. economy in a future downturn if it could buy stocks and corporate bonds, Fed Chair Janet Yellen said on Thursday.

“Speaking via video conference with bankers in Kansas City, Yellen said the issue was not a pressing one right now and pointed out the U.S. central bank is currently barred by law from buying corporate assets.”’

In March 2020, law or no law, the Fed conjured up ‘emergency powers’ to buy corporate bonds.

For now, I think the Fed will hold the line.

But once the recession hits and the losses start mounting up, all bets are off.

My guess is they’ll buckle.

Because ‘doing whatever it takes to support the financial system and their Wall Street buddies’ is what’s so deeply ingrained into the culture of this failed and disgraced institution.

This means what Lacy Hunt describes as the ‘dismal replay’, is still the most likely pathway on ‘the other side of bubble mountain’.

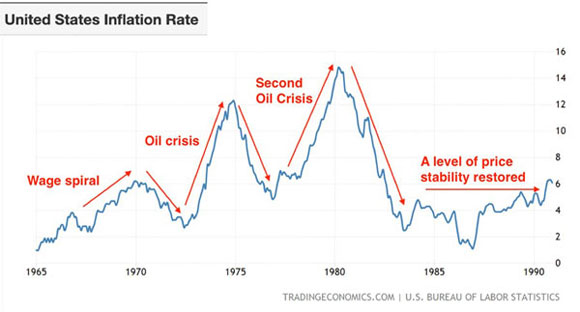

|

|

| Source: Trading Economics |

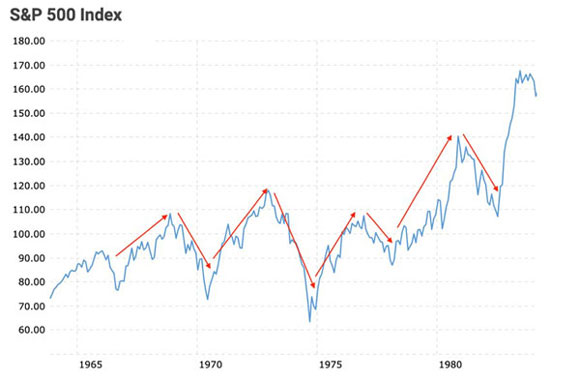

This is how the US share market performed during this period:

|

|

| Source: Macrotrends |

In a world of abundant free money, you want to own scarcity

Events of the past week have shown that cryptos are not digital gold.

They are, or were, just chips in a house-wins-all-casino run by con artists.

Cryptos were a symptom of the insanity gripping markets over the past decade.

In the cold light of day, stating the bleeding obvious seems so obvious…only gold is the real gold.

In a world where central bankers are most likely to revert to their true character — gutless and incompetent law breakers — money printing is all but assured.

Should this happen, the scarcity value of precious metals and commodities will carry a premium.

Even if the Fed surprises everyone and finds a backbone, precious metals still appear to offer fair value.

This chart, prepared by North Star, shows the ratio between SPX (S&P 500 Index) and ASA Gold and Precious Metals dating back to 1969.

When the ratio is low — the gold price is topping.

When the ratio is high — the gold price is bottoming.

|

|

| Source: CMG |

In US dollar terms, both gold and silver had a nice little boost at the start of November.

Due to the Aussie dollar gaining strength against the USD, some of this price action was lost to Australian precious metal investors.

That’s OK…we are taking a long-term approach to this exposure.

Currency movements are part of the ‘swings and roundabouts’ when it comes to precious metals.

The North Star chart indicates our exposure of 10% (evenly divided between gold and silver) appears to have been made at a time when paper assets (S&P 500) are overvalued, and hard assets (precious metals) are undervalued. That’s promising.

Regards,

|

Vern Gowdie,

Editor, The Daily Reckoning Australia