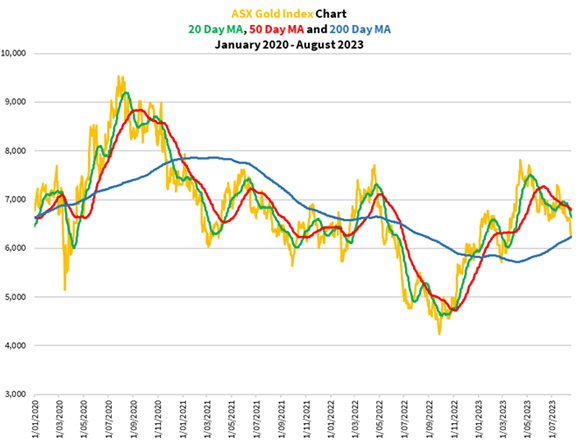

Commodities investors may’ve left the gold mining industry out in the cold after two years of frustration. There’s no denying that it disappointed on several occasions with a series of false rallies. You can see this in the figure below showing the performance of the ASX Gold Index [ASX:XGD] over the past three years:

|

|

| Source: Thomson Reuters Refinitiv Datastream |

Even though many gold stocks are trading at levels that make them look cheap, further selling pressures remain at least in the short term.

For the past two years, traders turned a quick profit by buying into the weakness and selling into the false rallies. Long-term investors had mixed success trying to profit from holding the larger producers. That wasn’t so much the case for smaller producers and not at all for the explorers.

The short-term traders trounced the buy-and-hold investors for now.

Given such conditions, ignoring gold stocks and pursuing other opportunities is easy. But if you’re looking for the opportunity for sizable gains, you’d stick to your plans.

And don’t think I’m merely clinging to a safety blanket for comfort by insisting that the buy-and-hold strategy will pay off. If you look closer at the action on the ground and in boardrooms, they’re buzzing with activity.

With the recent monumental collapse of the Evergrande Group, which filed for bankruptcy protection with a New York court last week, the ripples of this could cause an abrupt reversal to the current high-interest rate environment. That could see gold snap upwards or at least cause a flight to safety into mankind’s longest-surviving safe haven asset.

Could that result in a game-changer for gold and gold stocks? Possibly!

Tough conditions now but change can come quickly

Despite weakening economic conditions, gold hasn’t been able to fully flex its muscles. At least not yet.

The US long-term real yield is now at levels not seen since 2010 as headline inflation has slowed down. This in turn is placing short-term pressure on the price of gold as you can see below:

|

|

| Source: US Treasury, Thomson Reuters Refinitiv Datastream |

Since August, we’ve also seen a rising price of oil that could cause inflation to kick back into gear. This will also affect the profitability of mining companies because their equipment and vehicles consume a lot of diesel.

One measure I use is the gold-oil ratio which measures the number of barrels of oil that an ounce of gold buys. It’s a good indicator for determining the short-term profitability of gold producers. As you can see in the figure below, that’s also been falling recently:

|

|

| Source: Thomson Reuters Refinitiv Datastream |

So far, it doesn’t look like I’m making a case for you to invest into this space if you’re looking for opportunities.

But the insiders see it and have acted. And I’m inclined to follow them to increase my chances of reaping big rewards in the future.

So, let’s have a look at what’s going on inside the boardroom and on the ground…

Cashed up companies on the hunt…why there are more deals to come

The recent consolidations in this industry including Newmont Corporation [NYSE:NEM] acquiring Newcrest Mining [ASX:NCM], Ramelius Resources [ASX:RMS] snapping up Breaker Resources [ASX:BRB] and Musgrave Minerals [ASX:MGV], Genesis Minerals [ASX:GMD] buying the Leonora operations from St Barbara [ASX:SBM] and several mergers among the smaller players suggest that management are far from bunkering down despite the tough environment they’ve endured.

After all, the protracted period of weak investor sentiment and challenging operating conditions have allowed cashed-up companies to go shopping for cheap companies and mines. Many mid-tier (150,000–500,000 ounces of gold produced annually) and junior producers (50,000–150,000 ounces annually) have run down their resources and reserves in these recent years, so they need to replenish them to extend their mine life. Even the larger players are on the lookout, especially if their operations contain large processing plants that crunch over 5 million tonnes of ore a year.

The problems of depleting resources and insufficient ore to feed hungry mills have become urgent, given that the lockdowns and border restrictions stifled exploration and development. As a result, mining companies are now trying to make up for lost time. And the fastest way is to acquire a company or mine property, especially if they’re deeply discounted.

On top of that, the global average grade of gold beneath the ground has fallen over time. However, production costs have sharply risen since 2021 for reasons already mentioned. My internal research showed that the average all-in-sustaining cost (AISC) of ASX-listed gold producers was around AU$1,300 an ounce before 2020. It has since increased to around AU$1,700. Despite gold rising to almost AU$3,000, higher capital spending has meant that many smaller producers are burning cash every quarter rather than building a cash pile.

In terms of the scale of a profitable mine operation, the hurdle has increased. Nowadays, an open-pit mine operation needs a processing plant with an annual capacity of over 3 million tonnes of ore to be profitable. The alternative is higher-grade ore, preferably from an underground satellite deposit with a grade exceeding three grams of gold per tonne (g/t) of rock.

The boards of larger producers are spending time running the ruler over neighbouring properties and down-and-out explorers to expand their mining portfolio. Meanwhile, smaller explorers and early-stage developers are frantically increasing their exploration spending hoping not to become easy prey to a producer on the hunt.

Sometimes there’s a happy coincidence where a producer hungry for more resources comes across a cash-strapped explorer with a deposit that needs substantial funding. In this case, you’ve got a great deal. This isn’t common especially when explorers are trading at rock-bottom prices. They have been overlooked by the market in the gold bull market that began last September.

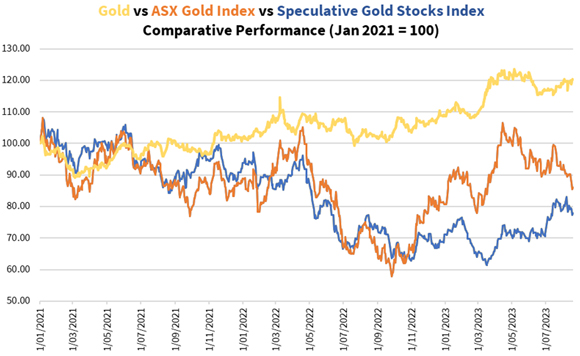

Your chance to capitalise on the opportunities like an insider

Let me show you in the figure below how there’s a clear divergence in the performance of gold, established gold producers and speculative early-stage explorers:

|

|

| Source: Thomson Reuters Refinitiv Datastream |

Now it’s over to you to decide how you want to play this opportunity.

As I said before, don’t jump in if you’re seeking a quick turnaround or can’t wait for the challenging conditions to come and go. It’ll turn you off this space possibly for good, and unfairly so.

If you’re ready, then I suggest building your gold ETF holding to use as a springboard to launch into gold producers when the trend turns around. That could become very rewarding, especially when the central banks back down and start cutting their interest rates.

If that interests you, consider becoming a member of my gold investment newsletter, The Australian Gold Fund. It’s probably Australia’s most comprehensive one-stop shop for precious metals investing.

The alternative is to try your luck and put a small amount of capital into the beaten-down explorers. Many have great assets but are deeply discounted, making them a bargain basement buy. The risks with these companies are much higher, but so could be the potential rewards when the time is right.

If got a high tolerance for risk and you’re game enough to take a couple of measured punts, join me in my premium gold speculation newsletter, Gold Stock Pro. We’ve got several explorers to choose from, with some companies setting up nicely in the coming months.

God bless,

|

Brian Chu,

Editor, Fat Tail Commodities

Comments