In 1974, the US and Saudi Arabia struck one of the most consequential financial arrangements in modern history.

Saudi Arabia agreed to price its oil exports in US dollars. In return, Washington became the region’s security umbrella.

Thus, the petrodollar was born.

That arrangement has been the backbone of the US dollar’s dominance as the world’s reserve currency.

And now it’s under serious threat.

This idea comes from the latest research note by Deutsche Bank. In it, they argue that this conflict may be the beginning of the end for the petrodollar system.

Not just because of the disruption to oil flows. But because of the damage being done to the longstanding oil-for-dollars arrangement.

Right now, Iran is negotiating with eight countries in the background. They’re offering passage through the Strait of Hormuz, in exchange for oil payments settled in yuan.

If that holds, the petroyuan stops being a theory. It becomes the reality of a bifurcated financial world.

First, How We Got Here

From 1945 to 1971, the US dollar was backed by gold. Central banks could exchange US$35 for one ounce at the Fed.

But America was spending so fast that the market was losing confidence in the convertibility of the dollar into gold.

By 1971, it held US$10 billion in gold against roughly US$60 billion in foreign claims. The math didn’t work.

On 15 August, Nixon closed the gold window. The dollar became a pure fiat currency overnight.

Nixon’s Treasury Secretary put it to the Europeans plainly:

‘The dollar is our currency, but it’s your problem.’

The world grumbled but complied. Without gold, the dollar needed a new anchor. It found one in oil.

In 1974, the US struck a deal with Saudi Arabia. Riyadh would price its oil in dollars, use US contractors to modernise its economy, and recycle the surplus into US Treasuries.

Washington provided security guarantees in return. The rest of the Gulf soon followed.

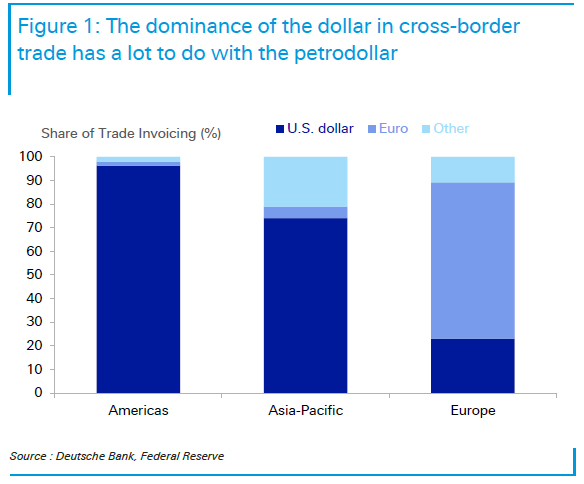

Because oil is the central input for global manufacturing and transport, the entire financial system remained fixed to the greenback.

[Click to open in a new window]

Think about it. Companies are incentivised to price their end products in dollars to hedge against their main input cost — oil.

The logic compounds from there. From corporate invoicing to banking infrastructure to central bank reserves.

Each layer reinforced the next. The dollar’s dominance became self-perpetuating.

That is the petrodollar. An arrangement that’s held for fifty years. The Iran conflict may be the moment it finally breaks.

The War Exposed the Cracks

Before this crisis, there were already challenges to the petrodollar system.

Saudi Arabia now sells four times as much oil to China as it does to the US.

[Click to open in a new window]

The shale revolution made America energy self-sufficient. That quietly removed Washington’s main reason for protecting Gulf producers.

And (as Trump is learning) after two decades of costly, inconclusive wars, the political appetite for another regional entanglement has evaporated.

Now we’re seeing the Gulf hedge its bets.

Saudi Arabia, under Vision 2030, is pushing to source half its defence locally. Other Gulf states are on a similar track.

These states have also been at the forefront of efforts to move away from US financial rails, such as Project mBridge.

That’s a blockchain payment system that connects China’s central bank with Gulf states and others.

It settles transactions entirely outside the US dollar and SWIFT and has seen a 2,500-fold increase in transactions since its pilot in 2022.

So the infrastructure to move oil payments off the dollar already exists.

That project is under pressure after Putin mentioned it as a way for Russia to circumvent sanctions. In other words, he said the quiet part out loud.

Now, that same technology has shifted to BRICS Pay.

The Petroyuan Split

This conflict may accelerate the shift to alternative payment systems by shaking three pillars of the petrodollar arrangement at once.

First, the US security umbrella. American bases and Gulf oil infrastructure have come under sustained attack.

The US has not been able to guarantee the free flow of oil through the Strait of Hormuz. That was the whole point of the deal.

Second, bilateral diplomacy has filled the vacuum. China, India, and Japan have individually negotiated tanker passage. Others will follow suit.

Third, and most significantly, is the possible yuan-for-passage arrangement that could come with these deals.

If the price of getting your tankers through Hormuz is settling in yuan, you’ll need yuan on hand. And once you are holding yuan, the incentive to invoice and save in yuan grows.

Deutsche Bank sees two paths from here. In the ‘best-case’ scenario, the US becomes the world’s dominant oil supplier by developing Western reserves.

That keeps the dollar’s role intact through supply-side control.

In the other, global oil pricing splits along trade routes. Middle East oil going to Asia is priced in yuan. Western Hemisphere oil going to US allies is priced in dollars.

That would be the most significant reshaping of the global monetary system since the collapse of Bretton Woods in 1971.

What It Means for You

The dollar’s reserve currency status is not just America’s concern. It shapes the price of everything we export.

And here, a weaker US dollar is generally good for our exporters — though it’s not always straightforward.

Zooming out, I think the current strength of the US dollar is unlikely to last beyond this crisis.

And as the petrodollar system continues to deteriorate, gold then becomes a compelling neutral reserve asset.

That means looking past its current weakness to a future multipolar financial world that’s likely to favour it.

If you want to learn more about what’s next for gold, you can check out Gold’s True Message here, from our gold expert Brian Chu.

There’s also a more direct challenge to Australia. China is our largest trading partner. It buys the bulk of our iron ore, coal, and a good chunk of gas.

If the yuan’s strength accelerates, we may increasingly be asked to settle trades in renminbi.

That shift is already quietly underway in parts of the iron ore market. BHP already settles roughly 30% of its spot iron ore trading in yuan.

If China controls the currency, the benchmarks, and the buyer cartels, our miners’ margins will be the next meal.

As Twiggy Forrest warned yesterday, China needs to ‘step away from that gun fight’.

The longer-term point is structural. The petrodollar system has funnelled global savings into US Treasuries for decades.

That’s kept American borrowing costs low and the dollar elevated. Any erosion of that system is, over time, a tailwind for the AUD and for commodity-linked assets.

The Iran conflict could be the catalyst for the erosion of petrodollar dominance and the beginnings of the petroyuan.

Fifty years is a long time for any financial arrangement to hold. The Strait of Hormuz may be where it starts to come apart.

Regards,

Charlie Ormond,

Small-Cap Systems and Altucher’s Investment Network Australia

Comments