The market is holding up remarkably well, given there’s a war on.

While you could spend all day looking at the Iran-specific dynamics of the current conflict, today I want to do something different.

Which is to look at the reason I think the US is attacking Iran.

And it’s all about China.

As we know, China is a dominant force in metals. And as I argued last week, the US was seeking to gain leverage over China by upping its control of traditional energy markets.

I think this will spur China to strengthen its hand in the metals market in the age of hard assets.

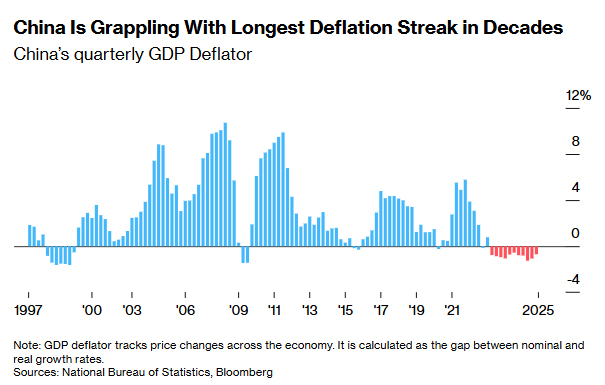

China is in a tricky spot right now.

For example, the country is on a long streak of deflation:

Source: Bloomberg

Generally speaking, in economics, this can be particularly bad for a country’s growth prospects.

Without doubt, China will be faced with some hard choices in the coming year or two.

Their set of options has definitely narrowed after Venezuela and Iran got taken off the board.

And if Ukraine gets a peace deal, those options could be even narrower.

So I suspect China will likely go back to its traditional playbook — doubling down on metals and manufacturing.

(With an added overlay of stimulus from its big banks.)

That should push additional demand into the market for commodities, particularly new-energy commodities like lithium, copper and uranium.

Which should only accelerate the US in its race to not only win on the traditional energy market front, but to continue to up its game elsewhere.

Just the other day, one of the stocks in my Fat Tail Micro-Caps service secured a major financing deal from China’s main nuclear company.

That after having previously signed a deal for offtake from a US energy utility.

Smart ASX resource companies will play a game a competitive tension with both the US and China to secure the best deal for shareholders.

At some point, you just have to take the cash.

And I expect that as both sides up the ante, this could lead to some extraordinary outcomes for ASX resource investors.

China, with its playbook for metals that it needs to prop up a slowing economy.

And the US, with its new appetite to compete with China in financing resource projects.

Again, it all boils down to chokepoints.

The places where capital must flow in order for adversaries to secure a strategic advantage.

It could be a Brazilian nickel sulphide project that is seeking a Final Investment Decision (FID).

It could be a niche water utility in the Pilbara.

Or it could be a massive lithium project in Ghana.

Point is, these chokepoints aren’t always the most obvious.

But once you start looking at the geopolitical map a certain way, their potential value in the age of hard assets becomes crystal clear.

I lay out how I’m seeing this map right now in this presentation.

Warm regards,

Lachlann Tierney,

Australian Small-Cap Investigator and Fat Tail Micro-Caps

Comments