Luxury retailer Cettire [ASX:CTT] posted rising gross revenue, sales, and improvements to the company’s EBITDA as profits came through strong for the six months ending in December 2022, the first half of the 2023 financial year.

The luxury group says that it experienced fast-paced growth, with CEO Dean Mintz commenting it has ‘been an exceptional half for Cettire’ as the group continues growing rapidly with significant profit delivery.

The results saw CTT shift from an early-morning 9% slide in share price to a gain of more than 4.5% not long afterwards, trading at $1.90 each.

So far, in 2023, CTT has increased its share value by more than 49%. This has fallen by 33% over the past 12 months.

Source: tradingview.com

Cettire revenue surges 1H FY23

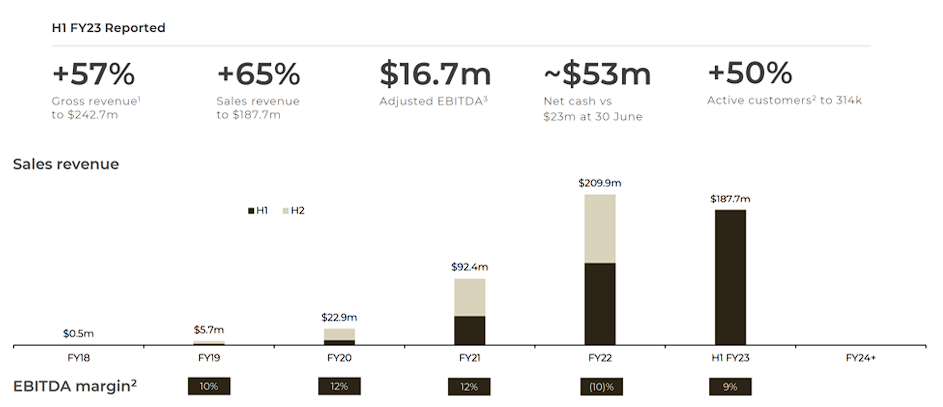

CTT provided a rundown of its financial and operational highlights for the first half of the financial year 2023, which saw an increase of gross revenue by 57% in the previous corresponding period (pcp).

Gross revenue had reached a total of $242.7 million, which was said to have been driven by growth in order volume and average order value.

Sales revenue increased 65% on pcp to $187.7 million, up from the $113.7 million reported the year before.

This jump was explained in correlation with the gross revenue increase, as well as fewer customer returns in the latest period — which declined to a rate of 22.6% versus 26.2% in 1H 2022.

The company delivered a margin increase of 90% at the same time last year, with $47 million (25.1%) of sales revenue demonstrating cost optimisation initiatives outlined in FY22.

Cettire’s improved cost structure and revenue growth assisted with improvements in operating profitability, resulting in an uptick of 8.9% in sales revenue, taking adjusted EBITDA to $16.7 million on the $9.9 million posted in H1 FY22.

Cettire cut marketing spending ($16.4 million) by around half that was a year before, but merchant fees went higher (at $7.6 million), as did administrative expenses ($7.8 million).

There were no dividends distributed for the half-year.

Mintz stated:

‘We remain laser focused on executing our strategy to maximise profitable revenue growth. I am particularly pleased that we have been able to continue our growth trajectory while cycling a period of significant marketing investment in Q2-FY22. Having successfully executed against the strategy outlined at our FY22 results, the H1- FY23 result highlights the potential of our unique business model as well as the benefits of our proprietary technology platform as we continue to scale globally.’

Source: CTT

Cettire’s reflections and outlook

The company managed with lower marketing expenses in the last half and was propelled by profitable growth, translating to $8 million in bottom-line gains.

This was a vast improvement on the $8.3 million in losses reported the year before.

CTT hopes to improve operations to the point where profitable revenue growth can be achieved while using its own funds.

The company has grown its active customers from around 209,000 to 313,000 in the last full year, and the company has added a new luxury brand from Italy, Zegna, to its collection.

Trading momentum continued in January, with sales rising by more than 80% and feeding into the group’s EBITDA-positive outlook.

Cettire looks to become EBITDA positive in H2-FY23.

Five bargain stocks

With the tailwind effects of the pandemic still lingering, the continuation of inflation, the war in Ukraine, continually rising rates and tough cost-of-living conditions…households and businesses are still feeling the pinch.

The silver lining is that in times like these, some real ASX stock bargains can emerge — if you know where to look.

Our small caps expert Callum Newman has done the hard work for you.

He’s found five of what he calls ‘the best stocks to own in Australia’ right now.

And the best part is, right now, they don’t even cost that much.

Click here to discover Callum’s top five Aussie bargain stocks.

Regards,

Mahlia Stewart,

For Money Morning