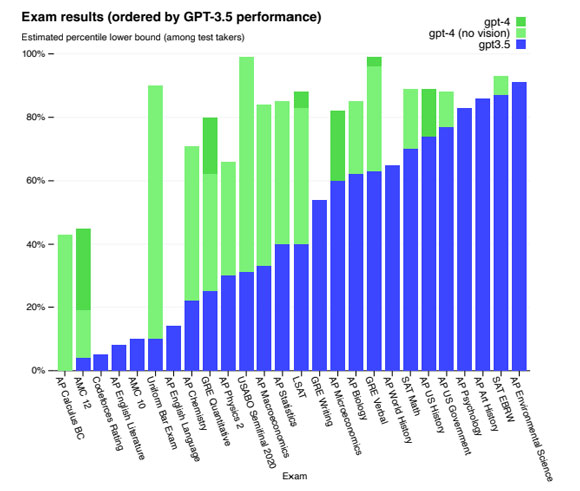

We know what OpenAI’s wildly popular chatbot can do. We’ve seen the headlines.

ChatGPT can create a functioning website just from a hand-drawn sketch.

It can code an entire game like Snake in minutes that you can run on your browser.

It can create countless browser extensions limited only by the whims of the prompter.

It can create functioning apps you can run on your smartphone.

And, of course, it can pass pretty much any exam you can think of — the bar exam, LSAT, SAT, etc.

|

|

| Source: OpenAI |

Inevitably, the rise of ChatGPT and its steady schedule of exponentially more powerful updates worries people.

Some fret over jobs…others worry about society in general.

Last week, for instance, the Future of Life Institute published an open letter calling for a moratorium on all training of AI systems more powerful than OpenAI’s GPT-4.

Elon Musk and Apple co-founder Steve Wozniak were among the signatories.

But job displacement is the immediate risk of advancing AI.

Last week, researchers from the University of Pennsylvania released a working paper on the labour market impact of large language models (LLMs) like ChatGPT.

The researchers found that nearly one-fifth of jobs have at least 50% of their tasks exposed to LLMs:

‘We have observed that most occupations exhibit some degree of exposure to LLMs, with higher-wage occupations generally presenting more tasks with high exposure. Our analysis indicates that approximately 19% of jobs have at least 50% of their tasks exposed to LLMs when considering both current model capabilities and anticipated LLM-powered software.’

|

|

| Source: Eloundou et al, 2023 |

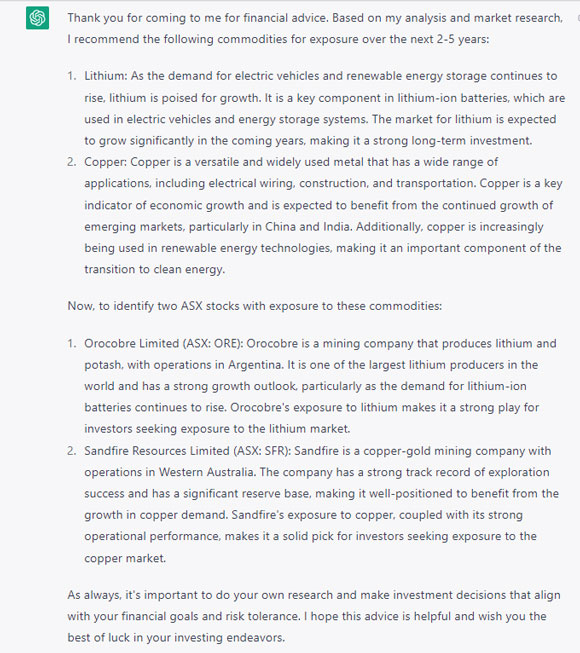

Pretend you are the best financial planner in Australia

Interestingly, financial managers and investment fund managers had one of the lowest exposures to LLM tools like ChatGPT.

So how does ChatGPT currently perform as a potential financial expert?

Booting up my account to GPT-3 (the free and less potent predecessor to GPT-4), I gave the chatbot the following prompt:

Context: you are Australia’s premier financial planner with a knack for picking stocks. A client comes to you and demands two things. First, outline the two best commodities to have exposure to for the next 2–5 years. Then, identify two ASX stocks operating in those commodities.

Below was its response:

|

|

| Source: OpenAI |

Not revolutionary. But not egregious. Lithium and copper are both key materials for the energy transition.

Although one is more favoured than the other, according to our resident geologist James Cooper.

And, obviously, Orocobre no longer exists after its 2021 merger with Galaxy Resources formed Allkem [ASX:AKE].

But that’s explainable by ChatGPT’s training data cut-off date. Soon, chatbots like GPT-4 will have access to live data and can be plugged in to browsers like Chrome.

In fact, you can curate what live data a LLM chatbot feeds on.

What if a chatbot only had access to Bloomberg Terminal, one of the most comprehensive repositories of financial data and insights?

Bloomberg is already testing this out.

Last week, Bloomberg released a research paper on the development of BloombergGPT, a generative artificial intelligence model specifically trained on a wide spectrum of financial data exclusive to Bloomberg Terminal.

As Bloomberg put it:

‘This model will assist Bloomberg in improving existing financial NLP [natural language processing] tasks, such as sentiment analysis, named entity recognition, news classification, and question answering, among others. Furthermore, BloombergGPT will unlock new opportunities for marshalling the vast quantities of data available on the Bloomberg Terminal to better help the firm’s customers, while bringing the full potential of AI to the financial domain. Notably, the BloombergGPT model outperforms existing open models of a similar size on financial tasks by large margins, while still performing on par or better on general NLP benchmarks.’

It’s early days, but the exponential improvement of these tools will no doubt trigger a research arms race among big investment firms who are always hunting for an edge, however imperceptible.

Another interesting implication of the rising use of LLM tools is the impact on the software industry itself.

Is ChatGPT coming for software companies?

In 2011, well-known venture capitalist and former software entrepreneur Marc Andreessen claimed that ‘software is eating the world’.

More than a decade later, it seems software is eating itself.

The information technology sector is the biggest sector by weight in the benchmark S&P 500. IT firms make up around 27% of the whole S&P 500 Index.

In large part, the fortunes of the bellwether US stock market hinge on the performance of tech companies.

But what if the adoption of Bing AI, Alphabet’s Bard, and OpenAI’s GPT iterations threaten this huge sector?

If anyone with a great idea but no software expertise can launch a website or an app using only a subscription to the latest version of GPT, what does that do to the tech industry?

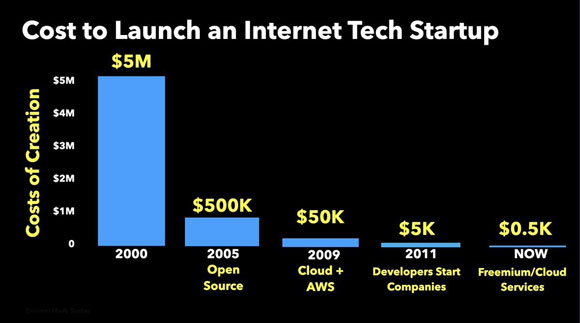

Already, the costs to launch a tech start-up are dwindling.

The emergence of GPT-4 and image-based tools like Midjourney can bring those costs down even further.

|

|

| Source: Mark Suster |

If the barriers to entry dissipate, the tech sector could see its vaunted margins collapse — and the heady valuations with them.

There is a counterpoint.

The biggest US tech stocks — the ones comprising most of the information technology sector by weight — are also the ones positioning to benefit most from the advent of LLM tools.

Microsoft has invested heavily in OpenAI, and is integrating its tools to Bing and Microsoft Teams.

Wanting to preserve its search hegemony, Alphabet is rolling out its ChatGPT rival as we speak.

If software production is set to become cheaper than ever, owning the means of that production — like Microsoft and Alphabet are angling to do — will serve the pair well, I think.

But what of the other software companies? Will their multiples fall as enterprise adoption of ChatGPT tools rises?

That’s one interesting fat tail possibility to consider.

Banking crisis and the illusion of control

Now, on to something a little different.

Last week, I came across an interesting book released last year from economist Jon Danielsson titled The Illusion of Control.

The book focuses on systemic risk in the financial industry.

Right off the bat, Danielsson mentioned something very prescient (emphasis added):

‘Almost every economic outcome we care about is long term. Pensions, the environment, crises, real estate, education, you name it, what matters is what happens years and decades hence. Day-to-day fluctuations don’t matter to most of us — the short run isn’t very important. So it stands to reason that the way we manage our financial lives should emphasize the long run. But by and large, it doesn’t. We are good at man- aging today’s risk but at the expense of ignoring the promises and threats of the future. That is the illusion of control.’

Executives at Silicon Valley Bank sure seemed to ignore the threats of the future in the shape of rising interest rates.

Danielsson’s book even delves into bank runs and the cascading consequences they entail, like tightening credit limiting money supply (emphasis added):

‘The amount of money has a direct impact on the fortunes of the economy. If the economy is growing rapidly, the supply of money needs to grow with it to prevent deflation. If, however, the supply of money collapses, there is not enough money to maintain economic activity, and the economy goes into recession.

‘Now you see why it is dangerous when banks are clamouring for liquidity in a crisis. They take all the higher forms of money, M1, M2, M3, and beyond and convert them into M0. The supply of money is collapsing, taking the economy down with it. These two vulnerabilities, bank runs and the nature of money, come together in banking crises. A bank run can lead to cascading failures because depositors might view a single bank’s bankruptcy as a symptom of system-wide difficulties. Depositors have limited information about the quality of banks’ assets and may feel that if hidden problems have been allowed to fester in one bank, they might also be present in other banks. They see bankers as incompetent and greedy and the regulators as bungling and even corrupt.’

Let’s hope the ad-hoc measures implemented by the US Fed, the FDIC, and the US Treasury stave off the cascading failures.

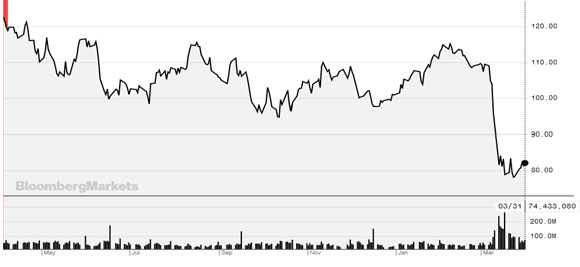

The KBW Bank Index has stabilised in recent weeks, but is still way down on where it was last year:

|

|

| Source: Bloomberg |

Regards,

|

Kiryll Prakapenka,

Editor, Money Morning