Here’s a couple of things I’m thinking about today…

1) Bubble, bubble, bubble…

I’ve been writing about finance for nearly 14 years. If there is one word I hear over and over again, it is “bubble”.

We’re told we are in an AI bubble. Before that it was a bitcoin bubble. Before that it was an Aussie property bubble. And before that it was a China bubble.

Investors and commentators are obsessed with spotting bubbles!

They’re downright shite at it, too. None of these articles and conversations have achieved anything, as far as I can tell.

Bitcoin, China, Aussie property and now AI are all going on their merry way.

One thing we DO know about so called “bubbles” – periods of speculative excess that result in a crash – is they’re usually fuelled with borrowed money.

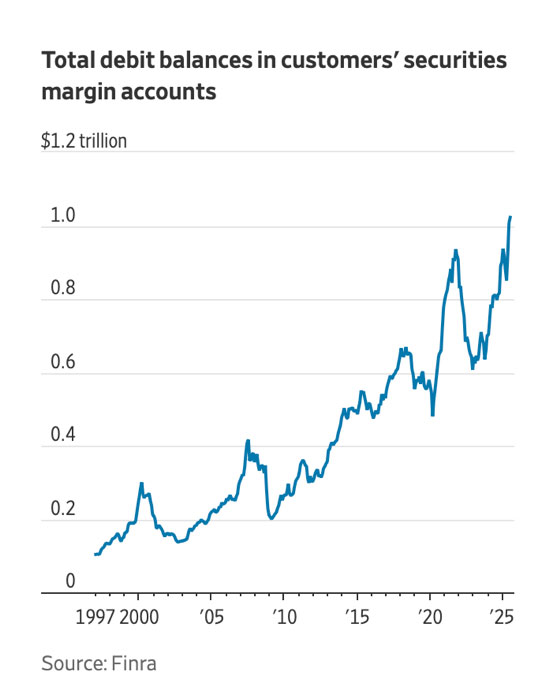

That’s why this chart in the Wall Street Journal caught my eye this week.

It shows US “margin” debt – borrowed money used to buy shares – is at a record high.

| |

| Source: Wall Street Journal |

In theory, this is a danger because the fragility of the market increases if interest rates rise or something else causes investors to sell out of the market to reduce their borrowing.

It could also be a warning sign for US stocks.

A trillion dollars of margin debt sounds like a lot of money. I suppose it is a lot of money.

But we have to compare it to the total market capitalisation of US stocks, which is about US$60 trillion.

Margin debt is therefore only about 2% of the total market cap for US stocks.

I was curious to see how this stacked up, as a percentage, against other times in history.

Here’s one chart I found…

| |

| Source: First Trust |

Today is actually pretty modest, at least as far as the last 30 years go.

That said, it’s not hard to imagine this heating up if Trump gets his wish – and forces the Fed to drop rates.

Unnaturally low rates were part of the fuel that took the market to its 2007 top – with margin debt soaring right alongside of it.

In other words, maybe don’t worry about it today – but watch this space.

2) One of my recommendations, Beacon Lighting ($BLX), is out with its earnings this morning.

I recommended BLX back in early 2023 for subscribers to Australian Small Cap Investigator.

You could also read about that idea later, in November 2023, on public investing forum LiveWire. You can see that here.

Back then I wrote…

“Right now, you have a chance to accumulate small-cap shares while they are trading at depressed prices…

“The current interest rate squeeze will likely be forgotten [by 2025 or 2026]. Who knows where consumer confidence and spending will be by then? No one.”

BLX is now up 100% since 2023.

However, it’s interesting to note that BLX has not jumped on today’s results.

We can say BLX has delivered to expectations. Is there anything else we can take from this?

Yes – I think so.

Back in 2023 you had a look at “bear market” pricing.

I’m talking about established firms like BLX that were going cheap because sentiment and expectations were so terrible.

That kind of pricing is not really available anymore.

We can roughly say, in this instance, that BLX is fairly valued. But it’s unlikely to double again in the next two years.

What does this mean?

High returns can only come, from here, to my mind anyway, from going further out the risk curve.

To get a stock to double now you need to rely on it doing something out of the ordinary…something that isn’t priced in…and NOT based off a market ‘reflation’ like we’ve seen the last few years.

Beacon’s business hasn’t changed THAT much since 2023.What has changed is the multiple investors are prepared to pay. That has gone from 10x to 20x – hence the doubling in shares.

Essentially, the best “big” buying opportunity is gone.

I’m not saying you can’t make money now. Far from it.

There are and will be plenty of opportunities.

But you’ll need to think more strategically, more deeply, I believe, than just swooping in and buying up good assets.

Or, you’ll need to embrace more risk, and back companies building out their future and creating value that the market marks up as it happens.

That still puts small and microcap stocks in play.

Established players like BLX aren’t the bargains like they were. The same for the REITs we chatted about earlier in the week…and most of the other blue chips.

Of course, from time to time, there are always unique opportunities that appear, if you see and understand the context of what’s happening.

But a lot of fund managers have posted big returns the last financial year.

That’s the reflation trade at work. That kind of performance is hard to maintain as the bull market rolls on.

The “upside”, if that’s the right word, is you probably feel less scared and intimidated than 2 years ago. The market is certainly less volatile.

It just means we all have to work harder to get those big returns. Nobody ever said it was easy.

Best Wishes,

Callum Newman,

Small-Cap Systems and Australian Small-Cap Investigator

***

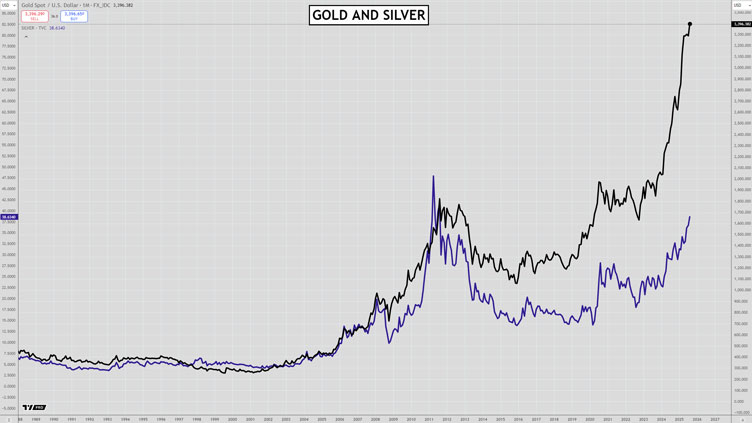

Murray’s Chart of the Day –

Gold and Silver

Source: TradingView

[Click to open in a new window]

The image above shows you the monthly line charts in gold and silver.

Gold is about to close the month out with a new all-time high monthly close.

Silver is also closing the month strong and looks like it wants to keep rallying towards its 2011 high near US$50.

Trumps moves on the Fed will be enough to keep gold and silver well bid.

The thought of a property developer getting his hands on the interest rate lever for the economy is a scary prospect.

The US dollar has been treading water for a few months after getting dumped earlier in the year.

Another wave to the downside could erupt at any moment and Trumps actions will encourage that outcome.

The Jackson Hole speech by Fed Chairman Powell has already increased expectations that rates will fall soon.

The sacking of a Fed governor for spurious reasons and the instalment of a puppet next year as Chairperson is big news.

There will be unintended consequences if Trump gets his way and rates fall sharply.

My view is that there will be a further steepening of the yield curve as expectations for future inflation build.

Perhaps Trump can spark a huge rally in stocks as a result. Banks will certainly be big winners the steeper the yield curve gets.

But mortgage rates could remain stubbornly high since they are priced off 10-year bond yields.

Trump of course has his eye on funding government deficits with cheap debt. They will issue plenty of short-term debt and strong arm the Fed into lowering rates.

Front loading all of their debt and keeping long-term issues to a minimum may take some pressure of long-term bond yields.

But in the end it may take another operation twist from the Fed to stop the sharp rise in yields in long-term debt as inflation expectations rise again.

These events could be the spark for an exponential rise and then crash in stocks over the next few years.

So the name of the game will be riding it as hard as possible, but with one eye on the exits at the first signs of trouble.

Regards,

Murray Dawes,

Retirement Trader & International Stock Trader

Comments