There’s been some heavy selling in the iron ore sector of late, so I thought we’d spend some time profiling this important commodity.

Considering mining behemoths like BHP, Fortescue, and Rio Tinto make up a large chunk of Australia’s large-cap indices, there’s a good chance your investments are tied to this commodity in some way.

Not so long ago, things were looking very rosy in this space.

The price of iron ore was perhaps one of the few things making headlines (outside of COVID) for a good part of 2021. As prices breached a record US$200 per tonne, our terms of trade were the envy of the world.

But on the back of ongoing market volatility through 2022, this commodity has well and truly faded from the limelight.

Fears of global recession continue to impact prices.

After sitting at more than US$200 per tonne for much of 2021, prices have plummeted to around US$90 this year.

That’s a drop of almost 60%!

Right now, the prospects don’t look good…that’s according to the most recent forecast released by ANZ’s team of analysts…

With the doom and gloom surrounding a potential China property crash, global recession, and ongoing stock market falls, it seems the analysts at ANZ might be succumbing to the general fear of the masses.

So should we be paying attention?

Perhaps, but history tends to suggest that mainstream forecasts, those that come out of banks, government departments, and major stockbroker firms tend to work better as an ‘inverse indicator’.

After all, these experts have a pretty dismal track record…their predictions of a housing market crash in 2020 on the back of the ‘pandemic panic’ was more of a panic projection than anything else.

Looking back, this was actually an excellent time to buy property. Prices leaped across the nation with some neighbourhoods recording gains of 50% or more.

But if you allowed mainstream economists to dictate your thinking, you would’ve sat on the sidelines watching this once-in-a-decade opportunity pass you by.

It seems important junctures in financial markets bring to light the shortcomings of conventional forecasters.

Never more so than our last major financial catastrophe.

It was the then US Federal Reserve Chairman Ben Bernanke who infamously pronounced the strength of the US economy just months prior to the global financial meltdown (emphasis added):

‘The global economy continues to be strong, supported by solid economic growth abroad. U.S. exports should expand further in coming quarters. Overall, the U.S. economy seems likely to expand at a moderate pace over the second half of 2007, with growth then strengthening a bit in 2008 to a rate close to the economy’s underlying trend.’

Again, another major failing at an important confluence in economic history.

It’s fair to say that the mainstream economists’ track record is not solid.

Now, this brings me to our own federal government’s latest budget figures…AND, as always, it follows the conventional sentiment of the day.

So, not surprisingly, its forecasts are extremely bearish on the outlook for Australia’s two major exports.

It includes a prediction for iron ore prices falling 40% from today’s current prices, to just US$55 per tonne…as well as a staggering 83% decline for thermal coal!

If you’re shocked by that projection, you’re not alone. Prices for thermal coal currently sit around US$360/tonne but the government expects this to be US$60/tonne sometime next year. According to our financial leaders, coal is on the cusp of recording one of its worst annual performances on record!

These are simply astonishing projections that demonstrate a department totally caught up in the fear of the day. We’re told to trust these experts, yet such grim predictions are nothing short of reckless.

But perhaps they present an opportunity for you, so let me explain…

The future of iron ore boils down to this

When it comes to iron ore, the China story is the only game in town.

But as you’re no doubt aware, the Chinese economy has been stuck in a two-year COVID lockdown. This continues to drag on far longer than anyone expected.

But what happens when China inevitably ends its self-imposed economic shutdown?

As a resource investor, it’s time to seriously consider the implications of China’s reopening and begin strategising your portfolio accordingly.

In my mind, the market is overly fixated on US Treasury rate hikes. This issue continues to be the primary driver affecting almost all equities.

You see, markets continue to salivate to the words of a select few in the US Treasury Department.

One minute it’s faltering on the Fed’s commitment ‘to attack inflation head on’, the next it’s rising due to some data that indicates weakening conditions and a chance that central banks might ‘pivot’ on aggressive rate hiking.

It’s all folly and noise. A distraction from the more important issues, particularly for us here in Australia.

I think you’d agree that very few market commentators are taking notice of a much more important factor, the inevitable reopening of the world’s second-largest economy, China.

So, let’s dive in and take a look for ourselves…

Chinese imports indicate growth ambitions

It comes as no surprise that the Chinese economy has slowed markedly since lockdowns were enforced…the International Monetary Fund (IMF) forecasts China’s GDP will drop to just 3.2% this year, down from the 8.1% growth recorded in 2021.

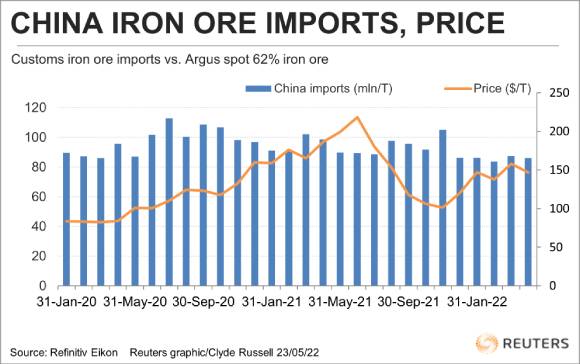

But despite the enormous slowdown, China continues to import iron ore at a pace equivalent to pre-pandemic rates. See for yourself below:

|

|

| Source: Reuters |

In the face of immense cuts to manufacturing and construction across the Chinese mainland, imports for iron ore are still as strong as ever, so what gives?

In my opinion, China is capitalising on lower commodity prices to boost its inventories.

This suggests one thing…China is preparing to reignite growth for manufacturing and building as soon as lockdowns end.

In fact, it’s feasible that the purpose of lockdowns is not to prevent the spread of COVID, but rather buy the government more time to build stockpiles of key commodities including iron ore, coal, copper, oil, and gas.

This would help alleviate inflation pressures that have inflicted the West and will inevitably affect China when it opens its economy.

I know this might sound like a wild statement, but why would China continue to boost its internal supplies of key commodities while its economy sits idle?

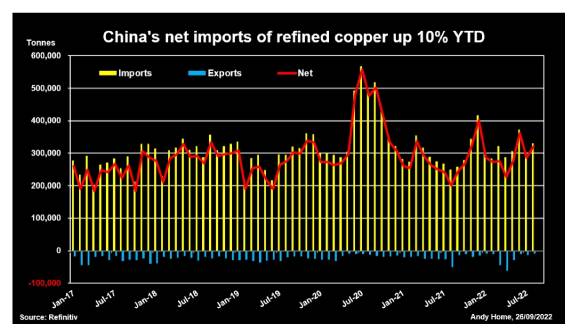

Copper imports into China follow a similar trajectory to iron ore. As this chart from Refinitiv shows you, imports are up 10% in 2022:

|

|

| Source: Refinitiv |

Just like iron ore, copper demand is heavily tied to construction and manufacturing.

With the IMF forecasting China’s GDP slowing from 8% to just 3% in 2022, it clearly shows China is looking BEYOND lockdowns. Something our economists struggle to comprehend.

In my mind, there’s simply no way that the Chinese Government is bracing for a major long-term economic slowdown while increasing imports for copper. At the very least, it’s preparing for a situation that brings growth back to pre-pandemic levels.

So when CAN we expect this long-awaited reopening?

It’s difficult to say for sure. The Chinese Communist Party is pretty tight-lipped regarding giving away its future plans.

But the world’s largest miner, BHP, has uncovered evidence that the government may be looking to boost the nations property market ahead of a future opening. According to the company’s latest economic and commodity outlook (emphasis added):

‘We are seeing some green shoots in China by way of property sectors, so increased sales and increased completions, we are not yet seeing that pull through to an increase in housing starts but we are seeing some more supportive policy, with encouragement being given to the banks to relax some of their lending practices for the property sector.’

With China accounting for around 50% of global mineral imports, BHP has a strong vested interest in what China does NEXT.

But actions speak louder than words.

Right now, China is NOT pulling back on imports for key commodities despite pausing economic activity.

It’s simply doing what the West failed to do. Proactively preparing its economy for growth while minimising the potential inflation impact arising from supply bottlenecks.

Will this reopening be an immediate ‘all-out’ resurrection of the economy or a staged effort allowing leadership to monitor growth and inflation while boosting inventories for commodities?

Who knows, but I believe the latter is more likely.

The one thing you can count on, however, is that the world’s second-largest economy IS getting ready…the engines are starting to rumble.

Which brings me to this question: Is YOUR portfolio ready for what happens next?

This is a great time to capitalise on bearish sentiment and accumulate quality mining stocks.

2023 could be an exciting and rare window for far-sighted Australian investors.

Much like 2002 and 2003.

Which is why I’ve been collaborating with Greg Canavan and James Woodburn on an ambitious new resource investing strategy.

With my previous experience in finance and geology, I plan to give you the edge from an insider’s perspective.

We’re going to delve deeply into Australia’s most promising resource stocks for this next phase of the commodities cycle. A phase I call ‘The Age of Scarcity’.

No one else seems to have quite cottoned on to the scope of opportunity here.

And that’s your advantage.

Keep reading The Daily Reckoning Australia for more. We’ll be going full force on this theme starting Monday.

Regards,

|

|

James Cooper,

Editor, The Daily Reckoning Australia

Comments