Shirt tucked. Best jacket on. Notes printed. Pen at the ready.

I’m tense.

I’m about to interview the ‘most positive man in finance’.

My assignment is to grill him.

Positivity cannot go unquestioned!

Fidgeting in my seat, I run through the talking points.

‘On a real, per capita basis, Aussie retail sales are down over 4%. Does that concern you? ’

‘What about the macroeconomic headwinds?’

‘How can earnings rise in a higher for longer environment?’

‘What about the equity risk premium?’

And Callum Newman, special guest on this week’s episode of What’s Not Priced In, had a ready answer each time.

As for the equity risk premium, he was blunt.

‘Frankly, I don’t give a toss.’

In this fun episode, I grill our small-caps expert Callum about his optimistic outlook for Aussie small caps. Topics discussed:

- Why Greg called Callum the ‘most positive man in finance‘

- Why Callum thinks ‘all the ingredients are there for the Aussie stock market to start firing on all cylinders‘

- How macroeconomic conditions inform (or don’t inform) Callum’s thinking

- Strength of iron ore price and why Callum remains bullish

- Lessons from the lithium hype cycle

- Why Callum ‘does not give a toss’ about the slim equity risk premium

- Principles of sound small caps investing: focus on businesses growing faster than wider economy

- ‘Astonishing value’ in the small-cap sector as market continues to misprice solid, profitable businesses

- Callum’s watchlist: Mount Gibson Iron [ASX:MGX], GQG Partners [ASX:GQG], Maas Group [ASX:MGH], and Resimac [ASX:RMC]

- Is the generative AI hype warranted and is there any AI ideas on the ASX?

Tale of two updates

Optimism versus pessimism.

Two trading updates offer a nice illustration of the conflict.

One from retail giant Harvey Norman [ASX:HVN]. And one from online furniture retailer Temple & Webster [ASX:TPW].

Let’s turn to Harvey Norman first.

Between 1 July and 25 November, Harvey Norman’s total sales fell 7.8%.

Comparable sales were down 8.7%.

But the retailer’s Australian segment fared worst.

Harvey Norman’s franchisees saw comparable sales fall 11.9%!

Pessimists vindicated!

Harvey Norman’s flagging sales jive with recent retail turnover data from the ABS.

Retail sales came in softer than expected in October, falling 0.2% against an expected 0.2% gain.

Annual sales growth is an anaemic 1.2%.

When you factor in population growth and retail price inflation, sales are down about 4.5% on a real, per capita basis.

That doesn’t sound positive.

Temple of Boom

But then we had the trading update from Temple & Webster.

In the same stretch between July and November, the online furniture retailer saw sales rise 23% year-on-year.

Sales even accelerated between October and November, up 42% YoY.

Management proudly said the firm continues to grow market share ‘at a time when the overall furniture and homewares market is down’.

The company also reaffirmed its EBITDA margin guidance for FY24.

Temple & Webster is up 30% this week.

Chasing secular growth

But what do the two contrasting sales updates reveal? What is the takeaway?

First, let’s digress by mentioning the market’s reaction to Harvey Norman’s trading update.

The stock went up.

Harvey Norman rose over 4% following the announcement.

That suggests slumping sales were largely priced in. The market is discounting current soft consumer demand and looking ahead.

Exactly how far ahead is something I discuss with Callum.

That’s the thing with markets.

The macroeconomic situation today can be justifiably gloomy. But if the market has already accepted it, what matters is the market’s view of tomorrow.

But back to the original question. What’s the message behind the tale of the two updates?

It’s not a stock market, but a market of stocks.

I’m sure you’ve heard Greg say this that on the pod before.

Or as Callum wrote recently, ‘there is always opportunity, every year, even if the averages don’t show it.’

The key is to focus on growing businesses who don’t give a hoot about real per capita sales declines.

Harvey Norman is a mature company with a big presence. Its size means it now grows more or less in line with the wider economy.

If the economy slows, so too will Harvey Norman’s sales.

But there’s always businesses who are growing faster than the aggregate economy.

I cited research from Morales and Kacher a while back:

‘[Winning stocks] represent the leading edge of what is happening in the economy with respect to the new industries, new economic developments, and other themes that serve as essential drivers for the economy at any given point in time.’

Temple & Webster is benefiting from the secular growth of consumers shifting traditionally offline purchases online.

The company is also trying to benefit from the AI craze.

This week our venerable Macquarie Dictionary announced its People’s Choice Word of the Year winner was generative AI.

It’s a winner in the corporate world, too.

Temple & Webster thinks it’s ‘well-placed to benefit from … the revolutionary potential of new technologies such as generative AI’.

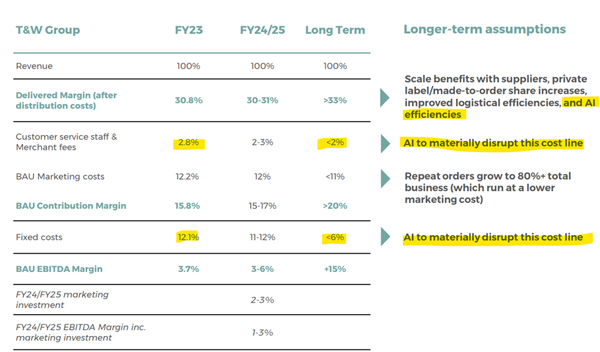

| |

| Source: Temple & Webster |

I doubt if ChatGPT can help a furniture retailer bring fixed costs down ‘materially’.

But the point is this.

There’re always businesses beavering away at the frontiers of the economy. And at the frontier, wider macro concerns rarely matter.

In Callum’s parlance: they don’t give a toss.

Enjoy the episode!

Regards,

|

Kiryll Prakapenka,

Editor, Fat Tail Daily

PS: Leave a comment or question you’d like us to address on the pod. Either leave a YouTube comment or email us at wnpi@fattail.com.au

Comments