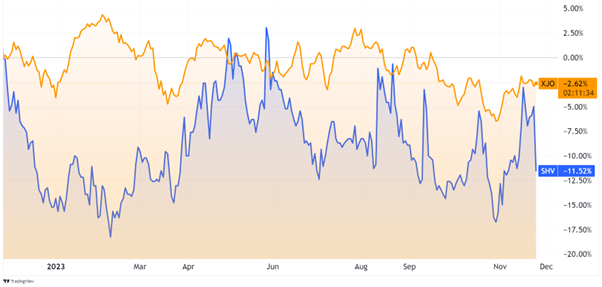

Australia’s second-largest almond grower, Select Harvests’ [ASX:SHV],shares fell heavily today, down –6.87%, trading at $4.07 per share as the company’s tough fiscal year was revealed in its latest report.

If you can remember the last couple of summers’ terrible weather, it comes as little surprise that growers faced challenges throughout FY23.

The company has battled low-quality almond crops and volumes from the poor weather. SHV cut production estimates for 2023 back in March after what was described as an unusually colder and wetter condition throughout the last growing season.

Share prices have struggled to recover to the $5.56 highs seen in September last year, with shares down 11.50% in the past 12 months as almond prices sit at a near-decade low.

For now, almond prices continue to fall, down roughly -6% from last year. But expectations of rising demand and a strong El Niño summer should help the next harvest in January.

Source: Trading View

A year of hardships

The past fiscal year was marked by a stark contrast from the previous one, with Select Harvests plunging from a $4.8 million profit in FY22 to a substantial net loss of $114.7 million in fiscal 2023.

This downturn can be attributed to a combination of unfavourable factors that usually hit growers only once a decade.

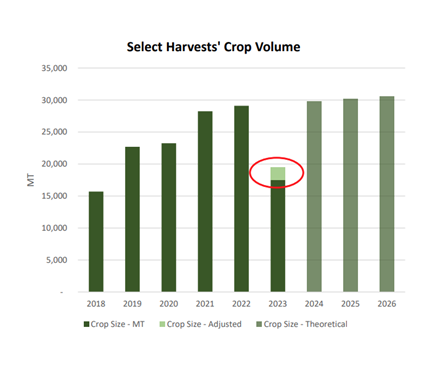

In FY23, Select saw major flooding events across its farms pre-harvest. As a result, almond crop yields took a significant hit, dropping by 30.2% to 19,771 metric tonnes. At the same time, almond prices fell to A$6.42 per kg — adding to the financial strain.

Source: Select Harvests

The company then faced the impacts of inflation, like many Australian producers, with production costs increasing by $25 million.

The lion’s share of that was from rising fertiliser costs. Sanctions of Russia and Belarus, as well as export restrictions from China, helped drive up the cost of natural gas used in production as well as the raw product.

In total, the company invested to produce 30,000 metric tons (MT) and produced only 19,771MT. This meant a $24.5 million write-down of 2022 crop inventory and a $26 million goodwill impairment.

SHV’s net loss for the 12 months through September stood at –$114.7 million, coupled with an operating cash flow deficit of $8.2 million.

Managing Director David Surveyor commented on the outlook, saying:

‘Despite two challenging years, the company is well placed. The forecast of warmer, drier conditions leading into our harvest period and likely improved crop quality profile–combined with a return to long-term normalised crop production volumes–is welcome and will further improve that position.’

Outlook for Select Harvests

The company has faced a perfect storm of adverse weather conditions and challenging market dynamics, leading to significant financial setbacks.

However, looking ahead to fiscal 2024, there’s a glimmer of hope on the horizon, with improved conditions and strategic maneuvers poised to turn the tide.

The company anticipates a rebound in crop volumes and quality thanks to El Niño bringing a hot summer.

The company is backing this forecast with investments in increased processing capacity at its Carina West facility. The company says it will be upgraded to a capacity of 40,000 metric tons.

In an effort to manage rising costs, they will also source over 9,000MT of almonds from external growers, which the company said will help improve margins.

These margins will be an important point for the company to improve as almond prices sit at a decade low.

Source: Select Harvests

A ray of hope for prices could be demand from the North American market, as their last season was also a wet and wild one.

Hurricane Hilary took out approximately 37% of the total almond crop there in August. A loss just shy of US$1 billion.

Their loss could be Select’s gain, but the company must maintain tight cost controls to fully capitalise on the harvest ahead.

Select Harvests’ year was fraught with challenges, but the company’s proactive strategies and the anticipated market improvements in 2024 paint a picture of resilience and potential recovery.

The focus is now firmly on maximising the yield and quality of the 2024 crop, maintaining stringent cost control, and enhancing cash flow.

With these measures in place, Select Harvests is poised to navigate the uncertainties of the agricultural sector and emerge stronger in the coming year.

Why you can’t rely on nature for everything

The sun can make or break a company’s profits, like Select Harvests. It can also play havoc on our power systems.

Renewable energy sources tend to fluctuate in generation as they rely on natural forces we can’t control.

The sun doesn’t always shine, and the wind doesn’t always blow.

Similarly, the demand for power changes throughout seasons and times of day. Often, these requirements can be at direct odds with renewable power sources.

With the flawed intermittent nature of renewable energy, many expensive solutions are required to fill the gaps so that heavy industry, manufacturing, or homes can get reliable power when needed.

This gap is known in the solar industry as the ‘duck bill curve’.

Source: Synergy (WA Estimates)

During the day, when demand is lowest and the sun is shining the brightest, solar can overload transmission lines that are designed for one-way electrical flows, leading to instability in grids.

At the head of the duck, these grids are again put under stress as demand rises and solar output falls to nil.

To make up for these shortcomings, expensive solutions are touted for new battery storage solutions and more than 10,000 kilometres of new transmission lines to carry these renewables.

That’s a ninefold increase in transmission lines that will also require batteries and new infrastructure to manage the needs of renewables.

And all of this is supposed to come in the next seven years.

If only there were a clean and consistent power supply that we have an abundance of in Australia…

Well, there is! It’s nuclear and it will be our future.

Our Editorial Director Greg Canavan has been looking into the cost of Australia’s transition to net zero.

He believes that a quick turnaround to nuclear is coming, like the one seen in France this year.

We’ve already seen uranium prices hit 15-year highs in the past weeks, and the momentum is continuing.

He’s found five ASX uranium picks that he thinks could benefit from the change.

Check it out here.

Regards

Charlie Ormond

For Fat Tail Daily