Live ASX News | ASX Set to Fall, US Fed Hikes 25bp, NAB’s Cash Profit Rises 17%

Almost all YTD S&P 500 gains are due to just five stocks and that’s bad

The following is an extract from The Gowdie Advisory service run by veteran financial planner Vern Gowdie.

In the early 1970s, the Nifty Fifty were the go-to stocks, the ones the investing public mistakenly believed you could not go wrong buying.

But, in 1973 and 1974, when things went South on Wall Street, the overpriced Nifty Fifty suffered greater losses than the broader market (as measured by the S&P 500).

The lesson from markets past is that no matter how strong the household names might be, they are NOT invaluable…they do have an intrinsic value based on prevailing economic conditions, interest rates, earnings, and multiples of those earnings.

This brings us to today’s ‘Fabulous Five’ — a far narrower base of blue chips than the Nifty Fifty.

The S&P 500 is an index tracking the stock performance of 503 of the largest companies listed on stock exchanges in the US.

11 companies constitute approximately 30% of the index.

And, if we narrow that down a bit further, five (just five) companies make up 20% of the index.

The other 490-plus companies make up the balance of the index.

Source: Slick Charts

To help us determine when a share market advance is broad or narrow-based, we can compare the Weighted Index (S&P 500) with the Equally Weighted Index (where the price movement of any company constitutes a 1/503 influence on the index).

This chart compares the year-to-date (YTD) performance of the S&P 500 Index (blue line) with the S&P 500 Equally Weighted Index (purple line).

Since 1 January 2023, the S&P Index has posted a 7% gain, whereas the Equally Weighted Index is only up 0.6%. Why the 6.4% difference?

When we crunch the numbers, we see almost ALL the S&P 500 gains since 1 January 2023 are due to the price movement of just five stocks.

Which means the other 498 companies in the index have collectively gone nowhere.

Investors are making the same mistake they did in the early 1970s. They think they can’t go wrong buying the household names with a US recession looming.

UK competition regulator to review AI chatbot technology

Here’s an interesting development.

The Financial Times has just reported that the UK competition watchdog will review the artificial intelligence sector, with a special focus on the models behind generative AI chatbots like ChatGPT.

Speaking with FT, the UK’s Competition and Markets Authority chef Sarah Cardell said her department will assess ‘what kind of guardrails, what principles, we should be developing in terms of ensuring that competition is working effectively and consumers are being protected’.

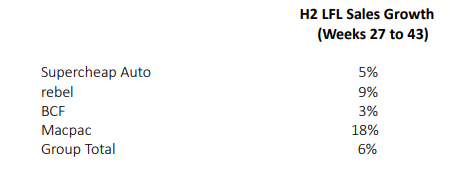

Super Retail down on downbeat outlook for the rest of FY23

Super Retail (ASX:SUL) is down 7.5% in late Thursday trade after the market digested a trading update released after-market on Wednesday.

Super Retail noted sales growth is moderating in the second half of the fiscal year, with group gross margin trending 10bps below 1H23.

SUL noted inflationary pressures still persist despite offshore freight costs returning to pre-pandemic levels. But wages, rent and energy expenses are still hurting Super Retail’s cost of goods sold in the second half.

Super Retail’s BCF brand registered only 2% sales total sales growth in the first 43 weeks of FY23 versus FY22, with ‘aggressive mark down activity from competitors’.

Macpac was the best performer, posting total sales growth FY23 YTD of 38%.

Still, the 2H23 sales growth is lagging 1H23. Here’s the 2H LFL sales growth data Super Retail revealed yesterday.

And here’s SUL’s data for 1H23.

Small-cap fintech Butn makes surprising 52-week high

Small-cap fintech Butn (ASX:BTN) hit a 52-week high today, a surprising development amid the wider macroeconomic gloom (which usually sours interest in small caps).

Butn debuted on the ASX in July 2021 at an issue price of 50 cents and fell over 80% over the following year as investors fled riskier assets.

However, since an all-time low of around 9 cents a share in June 2022, the BTN stock is up 180%.

Butn is a B2B funder focusing on invoice financing and has dabbled in the once-trendy BNPL.

Late last month, Butn released its March quarter results. Butn pocketed $3.1 million from customer receipts but staff costs and interest repayments saw the fintech end the quarter with negative operating cashflow of $0.4 million.

The top line results were more positive.

Butn said its March quarter originations were up 77% to $109 million, leading to record quarterly revenue of $3.1 million, up 151%.

Butn ended the quarter with $12.4 million in cash and cash equivalents.

4DMedical in trading halt pending capital raise and ‘material commercial arrangement’

Respiratory imaging technology developer 4DMedical (ASX:4DX) is in a trading halt pending a capital raise and announcement of a ‘new, material commercial arrangement’.

In April, 4DX reported having $36.8 million in cash and cash equivalents at the end of the March quarter.

On a March quarterly cash burn of around $8.5 million, the medtech company had about four quarters of funding available, precipitating the capital raise.

Say hello to the new growth engine of the world economy | Ryan Clarkson-Ledward

In the US, we’ve got the second-biggest bank collapse ever.

Europe is still grappling with soaring energy prices and undersupply.

And at home, the RBA has just delivered a shocking rate rise as costs continue to climb.

No matter where you look, dark clouds seem to be forming over the global economy. But as fears of recession grow, investors need to realise that markets aren’t doomed.

Sure, there may be some ongoing turbulence for a while to come, but it won’t last forever. Instead, if you’re really paying attention to all the happenings, you should be looking toward the opportunity.

After all, there is one glaring outlier amidst all this uncertainty…

One economy that is not only proving resilient, but also growing rapidly…

The new emerging economy

In days gone, this bastion of hope for growth has typically come from China.

During our last major credit crunch, back in 2008, the Middle Kingdom helped offset some of the pain for Australia. Their ongoing boom at the time continued to deliver massive returns for our mining sector, propping up our economy better than many of our peers.

But you shouldn’t expect that same kind of fortune this time around.

As Macquarie’s chief economist, Ric Deverell, bluntly put it this week:

‘China’s not going to save the world this time.’

So, if not China, then who?

India…

With its gargantuan population, massive economic overhauls, and rapid industrialisation, India is the new powerhouse of global growth. Even now, amidst the uncertainty, their GDP is forecast to grow by 6.9% this year.

Already sitting in the fifth spot for total GDP, by 2027, India is expected to leapfrog both Germany and Japan for the third position. And from there it will likely continue to grow as it fights to overtake China and the US as well!

That’s why, right now, there’s perhaps no better place to invest than India.

And just like our trade relationship with China, Aussie miners are one of the best ways to profit from India’s rise.

https://www.moneymorning.com.au/20230504/the-new-growth-engine-of-the-world-economy.html

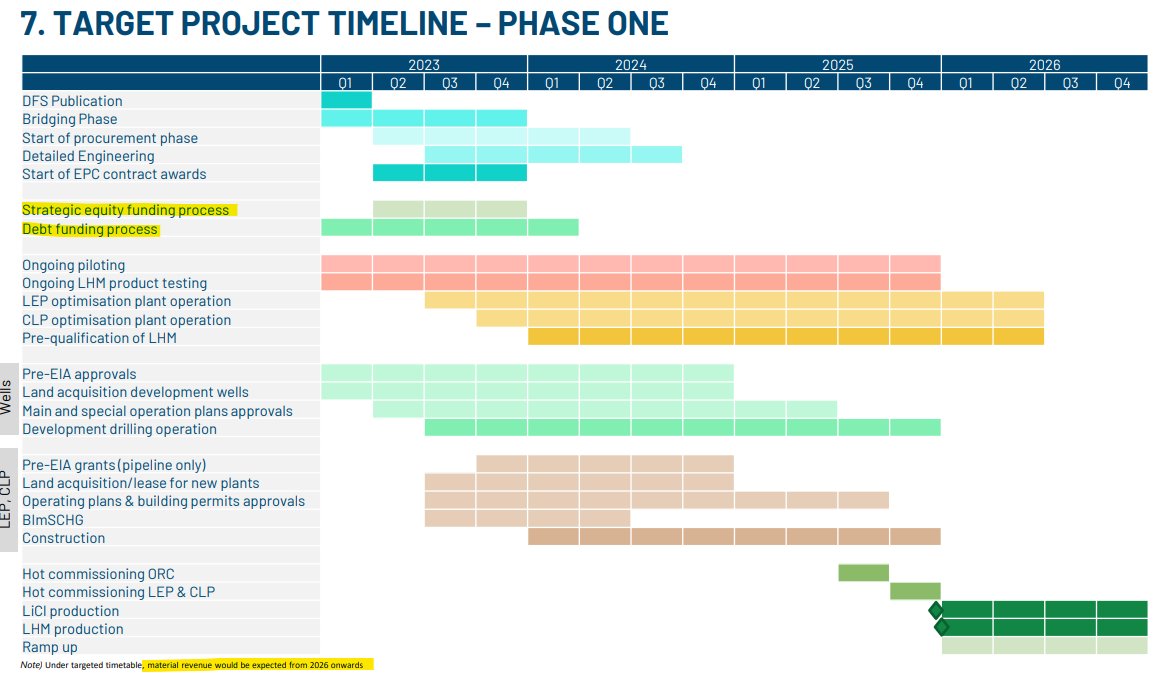

Vulcan Energy shareholders have a lot of reading to do

Vulcan Energy has dumped a lot of reading material on its shareholders.

A 74-page equity raising presentation along with the 574-page tome to go along with it. Maybe someone with a GPT-4 subscription can upload the mammoth document to the AI chatbot and ask it to skim for the salient bits.

Otherwise, it’ll be a few bleary-eyed days for the mortals sifting the wheat from the chaff.

Here are some interesting tidbits I’ve stumbled on so far.

On Vulcan’s pricing strategy:

‘The pricing under each of Vulcan Group’s existing lithium offtake agreements will be set monthly, quarterly, or on a six-month basis, and will be based on market prices for lithium, as calculated by reference to market recognised price reporting agencies’ contract-based indices. Therefore, movements in the market price of LHM are expected to have a substantial effect on Vulcan Group’s results from period to period. With a number of embedded costs (such as maintenance, power and consumables) being necessary for the operation of Vulcan Group’s facilities, any sustained increase or decrease in the market price of lithium would likely have a direct impact on Vulcan Group’s profits (positively or negatively, respectively). However, as Vulcan Group intends to sell substantially all of its LHM pursuant to lithium offtake agreements and the pricing under such lithium offtake agreements will be based on a mix of fixed price and indexation based on market prices calculated by reference to certain market indices, Vulcan Group does not expect to be exposed to the day-today spot market and believes that its pricing will be generally less volatile than the spot market. Additionally, Vulcan Group has included price floors and ceilings but also fixed prices in relation to part of the secured volume with offtakers, with the aim of bringing more stability to revenues.’

On the huge spike in lithium hydroxide pricing:

‘Lithium prices have generally experienced a strong upward trend in recent years, beginning with the 2015-2018 period when there was a sharp tightening in the availability of lithium in all product forms relative to demand levels, and generally continuing from 2019 to 2022 on the basis of strong demand figures for electric vehicles, expectations on future supply tightness and perceived future supply shortages (source: Fastmarkets Analysis, see section “8. INDUSTRY OVERVIEW”). Nevertheless, lithium prices have softened during the first quarter of 2023, with the average monthly market price for LHM peaking at $81,000 per tonne in January 2023, declining to $67,000 per tonne during the last week of March 2023 and reaching $45,000 per tonne by the last week of April 2023 based on the Asia contract price CIF, using contract price data from Fastmarkets’ online indices platform. This softening has been driven to a large extent by price declines in China as a result of lower electric vehicle demand during the period and existing lithium inventories, and has contributed to a downward pressure on lithium prices globally at the start of 2023 (source: S&P Global Daily).’

On the dual revenue stream strategy:

‘While the applicable feed-in tariff may not offer a risk-adequate return to investors in a stand-alone geothermal power plant, Vulcan Group’s business model, with its lithium and renewable energy businesses, foresees dual revenue sources of which the lithium business is expected to generate the larger revenue share. Following the acquisition of the Insheim Plant in December 2021, Vulcan Group began earning revenues from the sale of electricity from this plant in the financial year ended 30 June 2022, with revenues in the six months to 30 June 2022 amounting to EUR 2,977,000 and revenues in the six-month short financial year ended 31 December 2022 amounting to EUR 3,128,000. The revenues earned from this business in the financial year ended 31 December 2021 (i.e. prior to the acquisition by Vulcan Group) were EUR 5,756,000.’

On the costs of its direct lithium extraction method:

‘Lithium extraction operations based on the DLS method (such as the Zero Carbon Lithium™ Project) have higher capital costs at the outset as compared with more traditional methods of lithium extraction such as hard rock mining, while generally having lower ongoing operating costs than hard rock mining. According to Vulcan Group’s DFS for Phase One, the total capital expenditure (not including financing costs) required for Phase One of the Zero Carbon Lithium™ Project is expected to be approximately EUR 1,496 million (including contingencies). On the basis that the implementation of Phase Two is targeted to achieve similar production levels as, and in addition to those of, Phase One, the Company currently anticipates a materially similar additional amount to be required for Phase Two, subject to the completion of a definitive feasibility study for Phase Two (expected during the course of 2023). However, the exact level of capital expenditure required for the Zero Carbon Lithium™ Project will be further refined as the Company advances the project, with the level of capital expenditure for Phase Two to be further refined in the definitive feasibility study for Phase Two. See section “6.8.2 Capital expenditure” below for a further discussion of Vulcan Group’s estimated capital expenditure in connection with the Zero Carbon Lithium™ Project.’

$VUL dumped a lot of reading material on its shareholders.

A 74-page equity raising presentation along with the 574-page tome to go along with it.

Some selections below. $VUL.AX #Vulcan #ASX pic.twitter.com/U8nZNJdp6g

— Fat Tail Daily (@FatTailDaily) May 4, 2023

Vulcan Energy to raise $109 million at $5.10 a share

Two weeks ago, I covered here that lithium developer Vulcan Energy’s (ASX:VUL) planned total capex for the first phase of its Zero Carbon Lithium Project development is around $2.44 billion.

Vulcan planned to raise this amount on a debt to equity ratio of 65:35.

Meaning that Vulcan wants to raise an additional $850 million via equity raises — about the value of its current market cap.

Today, VUL launched a fully underwritten placement to raise part of that huge total — about $109 million.

The $109 million will fund ‘long lead item’ purchases and ‘general working capital and corporate purposes’.

What are the placement details?

Vulcan will issue 21.4 million shares at $5.10 a share. That’s a 17% discount to its last closing price.

$VUL is issuing 21.4m shares at $5.10 a share to raise ~$109 million, a 17% discount to $VUL.AX's last closing price. #ASX #lithium pic.twitter.com/SxW90haDCx

— Fat Tail Daily (@FatTailDaily) May 4, 2023

Vulcan is planning further debt and equity raises this year to shore up funds for development. VUL expects ‘material revenue’ from 2026.

Reading the Fed versus reading the economy

Will we see a change in how the market prices in interest rates?

Lately, the market has been prioritizing the Fed’s statements and policy attitude to inflation. Hanging on every word, traders wanted to discern the Fed’s forward guidance.

But the Fed is now moving away from firm policy stances. Clouded by uncertainty, the central bank is leaving things to data as it rolls in:

‘Looking ahead, we will take a data-dependent approach in determining the extent to which additional policy firming may be appropriate.

‘In determining the extent to which additional policy firming may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.

‘We will make that determination meeting by meeting, based on the totality of incoming data and their implications for the outlook for economic activity and inflation. And we are prepared to do more if greater monetary policy restraint is warranted.’

Forward guidance is over! The Fed will now truly be responding to data going forward, not slowly (or quickly) making its way to a set end point.

That's good and appropriate.

I expect that data to drive them to a few more rate hikes but we'll see. No need for them to say now.

— Jason Furman (@jasonfurman) May 3, 2023

US Fed: ‘inflation will not come down quickly’

The Fed’s 25 basis point hike was largely expected.

Less so was the Fed’s warning that inflation is unlikely to come down as quickly as the market would like. Meaning the Fed is not seeing rate cuts any time soon, or at least not as soon as the market is pricing in.

AFR’s James Thomson summed this up today in the Chanticleer column:

‘But the fresh warning Powell gave in his press conference that he does not expect to be cutting rates any time soon due to sticky inflation should raise an important question for investors: are the cuts investors are banking on really coming as soon as investors expect?

‘How the next few months play out will be telling. Bulls may find themselves barracking for the bad news that delivers rate cuts, while bears may want to see the US muddle through.’

Rewatch Powell’s press conference and indulge in semantics

US Federal Reserve chair Jerome Powell has a tough job directing monetary policy for the world’s most important economy.

But investors also have it tough analysing Powell’s comments to unearth his true meaning.

I’ve joked before traders are not only financial professionals but literary scholars, too. Semantics matter as much as financial statements.

Take Powell’s comments overnight at the press conference:

‘You will have noticed in the statement from March, we had a sentence that said the Committee anticipates that some additional policy firming may be appropriate. That sentence is not in the statement anymore. We took that out.

‘Instead, we’re saying that in determining the extent to which additional policy firming may be appropriate to return inflation to 2% over time, the Committee will take into account certain factors. So, that’s a meaningful change.’

What does that mean?

Is the change meaningful because the Fed no longer anticipates further hikes ahead? Have we reached the peak?

Watch Chair Powell’s statement from the #FOMC press conference:

Intro clip: https://t.co/ozSnfSBhVv

Full video: https://t.co/2AFxDFSLoo

Press Conference materials: https://t.co/CxqhrF5WAu— Federal Reserve (@federalreserve) May 3, 2023

US Fed raises interest rates by 25 basis points

In a unanimous decision, the US Federal Reserve raised rates for the tenth consecutive time.

The benchmark federal funds rate is now in the range between 5% and 5.25%, a 16-yeah high.

At a press conference following the decision, Fed chair Jerome Powell said central bank members ‘did talk about pausing, but not so much at this meeting’.

That said, Powell thinks the Fed is ‘getting closer [to a pause] or maybe even there’.

The latest hike brings the cumulative increase to 5% since March 2022 — the swiftest increase since the 1980s.

The FOMC statement used language broadly similar to how officials concluded their interest-rate increases in 2006, with no explicit promise of a pause by retaining a bias to tighten. https://t.co/gBcZ166OQv https://t.co/nDuyBH4YEQ

— Nick Timiraos (@NickTimiraos) May 3, 2023

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988