Live ASX News | ASX Down; US Regional Banks Stumble; JB Hi-Fi, Amcor, oOh!Media Feature

OpenLearning ends 25% higher on AI pivot

We’re at that point in the hype AI cycle.

The point where businesses pivot to AI or integrate AI to boost services.

Today, microcap SaaS edutech company OpenLearning (ASX:OLL) finished 25% higher on Wednesday after launching ‘AI-powdered learning design tools for education providers’.

The announcement was brought on by an article in The Australian titled ‘AI will revolutionise education in an unexpected way’.

OLL said its ‘generative AI-powered course authoring tools’ could change how education providers create content.

OpenLearning’s announcement went on:

‘Developed on Microsoft Azure’s OpenAI Service, these cutting-edge tools harness the power of GPT4 APIs, streamlining course design, and helping reduce the time and effort required to develop high quality short courses, micro-credentials and online degrees.

‘By leveraging OpenLearning’s unique approach to active learning and social constructivism, these AI-driven tools will generate course content and learning activities in line with OpenLearning’s educational philosophy. The embedded generative AI provides tailored suggestions to educators during the course design process, helping them create more engaging and effective learning experiences.’

OpenLearning will lock students away from its offering to ‘uphold the integrity of education’. Only educators will have access to these newfangled tools.

A pilot program using OLL’s new AI tools will include Western Sydney University, Education Centre of Australia, Sunway University Malaysia and the University of Wollonggong KDU Malaysia.

Western Sydney Uni’s executive director of education innovation, Cherie Diaz had this to say:

“This collaboration with OpenLearning demonstrates our dedication to embracing innovative technologies that can enable the future of education. We look forward to exploring how these AIpowered tools can assist us to deliver more personalised and effective learning experiences for our learners.”

Will students think AI-generated course content is more personalised and effective?

Why even enroll at a university in the first place? Why not cut out the middleman and buy a GPT-4 subscription and design your own course? Would not that be the height of personalisation?

Humm’s commercial business ‘produced another record quarter’

Humm Group (ASX:HUM) is leaving BNPL behind to focus on its core ‘bigger ticket financing’.

In a March quarter trading update, Humm reported that its commercial business posted ‘another record quarter’ with volumes up 39% on the prior corresponding period.

HUM chief executive Rebecca James said:

“Our strategy of focusing on bigger ticket items in the Consumer business is continuing to gain traction with volumes in Big Things AU growing 31% on pcp. Receivables for Consumer Finance were up 3% on pcp, while net loss / ANR was down 37bps driven by improved performance. Repricing initiatives implemented in the first half are beginning to deliver results with cost of funds increases being partially passed on in the Consumer business.”

James then mentioned the ‘unprecedented’ interest rate rises which compressed margins:

“Margin compression from the unprecedented increases in funding costs during late FY22 and FY23 continues to work its way through the backbook and will be offset by higher gross income which grows in line with the volume increases across the Commercial and Consumer businesses.

“The combination of higher gross income and the benefits of cost saving initiatives are expected to mitigate the seasonal impact of credit losses and margin compression, resulting in a second half normalised cash profit higher than the first half.”

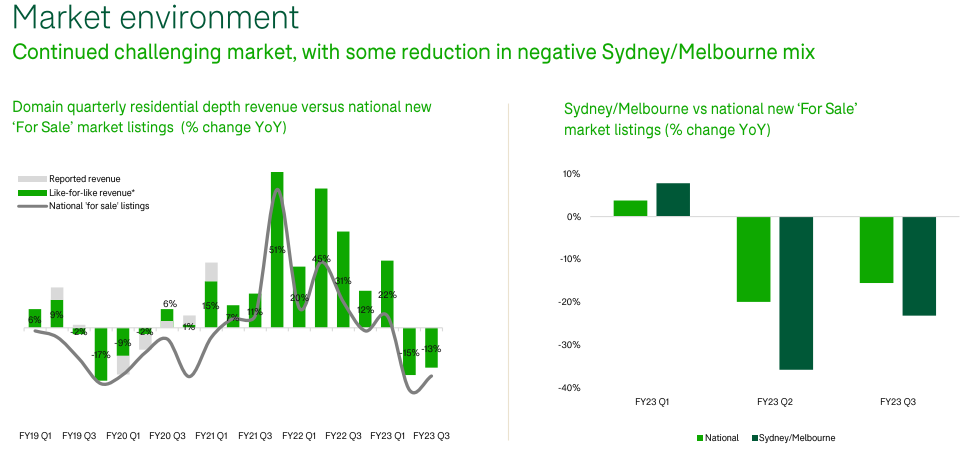

Domain downgrades EBITDA guidance

Online property marketplace Domain (ASX:DHG) said total revenue in the FY23 March quarter was down 4% year on year, with digital revenue down 1%.

Domain now expects FY23 EBITDA to ‘reduce in the mid-single digit percentage point range from FY22’s ongoing EBITDA margin’ due to ‘challenging’ market conditions.

The guidance downgrade reflects the ‘impact on FY23 H2 listing volumes from recent consumer confidence shocks’.

All energy paths lead to mining: Selva Freigedo

The Atacama Desert is one of the driest places on Earth. It’s a remote area, where nothing grows.

In fact, I hear it kind of looks like Mars. Conditions are so similar that NASA is using it as a practice area to test its Mars Rovers.

But the desert is also home to one of the most important lithium production areas in the world, the Salar de Atacama.

This salar (which means salt flat in Spanish) is the largest in Chile. Here, companies use the burning Sun to evaporate brine from the ponds. The substance left behind is lithium.

Atacama, which holds the world’s largest lithium reserves, has made Chile the second-largest lithium-producing country in the world, after Australia. Together, the two countries produced 77% of the world’s lithium in 2021.

But recent news coming out of Chile has sent shockwaves through the mining industry.

Chile sees lithium as a huge growth opportunity it doesn’t want to miss out on. So they recently launched its National Lithium Strategy.

While there isn’t a huge amount of detail out there yet, the plan is to create a State-owned lithium company that will be involved in Chile’s entire lithium production cycle. From exploration to value-adding to the lithium supply chain.

The idea is to turn Chile into the largest lithium producer in the world — Chile lost first place to Australia in 2017.

Stock prices for lithium companies Sociedad Quimica y Minera [NYSE:SQM] and Albemarle [NYSE:ALB] fell on the news and are trading 17% and 20% down, respectively, from last month.

You see, they both operate in the area and while their contracts don’t end until 2030 and 2043, the Chilean Government has said it’s hoping the companies will be open to accepting some sort of government participation before the contracts expire.

The whole thing has brought in a lot of uncertainty on the future of lithium production in Chile…which could mean more investment flowing into the lithium sector in Australia.

But it shows there’s still plenty of competition to secure critical materials.

https://commodities.fattail.com.au/all-energy-paths-lead-to-mining/2023/05/03/

The Big Four banks — good buying today: Callum Newman

‘Everyone has a plan until they get punched in the face.’

Boxer Mike Tyson said that one time.

Yesterday, the market copped one across the chops from the RBA. It’s getting another dose today.

But the fight between the bulls and the bears ain’t over…

And there’s always opportunity amongst volatility like this.

Read on for my take on where we should be looking!

Here’s what I noticed about yesterday. The 1% drop in the index got the headlines.

But there was one group of stocks that didn’t get rattled that much.

It was the Big Four banks.

I find that instructive. They’re under some pressure today. But I see opportunity.

What’s going on here?

All four are already well down from their February highs of 2023.

The US banking wobbles since March have hit financial stocks all over the place.

That’s not all…

Reuters reported back in December that Aussie fund managers had a very low weighting toward banks.

The concerns were peaking margins and rising bad debts as the Aussie property slowdown hit their assets.

The RBA rate rise yesterday gives a lift to bank profitability, via their loans (assets) with variable rates.

Plus, the housing market is now surprising people by rising from low stock available and high rents.

And look at this recent report on the Big Four’s results that are coming shortly, from The Sydney Morning Herald:

‘According to analyst estimates, the profits of NAB, ANZ and Westpac are all expected to increase by well above 10 per cent, mainly because of a sharp widening in net interest margins (NIMs), which compare funding costs with banks’ pricing of loans.’

There looks to be reasonable value in the Big Four. I suspect the market accumulates them on sell-offs like now.

There’s a potential scenario where this could turn into an excellent idea…

https://www.moneymorning.com.au/20230503/the-big-four-banks-good-buying-today.html

The Big Four banks — good buying today: Callum Newman

‘Everyone has a plan until they get punched in the face.’

Boxer Mike Tyson said that one time.

Yesterday, the market copped one across the chops from the RBA. It’s getting another dose today.

But the fight between the bulls and the bears ain’t over…

And there’s always opportunity amongst volatility like this.

Read on for my take on where we should be looking!

Here’s what I noticed about yesterday. The 1% drop in the index got the headlines.

But there was one group of stocks that didn’t get rattled that much.

It was the Big Four banks.

I find that instructive. They’re under some pressure today. But I see opportunity.

What’s going on here?

All four are already well down from their February highs of 2023.

The US banking wobbles since March have hit financial stocks all over the place.

That’s not all…

Reuters reported back in December that Aussie fund managers had a very low weighting toward banks.

The concerns were peaking margins and rising bad debts as the Aussie property slowdown hit their assets.

The RBA rate rise yesterday gives a lift to bank profitability, via their loans (assets) with variable rates.

Plus, the housing market is now surprising people by rising from low stock available and high rents.

And look at this recent report on the Big Four’s results that are coming shortly, from The Sydney Morning Herald:

‘According to analyst estimates, the profits of NAB, ANZ and Westpac are all expected to increase by well above 10 per cent, mainly because of a sharp widening in net interest margins (NIMs), which compare funding costs with banks’ pricing of loans.’

There looks to be reasonable value in the Big Four. I suspect the market accumulates them on sell-offs like now.

There’s a potential scenario where this could turn into an excellent idea…

https://www.moneymorning.com.au/20230503/the-big-four-banks-good-buying-today.html

ABS: employees’ annual living costs highest on record

Living costs for employee households recorded the largest annual rise of all household types, coming in at 9.6% in the March quarter, according to the Australian Bureau of Statistics.

This was the largest increase since ABS began collating such data in 1999.

Mortgage payments were the biggest reason.

Mortgage interest charges rose nearly 80% over the year! That was up from 61.3% annual rise in the December 2022 quarter.

Source: ABS

ABS: employees’ annual living costs highest on record

Living costs for employee households recorded the largest annual rise of all household types, coming in at 9.6% in the March quarter, according to the Australian Bureau of Statistics.

This was the largest increase since ABS began collating such data in 1999.

Mortgage payments were the biggest reason.

Mortgage interest charges rose nearly 80% over the year! That was up from 61.3% annual rise in the December 2022 quarter.

Source: ABS

Australian retail sales rose 0.4% in March

The Australian Bureau of Statistics revealed that Australia’s retail turnover rose 0.4% in March, up from a 0.2% rise in February, a third straight monthly rise.

But the Bureau’s Ben Dorber said spending on discretionary goods saw a ‘pull-back’, with discretionary turnover at a similar level to six months ago.

Dorber further said:

“Food retailing has now recorded 13 consecutive monthly rises, largely driven by high food inflation.

“Businesses in cafes, restaurants and takeaway food services are passing on their rising costs to consumers through price rises, while also benefitting from strong demand driven by the continued return of large-scale cultural and sporting events.”

“Spending on non-food retailing has slowed in response to interest rate rises and increased cost of living pressures. This follows increased spending during and immediately following much of the COVID-19 pandemic period.”

Clothing, footwear, and personal accessory retailing fell 1% in March, the category with the biggest fall.

Household goods posted the second-largest decline, down 0.4%.

Australian retail sales rose 0.4% in March

The Australian Bureau of Statistics revealed that Australia’s retail turnover rose 0.4% in March, up from a 0.2% rise in February, a third straight monthly rise.

But the Bureau’s Ben Dorber said spending on discretionary goods saw a ‘pull-back’, with discretionary turnover at a similar level to six months ago.

Dorber further said:

“Food retailing has now recorded 13 consecutive monthly rises, largely driven by high food inflation.

“Businesses in cafes, restaurants and takeaway food services are passing on their rising costs to consumers through price rises, while also benefitting from strong demand driven by the continued return of large-scale cultural and sporting events.”

“Spending on non-food retailing has slowed in response to interest rate rises and increased cost of living pressures. This follows increased spending during and immediately following much of the COVID-19 pandemic period.”

Clothing, footwear, and personal accessory retailing fell 1% in March, the category with the biggest fall.

Household goods posted the second-largest decline, down 0.4%.

Philip Lowe explains RBA’s hike decision

Late last evening, Reserve Bank governor Philip Lowe was in Perth addressing a crowd at a ‘community dinner’.

The dinner followed the RBA’s unexpected decision to raise interest rates by 25 basis points to 3.85%.

If some at the dinner struggled to digest the decision, Lowe was on hand to explain it.

The RBA chief said last month’s pause was not a pivot but a reconnaissance mission to ‘provide us with more time to assess the pulse of the economy and the outlook’.

Clearly, the pulse was too rapid for the RBA’s liking.

‘Since then, we have seen further evidence that the Australian labour market is still very tight, that services price inflation is proving to be uncomfortably persistent abroad, and that asset prices – including the exchange rate and housing prices – are responding to changes in the interest rate outlook.

‘We also received confirmation that the peak in inflation in Australia is now behind us, but that has not changed our view that it will be some time yet before inflation is back in the target range. Goods price inflation is slowing, which is good news. But services and energy price inflation is still high and likely to remain so for some time. Looking overseas, we see worryingly persistent services price inflation. It is possible that circumstances might be different here in Australia, but the experience abroad points to an upside risk, especially given the high degree of commonality across countries in inflation dynamics recently.

‘Given this flow of data and our assessment of the outlook, the Board judged that it was appropriate to increase interest rates again today.’

Philip Lowe explains RBA’s hike decision

Late last evening, Reserve Bank governor Philip Lowe was in Perth addressing a crowd at a ‘community dinner’.

The dinner followed the RBA’s unexpected decision to raise interest rates by 25 basis points to 3.85%.

If some at the dinner struggled to digest the decision, Lowe was on hand to explain it.

The RBA chief said last month’s pause was not a pivot but a reconnaissance mission to ‘provide us with more time to assess the pulse of the economy and the outlook’.

Clearly, the pulse was too rapid for the RBA’s liking.

‘Since then, we have seen further evidence that the Australian labour market is still very tight, that services price inflation is proving to be uncomfortably persistent abroad, and that asset prices – including the exchange rate and housing prices – are responding to changes in the interest rate outlook.

‘We also received confirmation that the peak in inflation in Australia is now behind us, but that has not changed our view that it will be some time yet before inflation is back in the target range. Goods price inflation is slowing, which is good news. But services and energy price inflation is still high and likely to remain so for some time. Looking overseas, we see worryingly persistent services price inflation. It is possible that circumstances might be different here in Australia, but the experience abroad points to an upside risk, especially given the high degree of commonality across countries in inflation dynamics recently.

‘Given this flow of data and our assessment of the outlook, the Board judged that it was appropriate to increase interest rates again today.’

Jim Rickards: will AI take over the world?

AI is an old story.

Aristotle speculated on what the world would be like if a spindle could weave cloth without human hands. Alan Turing (father of theoretical computer science and the man who cracked the Nazi Enigma code) wrote essays on the ethical dilemmas of AI in the 1950s. My first discussions about AI occurred with a consultant from Arthur D Little in 1979. The concept has been around for decades.

What changed was the massive increase in available texts (starting with the internet, world wide web, and search engines in the 1990s), and the exponential increase in processing power (with NVIDIA and other processors in the 2010s). The missing pieces were large language models (LLMs) and natural language processing (NLP).

When these elements were combined with GPT algorithms (that allow the computer to be ‘trained’ on certain texts), the result was apps that could read billions of pages of text (LLM) in a common-sense kind of way (NLP) and produce answers in plain English.

Are these machines poised to take over the world?

Not really.

To downplay them a bit, they’re just speed-reading machines that can spit back results with some nuance. They also make things up.

That’s what I call the ‘puppy factor’, where the machine wants a pat on the head for answering your question the way a puppy wants a pat on the head for fetching a ball.

The problem is the machine will invent facts in order to please its master. One writer asked ChatGPT to write a biography of himself. The machine promptly did so, including his date of death and an obituary.

A real and immediate problem does exist, as described in this article. ChatGPT is offered by a consortium controlled by Microsoft. It is a threat to Google because GPT tech means the death of search engines. Google has responded with its own GPT app called Bard.

Google engineers have warned management that Bard is a ‘pathological liar’ and offers solutions to technical problems that can cause injury and death. We’ll leave it to readers to decide if and when they want to use GPT technology.

Just take it with more than a grain of salt.

Jim Rickards: will AI take over the world?

AI is an old story.

Aristotle speculated on what the world would be like if a spindle could weave cloth without human hands. Alan Turing (father of theoretical computer science and the man who cracked the Nazi Enigma code) wrote essays on the ethical dilemmas of AI in the 1950s. My first discussions about AI occurred with a consultant from Arthur D Little in 1979. The concept has been around for decades.

What changed was the massive increase in available texts (starting with the internet, world wide web, and search engines in the 1990s), and the exponential increase in processing power (with NVIDIA and other processors in the 2010s). The missing pieces were large language models (LLMs) and natural language processing (NLP).

When these elements were combined with GPT algorithms (that allow the computer to be ‘trained’ on certain texts), the result was apps that could read billions of pages of text (LLM) in a common-sense kind of way (NLP) and produce answers in plain English.

Are these machines poised to take over the world?

Not really.

To downplay them a bit, they’re just speed-reading machines that can spit back results with some nuance. They also make things up.

That’s what I call the ‘puppy factor’, where the machine wants a pat on the head for answering your question the way a puppy wants a pat on the head for fetching a ball.

The problem is the machine will invent facts in order to please its master. One writer asked ChatGPT to write a biography of himself. The machine promptly did so, including his date of death and an obituary.

A real and immediate problem does exist, as described in this article. ChatGPT is offered by a consortium controlled by Microsoft. It is a threat to Google because GPT tech means the death of search engines. Google has responded with its own GPT app called Bard.

Google engineers have warned management that Bard is a ‘pathological liar’ and offers solutions to technical problems that can cause injury and death. We’ll leave it to readers to decide if and when they want to use GPT technology.

Just take it with more than a grain of salt.

oOh!media sinks 20% on ‘softening media market’

Media company oOh!media (ASX:OML) is down over 20% at the open on Wednesday after releasing a trading update tacked on to its Macquarie Australia Conference presentation.

OML is seeing a ‘softening media market’, with trading moderating ‘significantly’ in March. As for April, April media revenue was ‘particularly soft’, pacing around 10% lower on the prior corresponding period.

oOh!media reported a decline in short-term in-month bookings versus the prior corresponding period, too, especially in government spend.

$OML is down over 20% after revealing a 'softening media market' in a trading update. #ASX $OML.AX pic.twitter.com/H830XM5e9i

— Fat Tail Daily (@FatTailDaily) May 3, 2023

AI investing — beware the lessons from history

If AI were a band, then ChatGPT would be its first number-one single. ChatGPT brought AI to the masses.

And now AI is getting the mass culture treatment.

Endless coverage, countless predictions, hot takes, fearmongering, and hype.

AI is rapidly improving, and its tools will disrupt lives.

It’s already doing that.

Last month at the ASU+GSV Summit, Turnitin CEO Chris Caren said his company will need only 20% of its engineers and many of those will be hired out of high school, not college.

Caren predicted a similar shrinkage for the sales and marketing department.

AI is ushering a time of both displacement and opportunity.

Some jobs and industries will change (or disappear), while whole new ones will spring up.

Maybe in a few months, we’ll be hearing about a high school student who turned their GPT-4 subscription into a hot new start-up.

Oh, how the press will have a field day with that story.

The hype is predictably spilling into the investing sector.

A good barometer of a trend’s potency is interest from venture capital. And VCs are loving AI. One founder told Reutersthat VCs ‘think this is the new internet’.

According to PitchBook, investment in AI start-ups rose to US$5.9 billion since 2022, up from US$1.5 billion in 2020.

AI will transform much of our lives. But will it make for a good investment?

https://www.moneymorning.com.au/20230502/ai-investing-the-upsides-and-the-pitfalls.html

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988