ASX Today — Live ASX News | XJO Falls, Earnings Season Kicks Off In Earnest

Battery metal stocks the worst performers on Thursday

The future may be green. And the future may be fueled by battery materials like lithium, copper, and graphite.

But battery metal stocks aren’t faring so well right now.

The top three worst performers on the ASX on Thursday were graphite producer Syrah Resources (down 9.5%), lithium developer Core Lithium (down 5.5%), and fellow lithium hopeful Sayona Mining (down 5%).

Another lithium developer — Lake Resources — hit a new 52-week low today, too. LKE closed at 42 cents a share, down 78% over the past 12 months.

A green future will need plenty of #lithium, #copper, and #graphite.

But battery metal stocks aren’t faring so well.

The 3 worst performers on the #ASX on Thursday were $SYR (-9.5%), $CXO (-5.5%), and $SYA (-5%).$LKE hit a new 52-week low today, too.

— Fat Tail Daily (@FatTailDaily) April 27, 2023

‘Beauty and the bust’ — Jason Andrew takes on BWX

SBO Financial’s Jason Andrew writes some of the best financial breakdowns in Australia.

Yesterday, he broke down the collapse of Aussie skincare retailer BWX, which entered administration earlier this month.

“While softening demand, excess inventory and an over-leveraged balance sheet were contributing factors, it was the hangover of its toppy acquisitions that put the final nail in the coffin”, wrote Andrew.

BWX grew through acquisitions.

Source: Jason Andrew

Yet this acquisitiveness was its undoing.

Revenue grew, but not enough to offset the asking price of its purchases. These acquired assets soured as interest rates rose — and the cost of capital with them.

As Andrew explained:

“BWX bought their business in an era of cheap capital (low interest rates) and solid consumer demand due to government stimulus and money printing. At that time, the cost of borrowing money was lower and the growth rate was higher, so it made sense to pay more for the assets.

“Being a premium skincare provider, BWX is particularly exposed to changes in consumer discretionary spending, which has not only impacted the company’s operating performance, but also impacts the write-down of the assets it bought.”

All this led to a massive writedown of $322 million in FY22.

Not even the best ointment can soothe that pain.

Syrah to moderate production as graphite demand softens

Syrah Resources (ASX:SYR) will cut production from its Balama operation in Mozambique following ‘prevailing volatile China anode market conditions and the availability of significant finished product inventory’.

Syrah will curb production until demand conditions and prices ‘warrant higher capacity utilisation’.

This is somewhat at odds with Syrah’s long-standing claim that Balama’s cash costs are ‘expected to reduce as the production rate increases beyond 20kt per month, with increasing sales and no inventory constraints’.

SYR did not quantify the announced production moderation but retained the Balama CT cash cost guidance at US$430-480 per tonne. This guidance is fettered with qualifications:

“Balama C1 cash cost (FOB Nacala/Pemba) guidance remains US$430–480 per tonne at a 20kt per month production rate, with the lower end of the range assuming a normalisation of diesel price to historical levels, the Solar Battery System operating at full capacity and updated labour costs associated with the renewal of the Company Level Agreement (“CLA”). Balama’s cash costs are expected to reduce as the production rate increases beyond 20kt per month, with increasing sales and no inventory constraints, and as improvement initiatives continue to be embedded.”

$SYR will cut production at Balama following 'volatile China anode market conditions and the availability of significant finished product inventory'.$SYR.AX will curb production until demand conditions and prices 'warrant higher capacity utilisation'.#ASX #graphite pic.twitter.com/zc7B6xy0s5

— Fat Tail Daily (@FatTailDaily) April 27, 2023

Airtasker lays off 20% of workforce

Airtasker (ASX:ART) is changing tack. Cost reduction is now the top priority.

As a result, Airtasker will cut 20% of staff and ‘restructure to focus on efficient global scaling of its core business’.

The goal is to be cashflow positive in FY24.

Airtasker founder Tim Fung said:

“Whilst Airtasker has delivered strong YTD March 2023 revenue growth of 49% we believe that in the current macroeconomic environment it is the right time to focus on greater efficiency and return to positive operating cashflow.”

Somewhat confusingly, Airtasker’s latest quarterly showed March quarter revenue rising 34.1% on the prior comparative period to $11.5 million. This was only up 5.3% if you exclude the contribution from the Oneflare acquisition.

Ex-Oneflare, Airtasker’s gross marketplace volume fell 2.6% year on year. Even with the Oneflare contribution, GMV fell quarter on quarter.

Airtasker ended the quarter with $20.6 million in cash and cash equivalents.

Syrah’s production struggles continue in March quarter

Mozambique-based graphite producer Syrah Resources (ASX:SYR) continues to struggle eking out a profit from its Balama operation.

During the March quarter, Syrah’s free cash flow was in the red by US$26 million.

US$21.4 million borrowed during the quarter cushioned the blow to the bank balance but Syrah still saw its cash and cash equivalents shrink from US$90.4 million to US$84.2 million.

The story with Syrah remains the same — its not producing enough graphite at a high enough price to cover costs.

While SYR pocketed US$25.6 million from customer receipts in the quarter, production costs alone were US$25.7 million. On top of that, Syrah spent US$29 million on property, plant and equipment — most of that going towards the development of Vidalia in the US.

Syrah said graphite production at Balama underperformed in March. A bunch of culprits were ready at hand to draw blame:

“Net cash from operating activities for the quarter was impacted by operational stoppages and underperformance at Balama and relatively higher working capital at quarter end with significant natural graphite inventory positions accumulated.”

Syrah also seemed to insinuate a US Department of Energy grant worth about US$220 million it was selected for last year isn’t progressing as intended.

Syrah expected the DOE grant to close in the upcoming quarter ‘but is now being assessed in conjunction with alternative funding options’. In fact, the producer said it applied for a ‘further DOE loan, of a significantly higher amount than the DOE grant’.

Currently, Syrah has a binding loan facility with the DOE for up to US$102 million to finance Vidalia.

Syrah argued a grant is no doubt great, but ‘debt funding options are expected to provide higher cash proceeds compared with a DOE grant, which is likely to be taxed as income as received’.

Interesting.

$SYR $SYR.AX insinuated a US DoE grant worth ~US$220m it was selected for last year isn't progressing as intended.

Syrah expected the DoE grant to close in the upcoming quarter 'but is now being assessed in conjunction with alternative funding options'. #ASX #graphite pic.twitter.com/VYW4gt9fv7

— Fat Tail Daily (@FatTailDaily) April 27, 2023

Playside posts record original IP revenue

Video game developer Playside Studios (ASX:PLY) posted record original IP revenue and was operating cash flow positive in the March quarter.

Original IP revenue rose 95% to $5 million while total revenue rose 73% to $9.3 million, giving Playside net operating cash inflow of $1.7 million.

Playside owns the popular Dumb Ways to Die mobile game franchise, which had over 15 million downloads during the quarter and drove the majority of sales. Playside said downloads of the game came ahead of expectations, boosted by a ‘viral resurgence in brand activity, initially on TikTok but eventually spreading to other social media platforms’.

Will this viral resurgence last? The installs chart suggests a petering out:

Chief executive Gerry Sakkas said:

“The quarter finished strongly as the viral success of Dumb Ways to Die persisted through to the end of the period, contributing to record Original IP revenue and our best operating cash flow quarter to date. We are very pleased to provide revenue guidance that implies underlying growth of at least 70% for this financial year. This year has seen our Work for Hire pipeline grow much larger than we could’ve anticipated at the start of the year, including a new VR co-development partnership with Skydance this week. Our decision to commit to this volume of work reflects our desire to internally fund a portfolio of Original IP projects with even greater potential than the slate of titles we announced at the time of our IPO two years ago. At the half year result we began to outline our plans to work on new PC/Console titles that meet this criteria. We currently have a team working on a new indie title and look forward to sharing more details as the calendar year progresses.”

Even Coca-Cola and Pepsi are getting into AI: Ryan Clarkson-Ledward

It’s been an eye-opening week for earnings over in the US.

The general result, and consensus, seems to be surprising. A lot of big stocks are faring better than many expected.

Obviously, that doesn’t mean the threat of a downturn is behind us…

The choppy markets of late aren’t going to go away until we have more certainty on inflation and interest rates. As for when that may happen, your guess is as good as anyone’s. The only thing more volatile than markets nowadays are central bankers.

But despite all this, the big winner has clearly been big tech.

After all the layoffs, all the cost cutting, and all the speculation, big tech continues to thrive. You can see this in the huge earnings beats for Microsoft, Alphabet (Google), and Meta (Facebook).

All three of these tech titans are proving why they dominate US markets.

And when it comes to these three stocks, all of them pinpointed artificial intelligence (AI) as the main driver of their growth to come…

In both Microsoft’s and Google’s conference calls, it was clear that AI was the focus. As Reuters reports, AI was mentioned an astounding number of times by both companies:

‘Google used the term 52 times on its first-quarter call on Tuesday, up from 45 in the fourth quarter. Microsoft said it 36 times, versus 20 — not including references to its partner OpenAI.’

It was a similar story for Meta too. Here’s what Zuckerberg had to say on Meta’s AI development:

‘At this point, we are no longer behind in building out our AI infrastructure,

‘And to the contrary, we now have the capacity to do leading work in this space at scale.’

Let’s be real though, none of this is really that surprising. If we were to put our cynical hat on for a moment, we could argue that AI is just the latest buzzword fad for tech to latch on to.

After all, it was around this time last year that ‘Metaverse’ was doing something similar. Today, almost all interest in that technology has dried up, despite some exciting developments in the sector.

My point is the market has a short attention span. And big tech companies are notorious for trying to dazzle with short-lived excitement each and every year.

Personally, I’m taking the cynical hat off for good when it comes to AI.

I don’t believe it will be short-lived, and I think that is being made clear by the discussions beyond tech. For example, it wasn’t just the FAANG stocks discussing their AI capabilities and ambitions this week…

The biggest AI surprise this week came from both Coca-Cola and PepsiCo.

Yes, two of the biggest names in beverages and snacks spent a good amount of time discussing AI. Here is what Coke’s head of Global Creative Strategy had to say on the topic:

‘I was the one who launched our first NFT for Friendship Day in 2021 and it worked very well, and after that we launched multiple different digital collectibles,

‘But I think AI is a more approachable technology. I can collect NFTs if I’m a big fan, but then I don’t use it every day. [AI] is available to you — you use it you can turn that into your profession, your marketing efficiency machine, you can create and it’s happening now.

‘So I feel the utility value of this technology is much higher.

‘I’m telling everyone…please learn to prompt, it’s going to be useful and it’s fun.’

https://www.moneymorning.com.au/20230427/ai-is-all-over-us-earnings.html

Tigers Realm Coal sinks 20% on potential delisting update

Tigers Realm Coal (ASX:TIG) is discussing a potential privatisation of the company with several shareholders after its Russian subsidiaries came under scrutiny by Australian authorities.

The Department of Foreign Affairs and Trade’s indicative assessment is that TIG’s Russian operations are likely to be ‘prohibited by, or subject to authorisation under, regulation 4A of the Australian Sanctions Regulations which relates to sanctioned imports’.

Tigers Realm says the sanctions ‘represent an existential threat to the company’s ability to continue operating as a public company’.

So, while TIG disagrees with DFAT’s assessment, it’s ‘actively progressing its consideration and preparation for the potential privatisation’.

Going private, in TIG’s estimation, will make dodging sanctions easier:

“As a private company, the Company will be able to react more readily to both sanctions‐related risks as well as to an array of other issues directly or indirectly related to the dramatic deterioration in the geopolitical space in which the Company operates.”

If the privatisation goes ahead, it will involve a ‘selective capital reduction’ to allow some shareholders to ‘realise immediate value for their shares’ along with a delisting. Earlier this week, Tigers Realm lodged a request with the ASX to in-principle approve a proposed delisting.

This arrangement will require shareholder approval, which TIG will seek at two upcoming meetings.

TIG mentioned today that 92% of TIG shares are held by just four shareholders. This illiquidity formed part of the rationale for the proposed delisting, as it will ‘provide a unique liquidity event for shareholders’.

Helloworld upgrades guidance following ‘strong’ third quarter

Travel distribution firm Helloworld (ASX:HLO) has updated guidance following a ‘strong’ third quarter.

Helloworld swung to an underlying (unaudited) EBITDA profit of $14.2 million in 3Q23 following an EBITDA loss of $4.9 in 3Q22. On a year to date basis, underlying EBITDA was $29.8 million compared to a year to date loss of $12.3 million in FY22.

A big reason for the turnaround was a big jump in total transaction value.

In the March quarter, TTV rose 150% to $596.2 million on the relevant period last year.

Revenue for the quarter rose 240% to $46.9 million, with a revenue margin of 7.7%.

The travel stock said demand for international and domestic travel ‘continues to improve with a trend towards longer trips and longer lead times to overcome global supply constraints’. Interestingly, Helloworld noticed demand across ‘traditional Asian markets remains slow’.

These results have prompted a rethink.

Helloworld now expects FY23 underlying EBITDA to increase from $28m-$32 million to $38m-$42 million.

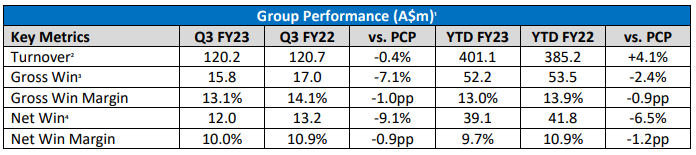

Bluebet says Australian business ‘back to generating positive operating cash flow’

Wagering firm Bluebet (ASX:BBT) said it grew its market share in Australia, with the local segment returning to positive operating cash flow.

Bluebet grew its customers 27% to 63,118. However, the actual bet count rose a more modest 7.9% to 2.6 million in the March quarter.

Customer receipts for the quarter totalled $30.7 million but total net cash outflows from operating activities came in at $2.3 million. Year to date (9 months), the net cash outflows totalled $11 million.

Bluebet ended the quarter with a reduced cash balance of $27.6 million.

BlueBet CEO Bill Richmond said:

“We continued to make good progress in Q3, with market share gains in Australia driven by strong growth in Sports. With our Net Win margin back above 10% and our Australian business back to generating positive operating cash flow, we have demonstrated our ability to deliver sustainable, profitable growth.”

Good morning!

Good morning!

Kiryll here, again.

It’s shaping up to be a big day on the ASX, with a swathe of companies releasing their March quarter results. I hope to cover as much of that as I can today.

(Here’s Bing AI’s generated image of a busy trader starting their morning. May your morning be less screen-saturated).

Source: Bing AI

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988