ASX Today — Live ASX News | XJO Rises on Huge Quarterly Earnings Day

Arizona Lithium has $4.4 million left in the bank

Lithium junior Arizona Lithium (ASX:AZL) has $4.4 million left in the bank.

Arizona’s cash balance dwindled after paying $44 million to acquire Prairie Lithium. While the acquisition enlarged AZL’s lithium resource to 4.4MT of lithium carbonate equivalent, it shrank its cash holdings.

The $120 million developer estimates it has about four quarters of funding available given its March quarter cash outgoings of $1.2 million.

But those outgoings are surely only set to grow as it ramps up development of its Big Sandy and Prairie projects. Especially when you consider that exploration expenditure ‘primarily relates to the setup and operating costs of the Lithium Research Centre’.

Is a capital raise in the offing? A debt facility?

Getting your hands on world-class deposits before the major miners snap them up: James Cooper

The following is an extract from an article by our commodities expert James Cooper in the newly launched publication dedicated to resource stocks.

Over the last 2–3 years, the large mining conglomerates have benefited from higher prices and juicy revenues…

While that’s proved a gift for shareholders in the form of handsome double-digit dividends, it does point toward some worrying trends in the years ahead.

You see, mines are a depleting asset.

As companies ramp up production on the back of rising commodity prices and revenue pours in…outsized dividends are one of the benefits.

But without new discovery or investment into new projects, future output DRIES up.

That spells trouble for majors attempting to maintain output at their ageing operations…many of which were discovered several decades ago.

But the apathetic actions of mining conglomerates present an enormous opportunity for the new developers holding the next generation of deposits.

It’s why being selective in this coming age of resource scarcity remains critical.

New developers will remain in the cross hairs for mining conglomerates looking to replace depleting reserves…

But acquisitions will come at a premium.

In fact, our Diggers and Drillers portfolio has been on the receiving end of a takeover bid from one major already…

In a repeat of the Oz Minerals deal, we now have a similar situation playing out for Mincor.

MCR holds a key nickel asset in the Kambalda region of Western Australia and is now subject to a $760 million takeover offer from Wyloo Metals.

Wyloo is a private company owned by Australia’s mining magnate, Andrew Forrest.

It already holds several key critical metal projects in Australia and overseas.

But Wyloo is keen to get its hands on Mincor’s assets for several key reasons…

Junior companies holding nickel assets are rare…the major conglomerates including BHP, Glencore, and Vale dominate the extraction of this commodity.

However, Mincor is a mid-cap miner tied exclusively to nickel production…

That means investors can gain maximum upside from higher nickel prices by holding this stock.

It’s ONE of the reasons I recommended Mincor to my subscribers earlier this year.

It’s also a key reason Wyloo is making a bid for this company.

However, there are some other interesting dynamics that made Mincor a strategic investment…

Right now, Russia is a major global supplier of the metal.

In fact, the country holds the world’s largest nickel mine located on the Kola Peninsula near the Norwegian and Finnish borders.

The operator, known as Nornickel Kola Division, extracts around 172,000 tonnes per annum.

That kind of output trumps the world’s second-largest mine, Nickel West, which generates around 75,000 tonnes for its owner BHP in Western Australia.

But Russia’s invasion of Ukraine last year has made the supply outlook increasingly vulnerable.

So far, US and European nations have NOT added Russian nickel to its list of embargoes…

To me, that’s a warning sign.

The West is concerned about FUTURE global supply.

While exempting Russian nickel from embargoes has helped stabilise the market, it doesn’t guarantee future stability…

That’s because the market SUPPLIER holds the power…Russia.

Nickel is a key weapon in Putin’s trade arsenal as he looks to recapture power in this trade struggle.

That’s where companies who are able to offer alternative supplies are set to benefit.

Scarcity, a breakdown in global trade, and enormous projected demand points toward a very bright future for stocks like Mincor.

https://commodities.fattail.com.au/get-your-hands-on-world-class-deposits-before-the-major-miners-snap-them-up/2023/04/28/

Who’s hitting their 52-week lows today?

Quite a few companies are hitting their 52-week lows today.

Here are the top five by market size:

- Syrah Resources (ASX:SYR)

- Brainchip (ASX:BRN)

- Vista Group (ASX:VGL)

- Trajan Group (ASX:TRJ)

- Bubs Australia (ASX:BUB)

Bubs China sales down 56%, strategic review of China operations initiated

BUB’s China gross revenue was down 56% year on year in the March quarter, with ‘significant amounts of finished goods inventory held in trade’.

Bubs is yet to see the an uplift in sales it was expecting following China’s recent COVID-19 policy change and border reopenings.

The company said the short-term outlook for sales in China ‘remains subdued’.

“China Q3 Gross Revenue was down 56% on pcp with significant amounts of finished goods inventory still held in trade, predominately Bubs Supreme. This is significantly impacting the replenishment volume and therefore new sales to China. The Bubs Supreme brand was initially custom made for principal corporate daigou partner, AZ Global. Bubs Sales of IMF and Adult Nutrition in the CBEC and O2O channels have been and remain below expectations and Bubs is working to improve the distribution and sell through in China.”

The Bubs board will now perform a review of its China operations and update shareholders once the review is complete. No timeline was given.

$BUB's March quarter revenue fell 10% after reporting 'poor' sales in China. $BUB.AX's operating cash burn was $12m, with the firm initiating a review into the global business.

Financial YTD, Bubs would be underwater were it not for the $60m raised from issuing shares. pic.twitter.com/pX8uKiDR6e

— Fat Tail Daily (@FatTailDaily) April 28, 2023

Bubs reports ‘poor’ sales in China, initiates strategic review of global business

In June 2022, Bubs was flying high.

China sales were picking up just as Bubs was selected to help America’s infant formula shortage.

That month, Bubs upgraded its FY22 guidance, with the Bubs founder Mrs Carr then saying:

“Due to a strong momentum in China and the unanticipated volume of sales in the USA, complemented by Bubs’ demonstrated agility and speed to respond to the call for action with first mover advantage, Fourth Quarter turnover is likely to be higher than originally anticipated. It has been an extraordinary journey for Bubs to have had over 12 months of in-market experience to provide the first response to USA’s infant formula shortage, which is likely to change the industry landscape in the USA. This has significantly accelerated our entry to one of the largest infant formula markets in the world, and we look forward to introducing more American families to Bubs’ full range of products.”

Since June 2022, however, BUB shares have fallen 70%.

Today, the infant formula company released its March quarter results, showing revenue was down 10%. Bubs reported ‘poor’ sales in China and other overseas markets.

“Expenditure management is an immediate focus of the board, and a strategic review of the global business has commenced,’ said BUB chair Katrina Rathie.

It’s no wonder ‘expenditure management’ is a pressing concern — BUB’s operating expenses rose 74% on the March 2022 quarter.

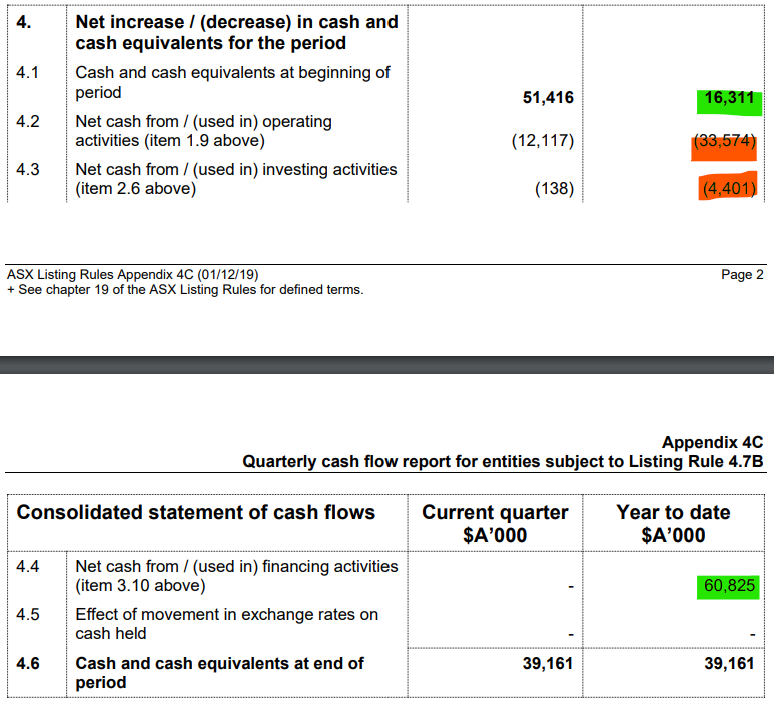

Bubs’s operating cash burn totalled $12 million for the three months ended March 31st.

The infant formula company continues to struggle with margins. Bubs booked $13.1 million from customer receipts in the quarter but paid $12.9 million for product manufacturing costs alone.

Bubs ended the quarter with $39.1 million in cash and cash equivalents. That’s about 4 quarters of funding available at the current rate of spending.

Financial year to date, were if not for the $60 million raised from issuing shares, Bubs would be underwater.

Bitcoin is beginning to beat credit cards: Ryan Clarkson-Ledward

Visa is in a bit of an arms race. Where companies like Microsoft, Meta, and Google are racing to pioneer AI, Visa is seemingly in a race to stay relevant.

It seems clear to me that the payment processor and credit card issuer is worried about bitcoin. So much so, they’re actively trying to catch up with their own crypto project.

Here’s what Visa’s ‘head of crypto’ had to say on Twitter this week:

We have an ambitious crypto product roadmap @Visa and just opened a few reqs for senior software engineers to help us drive mainstream adoption of public blockchain networks and stablecoin payments. https://t.co/UQRJNcOJtB

— Cuy Sheffield (@cuysheffield) April 24, 2023

The mainstream, of course, hasn’t given much mind to this little sideshow.

Few people see Bitcoin [BTC] or crypto as an immediate threat to banks or payments processors right now. After all, they’re still a very volatile and speculative asset class.

But, despite these constant surface-level criticisms, bitcoin continues to improve behind the scenes. In fact, one of the most exciting upgrades to the network and its blockchain, the Lightning Network, is beginning to really demonstrate its potential.

If you’re unfamiliar with the Lightning Network, it’s known as a layer-two protocol. It’s built on top of the bitcoin blockchain to deliver near instantaneous transactions at a fraction of the cost of the usual payment processors.

For example, most credit card providers, like Visa, charge businesses a 1–3% fee on each transaction. It sounds like a small amount, but it adds up over time.

By comparison, with the help of the Lightning Network, bitcoin could facilitate the same transaction for a fraction of the cost.

https://www.moneymorning.com.au/20230428/bitcoin-is-beginning-to-beat-credit-cards.html

Megaport surges 40% on EBITDA guidance upgrade

Down over 30% this year before today, Megaport (ASX:MP1) pared almost all of the YTD losses by issuing an EBITDA upgrade.

Megaport is currently up 45% after saying it expects normalised EBITDA ‘to be materially above market consensus’.

Tallying the average broker estimates, Megaport calculated the market consensus expecting EBITDA of $9 million in FY23 and $30 million in FY24.

However, management thinks the consensus is wrong.

Megaport now expects normalised EBITDA in FY23 to be in the range of $16 million to $18 million. Normalised EBITDA in FY24 is now expected to be in the range of $41 million to $46 million.

Quite the revision.

Pointsbet discusses potential sale of North American and Australian businesses

Tucked at the end of its quarterly release was a slide about potential ‘strategic transactions’.

As mentioned to the market before, Pointsbet said it ‘continues to engage in discussions regarding strategic transactions’.

PBH is currently talking with ‘multiple parties’ about selling part or all of its North American business. Some of these talks are ‘well advanced’.

Pointsbet also shopped its Australian business but terminated discussions with a particular party.

The stock is nonetheless discussing with ‘other third parties who have expressed an interest in acquiring our Australian business’.

Pointsbet’s operating cash burn hits $76.7 million in March quarter

Pointsbet continues to burn cash.

In the March quarter, the betting stock reported operating cash outflows of $76.7 million. Year to date (nine months), Pointsbet has burned through $180.2 million.

Pointsbet pocketed $109 million from customers in the quarter but spent $69 million alone on marketing! Marketing accounted for over 60% of customer receipts for the quarter.

Why is the company spending so much on advertising? Does management feel it can’t but spend big to bolster revenue?

Last quarter, PBH spent $67.5 million on marketing, generating $106 million in customer receipts on an operating cash burn of $59 million.

In the March 2022 quarter, Pointsbet’s marketing outlay was $54 million on customer receipts of $78 million and an operating cash burn of $58 million.

$PBH $PBH.AX continues to burn cash. #ASX #Pointsbet pic.twitter.com/KkfGePyJsh

— Fat Tail Daily (@FatTailDaily) April 28, 2023

Syrah Resources continues to slide

Struggling graphite producer Syrah Resources (ASX:SYR) continued to slide on Friday, down 10% at the open.

Syrah released disappointing arch quarter production results yesterday and revealed it will ‘moderate’ production in the coming quarters until trading conditions ‘warrant higher capacity utilisation’.

SYR didn’t quantify the production moderation.

$SYR continues to slide, opening nearly 10% lower on Friday. $SYR.AX is now down 50% in the past six months. #ASX #ausbiz #graphite https://t.co/JNxYPhOnXk

— Fat Tail Daily (@FatTailDaily) April 28, 2023

Brainchip collects US$40k in customer receipts for March quarter

In its December quarter report, Brainchip (ASX:BRN) — developer of neuromorphic AI chips — reported customer receipts of US$1.2 million.

In a statement, CEO Sean Hehir then said Brainchp will focus on ‘key sales targets and converting technical evaluations into paid licenses’ in the March quarter.

Today, the March quarterly was released.

It showed Brainchip collected just US$40,000 in customer receipts, way down on the US$1.2 million last quarter.

Brainchip’s operating cash outflow was US$6.1 million in the March quarter, meaning the stock had US$17.7 million in the bank at the end of March.

BRN has about 3 quarters of funding available.

Interestingly, this quarter’s CEO statement had an identical signoff as the December quarter:

“In the coming quarter, the Company will focus on key sales targets and converting technical evaluations into paid licenses. In addition, the Company is accelerating development of next-generation Akida IP and products to extend our technological lead and market opportunity. We remain positive on future market penetration and broad adoption of BrainChip’s technology.”

$BRN $BRN.AX pockets US$40k from customers in the March quarter and the CEO signs off with the same hopeful message as the December quarter. #ASX #ausbiz #brainchip pic.twitter.com/ZUQVEffGw5

— Fat Tail Daily (@FatTailDaily) April 28, 2023

Deluge of quarterlies released today

Good morning! Kiryll here.

We’ve got a lot of quarterlies to get through today.

Dozens upon dozens of stocks have released their March quarter results.

Here’s a teaser:

- Coles

- Lake Resources

- Brainchip

- Vulcan Energy

- Megaport

- Dubber

- Imugene

- IGO

- Mirvac

- Whispir

- Novatti

So let’s cover them.

Source: Bing AI

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988