ASX Today — Live ASX News | Myer Doubles Profit, Xero Cuts Jobs

ASX flat at the close

The ASX 200 ended flat on Thursday despite the information technology sector gaining 2.71%.

Xero was the best performer on the XJO, closing 10.7% higher after announcing layoffs and the exit of an underperforming subsidiary.

It feels like markets are in a holding pattern at the moment, waiting for definitive economic data that will offer clarity on the path data-dependent central banks will be forced to take.

The US Fed FOMC meeting is coming later this month but not before some crucial economic releases like the non-farms payrolls and unemployment data to be released on Saturday.

Thinking in unit economics

Warren Buffett likes to say he is a business picker, not a stock picker. The distinction lies in what you focus on. A business picker cares more about a company’s competitive advantage than its P/E ratio.

A business picker is also more likely to focus on unit economics — the foundational business unit at the core of a company’s business model.

As The Diff’s Byrne Hobart wrote earlier this month, identifying the unit economics of a business begins with identifying the ‘atoms’ of that business.

How do you do that?

“There’s no silver bullet here; you need to do some thinking—those units should, ideally, be:

- Fairly homogeneous, either in size (one US Netflix subscriber is pretty similar to another) or in behavior (a five-person company and a 5,000-person company both have some deployment pattern for new SaaS tools, where they start out with a small number of users on cheap or free plans and expand their seat count and price until they reach a steady state where growth is bounded by customer growth).

- Not easily divisible, because if they’re easily divisible the proper unit is whatever they divide into.

- Limited by discrete categories, ideally qualitatively: A Netflix model might build up revenue estimates by tracking ad-supported and non ad-supported users separately, for example. And that’s okay, but it’s hard to look at unit economics trends for companies that divide up their “units” by size, because it means individual constituents are switching from one bucket to another. Specifically, shrinking enough to drop below one cutoff makes the average revenue per customer above and below the cutoff rise.1

- And most importantly for valuing the business, it needs to be possible to match some costs to fixed unit-level costs, some to variable unit-level costs, some to unit acquisition costs, and some to expanding-the-set-of-acquirable-units or increasing-maximum-revenue-per-unit costs.

“This last point is where unit economics really shine as an analytical tool, because they let you convert all the complexity of a company into a fairly simple formula: there’s some cost to add a unit, whether that’s the cost of building a restaurant or the cost of marketing to a new customer. There’s some semi-predictable stream of cash flows from the acquisition of that unit. And that means growth can be converted into a net present value calculation: spend $1m building a restaurant that produces $150k in after-tax cash flows, growing 3% annually, and you can either a) say that you’re investing at an 18% internal rate of return, or b) say that at a 12% discount rate you’re converting $1m in expenses into an asset with a present value of $1.67m.”

Revaluing the US software industry

The way US software companies pay wages and report profits has inflated underlying earnings.

As FT’s Robert Armstrong argued yesterday, the industry’s ‘finances may be in for a reassessment. The implications for stock prices are obvious.’

“The illusion of extraordinary profitability is the fact that software companies pay their employees largely in stock. Many companies report adjusted profits excluding this form of pay.

“It is important to understand that this is an industry-wide issue. Mark Moerdler of AllianceBernstein calculates that over the past 10 years, as the good times have rolled, share based compensation has risen from 4 per cent to almost 12 per cent of revenue for global software companies, on average (median). In an industry with operating margins of 30-40 per cent, that means excluding SBC pumps up operating margins by as much as a third. At younger companies, the figure can be much higher: at Snowflake, a $45bn cloud software company, SBC was 42 per cent of revenue last year — all excluded from adjusted profit.

“Anyone who is valuing Microsoft (or other software companies) on cash flow and who doesn’t take the (considerable!) trouble to adjust for SBC is making a mistake. And to the degree that unadjusted cash flow drives software companies’ stock prices, the whole sector may be overvalued relative to other industries.

“In a note to clients last week, Ryan Hammond’s team at Goldman Sachs wrote that the difference between adjusted and unadjusted earnings is far larger in software than in any other sector. They expects that ‘the market backdrop will remain challenging for stocks with high SBC and low GAAP margins’ as higher rates increase the focus on real profitability. Here is their chart of the relative performance of the top and bottom quartile of the stock market companies, ranked by SBC as a percentage of revenue:”

“The average FCF for the 750 largest market capitalization firms is $2.67 billion as of April 2019. Adjusting for stock compensation this number drops to $2.47 billion, which translates to an average of about $225 million in stock compensation expense. This implies that on average, stock compensation expense increases the free cash flows for this group by about 10%. The variation is large, with about half the firms in the group having stock compensation expense that is less than 5% of FCF while the top 50 users of stock compensation enjoy an increase of about 230% to their free cash flows. To put this in perspective these 50 firms together are trading at a market cap/FCF multiple of 62 times (118 times excluding Google). If this multiple was applied to their corrected FCF it would result in a 66% decline in the market cap of the entire group (if we remove Google, the corrected combined FCF for the remaining 49 firms becomes negative, even though they represent $1.3 trillion in market cap). It is interesting to note that focusing on the top 5 largest firms by market capitalization, stock compensation expense accounts for 25% of free cash flow, which implies approximately $800 billion of overvaluation.”

Xero up 7% after announcing layoffs and Waddle write-off

Xero will cut 700-800 roles to ‘better balance growth and profitability’.

The layoffs will improve Xero’s ‘operating profitability as its operating expense to revenue ratio is expected to reduce significantly in FY24.’

The accounting software firm is targeting an operating expense to revenue ratio of 75% in FY24.

Xero maintained FY23 guidance for operating expenses as a percentage of operating revenue to be ‘towards the lower end of a range 80-85%’.

The restructure will cost about $25-35 million, with the majority of these payments slated for FY24.

Xero also announced it will exit the cloud-based lending platform Waddle. Xero acquired Waddle in 2020. The firm expects to incur a write down of $30-40 million in FY23.

Source: Xero

Tesla dumps rare earths — should you do the same?

Last week we witnessed a dramatic turn for companies tied to rare earths elements (REEs).

Australian producer Lynas Rare Earths [ASX:LYC] fell 11% last Friday, while Arafura Rare Earths [ASX:ARU] shed around 10%.

Chinese producers, accounting for around 90% of global production, also fell hard.

So, what drove the commodity-wide sell-off?

At its much anticipated ‘investor day’ presentation in Texas, Tesla revealed that it was looking to remove rare earth metals from its next-generation vehicles.

The market viewed this as a big deal in terms of the outlook for REEs…

Neodymium and praseodymium (NdPr) are two REEs used in permanent magnets for electric vehicles (EVs).

At first glance, Tesla’s announcement puts a major dent in the demand outlook.

But dig a little deeper, and things may not be so bad for this poorly understood commodity.

I’ll get to that point in a moment.

But first up, what’s at the root of Tesla’s change in strategy?

The answer…cost cutting.

According to Tesla, they’re looking to reduce manufacturing costs by up to 50% while also scaling up its global vehicle sales from 1.3 million to 20 million vehicles by 2030.

It’s all part of the grand plan to get EVs into the hands of the mass consumer.

However, the company was light on details…engineers outside Tesla ranks have little idea how the company is set to revolutionise its EV motor without rare earths magnets.

You see, NdPr magnets are the superior choice when it comes to EV production.

They offer significant performance benefits, enabling the development of compact, torque- and power-dense electric motors.

According to some experts, though, replacing rare earth magnets from its next-generation fleet will inevitably compromise efficiency.

In EV design, there’s a fine line between cost and performance.

But Tesla looks to be shifting dramatically toward the cost saving side…slashing production expenditure to deliver low-cost EV’s for the mass market.

It’s even looking to skip the critical step of building a prototype model in the name of saving cash and fast-tracking its newest model into production.

There’s valid reason car manufacturers build prototypes before going into mass production, and it goes beyond glossy magazines and marketing…

It’s a critical step that allows engineers to iron-out faults under normal driving conditions.

Any major failings could have a profound impact on the company’s long-term outlook…its PR could be shattered thanks to overreaching on cost cutting and expediating production.

That would pave the way for other manufacturers to capitalise on Tesla’s potential flaws and claw back market share in the EV mass-market race.

But with Tesla’s stock price capitulating almost 75% from its peak in November 2021 to its low in January 2023, the company is desperate to pitch something new…

https://www.moneymorning.com.au/20230309/tesla-dumps-rare-earthsshould-you-do-the-same.html

Myer leads All Ords with highest profit since 1H14

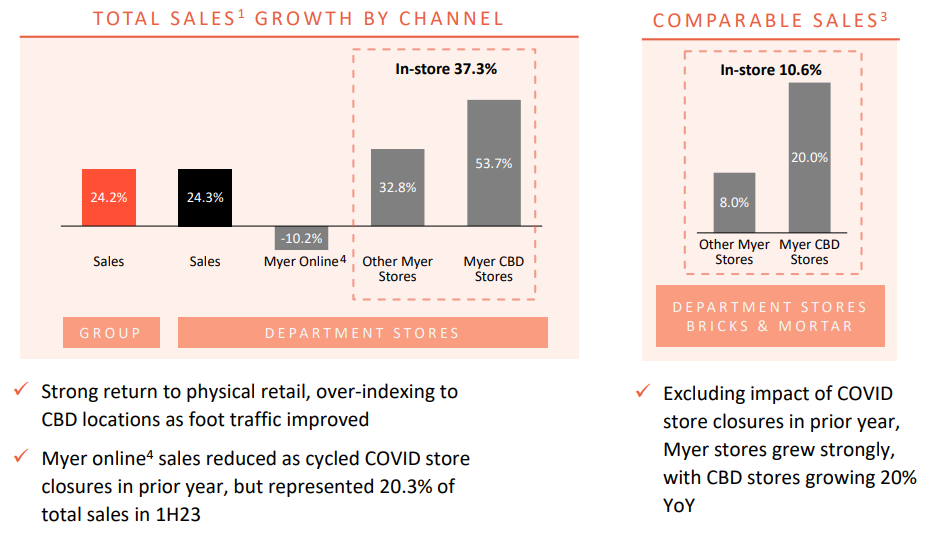

Myer is the best performer on the All Ords at midday trade after doubling its 1H23 net profit after tax to $65 million, the highest profit since 1H14.

Total sales for the 26 weeks ended 28th January 2023 rose 24% to a record $1.88 billion. Profit rose 101% to $65 million.

The strong performance led Myer to declare a special dividend of 4 cents per share, fully franked.

Myer CEO John King commented:

“We are very pleased with the strength and quality of our first half results, with a best-on-record first half sales performance, significantly improved profitability and a balance sheet that continues to provide a strong foundation for future growth. The result reaffirms our view that the Customer First Plan is the right strategy, which continues to deliver strong outcomes for our business and shareholders. Our omni-channel offer is strong, we continue to invest in MYER one, one of the country’s most effective retail loyalty programs and have also demonstrated our ability to capitalise on customers returning to stores and CBD locations through a targeted program of store space optimisation, a stronger merchandise offer, key refurbishments and improved customer service. Our ordinary fully franked dividend and additional special dividend demonstrates the confidence in the momentum being built as we move through FY23, with Department store sales growth in the eight weeks post Christmas up 16.1% over the corresponding period in the prior year; continuing to deliver sales momentum despite tightening economic conditions.”

Myer’s strongest sales channel was CBD stores, which rose 54% on 1H22, or 20% on a comparable basis when excluding lockdown periods.

Online sales fell 10% to $382 million as more customers returned to physical stores. However, since 1H20, the 3-year CAGR for Myer’s online sales is 31.5%.

Source: Myer

Piedmont Lithium and Atlantic Lithium in trading halts following short report

Lithium developer Piedmont Lithium (ASX:PLL) is in a trading pause pending an announcement.

The trading halt likely relates to a short report released yesterday by Blue Orca Capital.

Blue Orca Capital alleges it has found evidence that Piedmont’s mining licenses in Ghana were obtained via ‘corruption’.

Atlantic Lithium (ASX:A11) also entered a trading halt pending a ‘response being prepared to an online report’.

Piedmont owns a 9% equity interest in Atlantic Lithium and could earn a 50% stake in A11’s spodumene projects in Ghana.

Blue Orca alleges that Atlantic obtained Ghana mining licenses via secret payments to the immediate family of a high-level politician in Ghana.

The short seller said it does not think regulators in Ghana will ratify these licenses when they find out the licenses are “tainted by corruption”.

If Ghana authorities do not ratify the license, Piedmont’s Tennessee conversion facility is ‘dead on arrival’, argues Blue Orca:

“According to Piedmont, Atlantic’s Ghana mine is to be the primary source of spodumene for its Tennessee conversion facility. Without Ghana, Piedmont’s Tennessee facility, and any promise of material near term revenue from Tennessee, are dead on arrival. Supply of spodumene is so tight that if Piedmont loses its Ghana supply, as we suspect it will, Piedmont cannot simply replace the Ghana spodumene offtake with a different producer’s offtake. It’s too late for that – there is a massive supply shortage and there is no longer enough near term spodumene production available for offtake, especially the large quantities Piedmont needs to feed the Tennessee facility’s capacity. We interviewed a former Piedmont senior level executive about potential offtake options for Piedmont. His response: Piedmont has no options, it is “locked-in” and “has gotta make it work” with Ghana to make Tennessee work.”

$PLL and $A11 are in trading halts pending responses to Blue Orca's short report, which alleges corruption was involved in securing key mining licenses in Ghana.

If Ghana authorities fail to ratify the licenses, Blue Orca thinks Piedmont's Tennessee facility is 'dead on… https://t.co/RYmkS4j7My pic.twitter.com/Vu3Vbmgcew

— Fat Tail Daily (@FatTailDaily) March 8, 2023

Bank of Canada differs from US Fed, holds interest rates steady

The Bank of Canada is taking a different approach to its US counterpart, keeping its official interest rate steady for the first time since March 2022.

After eight consecutive increases, the Bank of Canada paused hikes to assess the effects of its tightening policy. The official rate still sits at 4.5%.

Headline inflation fell to 5.9% in the twelve months to January, down from a multi-decade high of 8.1% in June.

The central bank expects CPI to fall to 3% by the middle of 2023.

In a press release, the Bank of Canada noted:

“In Canada, economic growth came in flat in the fourth quarter of 2022, lower than the Bank projected. With consumption, government spending and net exports all increasing, the weaker-than-expected GDP was largely because of a sizeable slowdown in inventory investment. Restrictive monetary policy continues to weigh on household spending, and business investment has weakened alongside slowing domestic and foreign demand.

“The labour market remains very tight. Employment growth has been surprisingly strong, the unemployment rate remains near historic lows, and job vacancies are elevated. Wages continue to grow at 4% to 5%, while productivity has declined in recent quarters.

“Inflation eased to 5.9% in January, reflecting lower price increases for energy, durable goods and some services. Price increases for food and shelter remain high, causing continued hardship for Canadians. With weak economic growth for the next couple of quarters, pressures in product and labour markets are expected to ease. This should moderate wage growth and also increase competitive pressures, making it more difficult for businesses to pass on higher costs to consumers.

“Overall, the latest data remains in line with the Bank’s expectation that CPI inflation will come down to around 3% in the middle of this year. Year-over-year measures of core inflation ticked down to about 5%, and 3-month measures are around 3½%. Both will need to come down further, as will short-term inflation expectations, to return inflation to the 2% target.”

Jerome Powell reiterates rates message, markets raise hike bets

Jerome Powell reiterated his message on interest rates overnight in an appearance before the House Financial Services Committee.

In a speech otherwise identical to one he gave on Tuesday before Congress, Powell added that while markets took his comments on Tuesday as indication of a 50 basis point rate hike, the Fed’s decision will hinge on incoming data:

“I stress that no decision has been made on this … but if the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.”

Markets are now pricing in a near 80% probability of a 50 basis point hike, up from only 30% at the start of the week.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988