ASX Today — Live ASX News | ASX Down, US Headline Inflation Eases to Lowest In Nearly 2 Years

Inflation is conflict

What is the root of inflation?

Conflict.

So argues a paper published this month by MIT economist Ivan Werning and University of Chicago economist Guido Lorenzoni.

The pair sought to craft the most minimal and general framework that explains the mechanism for inflation. In other words, Werning and Lorenzoni wanted to find the ‘most proximate causes’ of inflation.

Their research led them to conflict:

This paper argues that the most proximate and general cause of inflation is conflict or disagreement.

In this view, inflation results from incompatible goals over relative prices, with conflicting economic agents each having only partial or intermittent control over. Due to nominal rigidities, agents occasionally change a subset of prices that are under their control. Whenever they do, they adjust them to influence relative prices in their own desired direction.

When coupled with staggered prices this conflict manifests itself in a finite level of inflation: the conflict over relative prices are largely frustrated. Despite a stalemate in relative prices, the changes in prices motivated by this conflict gives rise to general and sustained inflation in all prices.

In our view, traditional ideas and models of inflation have been very useful, but are either incomplete about the mechanism or unnecessarily special. The broad phenomena of inflation deserves a wider and more adaptable framework, much in the same way as growth accounting is useful and transcends particular models of growth. The conflict view offers exactly this, a framework and concept that sits on top of most models. Specific fully specified models can provide different stories for the root causes, as opposed to proximate causes, of inflation by endogenizing conflict. Conflict is the most general and proximate cause for inflation.

Westpac chief economist: surge in consumer sentiment could have been stronger if not for RBA’s qualification

Bill Evans — Westpac’s chief economist — added an interesting wrinkle to this week’s survey results measured by the Westpac Melbourne Institute Index of Consumer Sentiment.

As has been widely reported, sentiment rose a substantial 9.4% to 85.8.

Evans said his team initially attributed the spike solely to the RBA’s decision to hold its cash rate steady after ten consecutive hikes. For instance, confidence of respondents with a mortgage rose 12.2%.

But after unpacking the survey results further, Evans stumbled upon something more interesting.

The survey was conducted over four days by phone and online between Monday, April 3 and Thursday, April 6.

The Reserve Bank’s interest rate decision was handed down on Tuesday, April 4, at 2.30pm.

Since the survey’s phone interviews are conducted after 3pm, you can assume that most of the survey’s Day 2 results were recorded after the RBA decision. Meaning you can compare consumer confidence immediately before the RBA’s decision and immediately after.

Here is the breakdown of results:

The results for the Index on each of the days (with sample size in brackets) were: April 3: 89.2 (525); April 4: 81.0 (287); April 5: 83.4 (324); April 6: 85.8 (64).

Readers will be surprised, as we were, that the print BEFORE the RBA’s decision was announced was much higher than the print on the days AFTER the decision.

The sample sizes for each of the first three days are large and certainly statistically significant.

Evans thinks the peculiar result can be pinned on Philip Lowe’s statement that further hikes may be necessary if inflation remains persistent:

The lower read following the announcement was most likely in response to the Governor’s comment, “The Board expects that some further tightening of monetary policy may well be needed to ensure that inflation returns to target.”

This qualification of the pause may have discouraged highly expectant respondents, with the Index falling by 9.2% on the second day of the survey. The Index recovered somewhat on the third day by 3.0%.

Westpac’s chief economist then offered a historical comparison, identifying the tightening cycle in 2009/10 as the best analogue:

The most comparable cycle to the current tightening cycle was the 2009/10 cycle when the RBA raised the cash rate at every meeting between October 2009 and May 2010 (with the exception of February).

When the Board paused in June 2010 Sentiment initially fell by 5.6% as Consumers were still sceptical about a sustained pause. Following a second pause at the July meeting Sentiment surged by 11%.

These results indicate that when Consumers become convinced that the Board is pausing for an extended period there is considerable scope for the Index to surge back to more normal levels.

This interpretation suggests that a second pause after the May Board meeting would be met with another significant lift in Sentiment as sceptical Consumers became more comfortable that rates had peaked – just as we saw in July 2010.

How might Sentiment respond to a rate increase at the May Board meeting?

The reasonable conclusion from this note is that because Consumers remain cautious about the rate outlook the extent of the likely negative response to a May rate hike may be quite muted.

Westpac's consumer sentiment survey results BEFORE the #RBA's decision were 'much higher' than the results on the days AFTER the decision. #auspol #ausbiz pic.twitter.com/RvBSSEkE47

— Fat Tail Daily (@FatTailDaily) April 13, 2023

Milkrun’s collapse a high-profile miss for Aussie VC firms

This week, the AFR reported grocery delivery service Milkrun will wind down and make its whole workforce redundant.

Raising fresh funding proved a challenge this year and Milkrun’s continued cash burn meant the firm could not survive without a capital injection.

Milkrun will cease trading this Friday.

Milkrun’s closing will sting for several prominent local VC firms who invested in the grocery deliverer, including AirTree Ventures, Skip Capital, and Grok Ventures.

In January last year, AirTree’s partner Jackie Vullinghs wrote a blog post explaining the firm’s investment in Milkrun.

Vullinghs wrote that the grocery shopping experience is ripe for disruption:

‘Clearly, there’s an opportunity for a new company to improve the grocery shopping experience for a convenience-led world, delivering groceries in minutes at supermarket prices.

‘Grocery is a $122bn market in Australia, dominated by slow-moving incumbents with low NPS.

‘The population is urbanised, wealthy, and willing to pay for on-demand food delivery (Melbourne & Sydney are in the top 5 cities globally for Deliveroo).’

While admitting the grocery segment is ‘traditionally a low margin category’, AirTree thought an upstart like Milkrun could shake things up with ‘improved unit economics in multiple areas’:

-

‘Personalisation: With an app that uses data effectively, you can personalise the shopping experience for each consumer, increasing average basket size and improving frequency and retention.

-

‘Range localisation: A smaller retail footprint in lower-cost areas, combined with a solid data infrastructure allowing a granular understanding of which products sell in which suburbs, enables lower leases, wastage and inventory costs.

-

‘Vertical Integration: Having a direct to consumer relationship leads to constant customer feedback. With that feedback, you can create new products directly with producers and expand product margin.

-

‘Range Expansion: Over time, you build up a dense network of micro fulfilment centres throughout cities, allowing you to expand into higher-margin products and potentially partner with other brands that want to deliver a delightful consumer experience.’

Vullinghs said the extent of what Milkrun achieved up to that point in early 2022 gave AirTree a ‘glimpse of the extraordinary things they’ll make possible in the future’.

That glimpsed future proved to be illusory. But the curdled Milkrun investment has not dented AirTree’s confidence.

In correspondence obtained by the AFR, AirTree told investors failure is an ‘inevitable part’ of venture capital.

“Failure is an inevitable part of VC. With great upside potential comes risk, and if we don’t see some failures, we’re likely not adding enough risk into the portfolio for outliers to emerge and become fund returners. With that said, this wasn’t the outcome we hoped for.”

ABS: unemployment rate remained at 3.5% in March, reflecting ‘tight labour market’

According to the latest data from the Australian Bureau of Statistics, the unemployment rate remained at 3.5% in March.

The Australian economy added around 53,000 jobs and the number of unemployed fell by 1,600 people, leaving the unemployment rate at a near 50-year low of 3.5%.

The unemployment rate has remained at 3.5% for the eighth consecutive month.

ABS head of labour statistics Lauren Ford said the latest labour data reflects a ‘tight labour market’, with employers ‘finding it hard to fill the high number of job vacancies’.

Ford also noted the female participation rate rose to a record high of 62.5%.

Ryan Clarkson-Ledward: Bitcoin is the quiet achiever of 2023

Year to date, Bitcoin [BTC] is up an incredible 80%!

That’s an incredible result compared to a lot of the volatility we’re seeing in other assets. And yet, most people probably haven’t even noticed.

The mainstream media, which couldn’t get enough of the 2021 crypto boom, has gone cold on the subject. After all, despite the 80% gain for 2023, the price of bitcoin is still sitting around US$30,000.

That is still well below its all-time high of US$68,789.

Until that record is broken, I wouldn’t expect to see bitcoin dominating any headlines. Not that that matters, of course…

Bitcoin’s greatest strength has always been its disinflationary design. Because while speculation may lead to incredible price peaks and troughs, the fundamental reward structure of bitcoin is what ensures its longevity.

In fact, one of the most important features of bitcoin is that it gradually becomes harder to ‘mine’. This is a process that is known as ‘halving’.

If you’re unfamiliar with the term or the process, check out this article from Sam Volkering around the time of the last halving.

Back in May of 2020, when this last halving occurred, one bitcoin was worth roughly US$8,605. Nearly a year after that, in April 2021, it would be worth closer to US$50,000.

Granted, the halving certainly wasn’t entirely responsible for this huge price spike. But it certainly played a part in the speculative frenzy. Because with each occurrence it becomes harder to mine bitcoin and, therefore, rarer to own and buy.

Of course, I’m telling you all of this because another halving event is on its way…

We’re roughly a year away from the next milestone moment for bitcoin.

https://www.moneymorning.com.au/20230413/bitcoin-is-the-quiet-achiever-of-2023.html

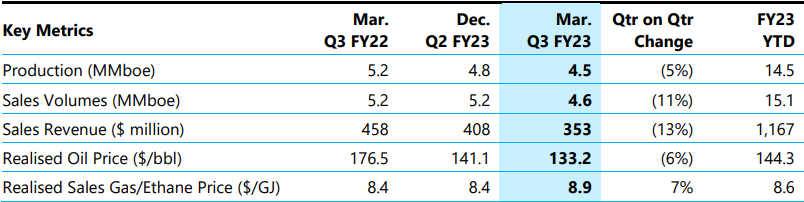

Beach Energy: quarterly production down

Oil and gas producer Beach Energy (ASX:BPT) released its 3Q23 production report today, showing production was down 5% quarter-on-quarter to 4.5 MMboe. Production fell 13% year-on-year.

Beach Energy said gas production was impeded by several factors, chief among them a 10-day planned downtime at Otway Basin, lower nominations partly ascribed to surplus gas available during Queensland LNG outage, and unplanned outages at its Cooper Basin JV.

Sales revenue fell to $353 million — a 13% drop QoQ and a 23% drop YoY.

4DMedical clarifies US hospital SaaS contract

Respiratory imaging technology firm 4DMedical (ASX:4DX) was up over 100% in a week after announcing last Wednesday it signed its first US hospital SaaS contract with the University of Miami spanning five years.

The contract is to provide the university XV LVAS (X-ray velocimetry lung ventilation analysis software) ventilation reports.

Today, 4DMedical clarified the financial benefit of the contract, sending it shares 14% lower.

4DX said the minimum guaranteed fees to be paid to it are in the range of $1 million to $1.5 million for the five-year term.

4DX said it will earn additional fees ‘for additional scans beyond those covered by the minimum fees’.

ASX opens 0.20% lower, Corporate Travel jumps 10% on material customer contract win

The ASX 200 opened 0.20% lower on Thursday.

Recent short-report target Block (ASX:SQ2) is the worst at the open, currently down 6%. Block is dual-listed on the Nasdaq and that tech-heavy index closed 0.85% lower overnight.

The best performer currently is Corporate Travel Management (ASX:CTD), up 10%.

Corporate Travel announced a ‘material customer contract’ by the UK Home Office this morning. CTD said the UK Home Office estimated the contract at ~$3 billion TTV, spanning two years with an option to extend.

Corporate Travel said the contract will have a ‘significant impact on the further growth of our European region in FY24 and beyond’.

Core inflation trend remains a concern

For the first time in over two years, US core inflation came in above the headline measure. So which should you care about more?

Economists — and the Fed — prefer to look at the core CPI figure as it excludes volatile items, giving a rounder picture of underlying inflation in the economy.

And core inflation is not abating.

If we eschew annual comparisons and focus on shorter intervals to gauge trends, we see that core inflation has been elevated over the past 3-5 months.

Source: Jason Furman

Some reasons to expect inflation to slow, like lagged shelter & possibly labor cooling.

But would be a mistake to extrapolate from the fact that inflation is slower now than 6 months ago to predict it will be even slower 6 months from now. Best to think of a ~4% pace.

— Jason Furman (@jasonfurman) April 12, 2023

US core inflation remains sticky as headline CPI falls

The biggest story today is the US inflation data released overnight.

Headline inflation rose 5% year on year in March, down from February’s 6% increase. It was the smallest gain since May 2021.

However, core inflation — which excludes food and energy — rose 5.6% from a year earlier, actually slightly higher than the 5.5% increase in February.

Month on month, March headline CPI rose 0.1% while core CPI rose 0.4%.

The persistence of core inflation means another 25 basis point hike by the Fed is likely. The majority of traders are betting on a 25 basis-point hike at the Fed’s May meeting while still wagering the central bank will cut later this year.

Headline CPI in March

3-month annualized change: +3.8%

6-month annualized change: +3.6%Core CPI in March

3-month annualized change: +5.1%

6-month annualized change: +4.7% https://t.co/nx9Te9qL9f pic.twitter.com/PtzrXAsnlz— Nick Timiraos (@NickTimiraos) April 12, 2023

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988