ASX News Today LIVE | XJO Gains 0.6%, Tech Stocks Notch Solid FY23

Gold miner Ten Sixty Four calls in voluntary administrators

We have FY24’s first casualty.

Gold miner Ten Sixty Four [ASX:X64] entered voluntary administration only a fortnight after the appointment of a new Board following a mass resignation of previous directors.

The new Board pointed to a dispute concerning the ‘alleged transfer of ownership of a 60% interest in X64’s subsidiary Philsaga Mining (PMC).

While the dispute goes unresolved, X64 ‘has no guarantee of continued income from PMC to support its operations’.

Cue the administrators.

X64 said it has a ‘strong desire to restructure the group and allow it to continue operating sustainably into the future’.

Melbourne Institute’s monthly headline inflation gauge for June rose 0.1%

The Melbourne Institute monthly headline inflation gauge rose by 0.1% in June with the annual rate edging down from 5.9 per cent to 5.7 per cent.#ausecon #inflation #business #Australia @CommSec pic.twitter.com/kSZx0mHsMA

— CommSec (@CommSec) July 3, 2023

ASX 200 begins FY24 with a 0.6% gain

Aussies shares closed the first trading session of FY24 on a positive note as the #ASX200 added 43pts or 0.6% to 7246. IT and healthcare were the only two sectors to lose ground while consumer discretionary (+1.4%) fared best. Miners and energy sectors also stood out.

— CommSec (@CommSec) July 3, 2023

What to look for when looking for income stocks

Excerpt from Greg Canavan’s latest Insider piece.

***

From 1 July 2021 until now, the ASX 200 has pretty much gone sideways. That’s two years of nothing.

But it’s been a wild ride over those two years.

To be precise, the ASX 200 is down about 2.5% over that time. That’s not really how markets are supposed to work, is it? I mean, you’re meant to get rewarded for the risk you take on.

Except there’s not much in the way of rewards for investors during an aggressive rate hiking cycle. You just have to suck it up and try and stay out of trouble.

On the plus side, when you take dividends into account, your head is just above water.

Over the same two-year timeframe, the ASX 200 Total Gross Return Index is up around 6%. That’s slightly misleading, though. This index takes into account the benefit of franking credits. So, unless you’re in a zero-tax environment, you won’t have experienced this return.

Anyway, the point I’m trying to make is that income has been the difference over the past few years, while capital growth has disappointed.

Now, I might be going out on a limb here, but my guess is that two years ago, how to secure a reliable income stream wasn’t really the main thing investors were thinking about.

Mid-2021 was bull market central. It was all about cryptos, SPACS, and wind farms…

Income was for losers.

But now, income is cool. Term deposits are back, baby! 4.5%? I’ll take some of that, please.

So I’m thinking…how will hindsight judge this mindset in two years’ time?

It’s a tough question to answer. On the surface, it makes sense to be looking for income opportunities right now. With the RBA hiking rates and expected to keep them higher for longer, ‘risk-free’ options like cash and term deposits look pretty good.

The lagged impact of the rate rises will continue to slow the economy in the second half of the year. Oh, and there is $60 billion of the RBA’s term funding facility (AKA low-cost fixed rate mortgages) due to be repaid in the September quarter.

That higher cost of financing will hit households immediately and then spread through the economy in the months following.

So yes, company earnings are under threat, and that means capital is at risk. Hence the desire for income.

This strategy certainly makes sense. But that doesn’t mean you opt for income at any cost.

Firstly, there is the contrarian angle to consider. As I said, two years ago, no one was interested in income. That’s because rates were pinned to the ground, and you had to be in the market to get anything.

The case for income AND growth

But now, cash rates are at their highest in a decade. That’s NOW, though. What about in two years’ time? They could well be much lower again. And if that’s the case, growth assets are the place to look.

But that doesn’t mean you need to abandon the search for income. There is an income/growth sweet spot developing in the market right now. It’s giving you the opportunity for a juicy dividend yield AND growth.

While the ASX 200 might be flat over the past two years, there are plenty of stocks that are down significantly from their highs.

In many cases, these stocks offer prospective dividend yields well above the cash rate AND trade significantly below a reasonable estimate of intrinsic value.

The way I see it, you can get a decent yield while waiting for the tightening cycle to play out. Then you’re in a good position to benefit from the eventual tailwind of a post-recession/slowdown easing cycle.

Now, I may be getting ahead of myself. But I’m looking two years out here. As the past two years have shown you, a lot can happen in this relatively short timeframe.

All this is to say that if you just focus on the yield and not the price you’re paying for that yield, you’ll get into trouble. Especially in a market where more profit headwinds are likely, as the lagged impact of previous monetary tightening works its way through the economy.

I’ve just put a report together detailing my six top dividend picks in the market right now. Fair warning, though…you won’t see many of these in your traditional income portfolios.

That’s because I’m focusing on out of favour, deep value plays first, and income second. The yields are still very attractive, it’s just that they come with a value overlay. That makes them ‘unusual’, unpopular picks.

But these are the attributes that will hopefully give your portfolio a boost in the next few years.

The commentariat places its RBA bets

The financial community is placing its final bets before tomorrow’s Reserve Bank board decision.

Here’s macroeconomist Warren Hogan opining in the AFR:

‘The lessons of the 1970s couldn’t be clearer; not only do you need to get inflation back to target after such a significant overshoot, but you must maintain a moderately tight stance of policy for an extended period to stop inflation taking off again.

‘And this is where real damage to inflation expectations is done; when the inflation re-emerges after a short lull to convince all the players in our economy that this is the new normal.’

Hogan then invokes a great golf analogy:

‘To quote the great Ben Hogan: “Golf is a compromise between what your ego wants you to do, what experience tells you to do, and what your nerves let you do.”

‘The RBA’s ego wants them to pause, their experience tells them to increase, may be even by 50 basis points, but their nerves are shredded after two years of serious missteps. They will probably pause.

‘Indeed, the easiest thing to do is keep grinding out 25-basis-point rate increases until the RBA board is comfortable with the trajectory for the economy and inflation.’

What does Hogan think the RBA should do? Pause for another month … but with qualifications. The strong labour market presents grave risks for protracted high inflation:

‘I still think there is a chance that we can get through this with a softish landing; a scenario I have been characterising for almost a year as the ‘rough landing’. To stay on this path, we probably need to pause the tightening cycle for another month.

‘But if the fires of labour demand are not looking like petering out with an interest rate above 4 per cent, then the debate will not be about a 4.6 per cent or even 4.85 per cent peak cash rate; it will be about whether we are going to 5.5 per cent or something a bit higher.’

The RBA now has good cause to pause https://t.co/5AKbCjrq1q

— Warren Hogan (@_warrenhogan) July 3, 2023

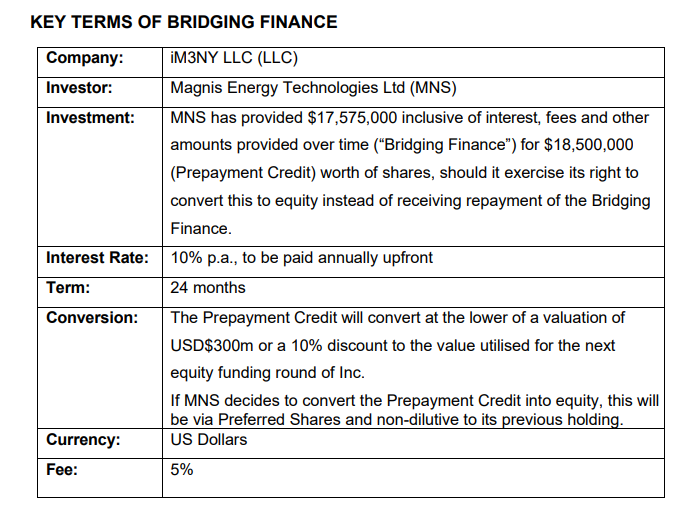

Magnis Energy raises stake in iM3NY, shares jump

Magnis Energy [ASX:MNS] is up 18% at the time of writing, having increased its interest in the iM3NY battery plant in New York to 73%.

The raised ownership followed the conversion of a bridging facility first announced on 31 March, 2023. The key terms of that facility are set out below:

Source: Magnis Energy

Rather than seek repayment of the bridging facility, Magnis decided to up its stake in iM3NY, as the battery plant is ‘likely entering the stage of commercial field trial sales from production batches in the current quarter.’

Magnis today also announced it entered a new ‘small-scale short term debt financing facility’.

This unquantified facility will provide ‘additional support to iM3NY’ but also ‘provide additional working capital to Magnis itself’.

Six best stocks for the new financial year: Ryan Clarkson-Ledward

Aussie investors deserve to feel a little peeved.

We’re in a similar spot economically to the US, we just don’t have the luxury of five companies lifting the rest of the market. Instead, our usual profit powerhouses — the banks and big miners — have delivered only modest gains.

So, should you give up on the ASX and go all-in on the NASDAQ?

Absolutely not.

Because as tempting as big tech may be, I think Aussie investors should be optimistic about local stocks. There are a lot of bargains on the market right now, and a whole lot more value in Aus relative to the US.

Of course, not every single stock fits this bill, but there are more hidden gems than you might think.

It just takes a little effort to find them, mostly because they’ve been dragged down by everything else.

The exact opposite of US markets…

Take Pepper Money [ASX:PPM], for example.

This $620 million market cap stock has been stuck on the market rollercoaster all year. And despite being up 11.9% for FY23, it should probably be trading even higher.

That’s because if you look beyond share price volatility, the fundamentals of this business are pretty fantastic.

Take a look at the following chart and data:

Source: Market Screener

Sales continue to grow and are forecast to keep growing.

Earnings are expected to remain stable for FY23 and bounce back in FY24 and FY25. And net income will do the same.

For a company that specialises in consumer loans and mortgages, that’s a decent outlook, particularly as most analysts are pretty sour on the sector with interest rates as high as they are.

But that’s not all…

https://www.moneymorning.com.au/20230703/these-are-the-six-best-stocks-for-the-new-financial-year.html

‘Brutal’ year for ASX small caps offers ‘opportunity not seen for some years’

Another asset manager has come out and said the recent turbulence on the Aussie market offers gainful opportunity.

Small-caps focused DMX Asset Management just came out and said the ‘brutal’ performance of the small-cap sector ‘provides an opportunity not seen for some years’.

The asset manager then shared a nice table showing the median 12-month returns by sector and market capitalisation.

The smaller the stocks, the bigger the beating sustained over the past 12 months.

(Although a question: on any given year, what’s the probability of the sub-$100 million stocks under-performing the $1b+ stocks? What’s the comparative baseline?)

It has been a brutal year for ASX investors in smaller companies (like ourselves). Below are the median 12-month returns by MC range and sector. We think this provides an opportunity not seen for some years. We will discuss more in our upcoming monthly newsletter. pic.twitter.com/9cmb5J8WNT

— DMX Asset Management (@DMXAsset) July 3, 2023

Argosy Minerals up 5% on company update but ‘mindful’ of ‘prolonged’ permitting process

Developer of the Rincon Lithium Project in Argentina, Argosy Minerals [ASX:AGY] is up 6% nearing midday trade after issuing a company update.

Argosy said it is ‘progressing the 2,000tpa facility commissioning works, which have advanced to successful 24-hour trials of continuous operations.’

Argosy expects to ramp up production operations during the second half of calendar 2023 — so in the next six months or so.

AGY also said it produced 20 tonnes of battery quality lithium carbonate product so far, with an average product quality of 99.79%.

Argosy also whipped out a stellar example of legalese verbiage regarding its quest for a strategic partner:

‘The key objective of the strategic partner process was to assess, then select via mutual alignment to secure funding and long-term off-take arrangements for the 10,000tpa expansion operation from a tier-1 counterparty in the EV supply chain. The Company has undertaken a comprehensive and thorough process, including multiple phases (due to significant and increasing interest with varying propositions) during the course of the lithium market uplift over the past 2.5 years, and this process is now nearing finalisation.

‘The Company was not constrained by a set deadline, preferring to achieve a favourable deal for stakeholders and a mutually beneficial partnership, aligned for the long-term sustainability and strategic benefit of the parties. As such, the Company is progressing to finalise the key agreements for such, via an off-take agreement for long-term battery quality lithium carbonate product supply and a finance agreement for the 10,000tpa operation funding.’

The takeaway?

The process is ‘nearing finalisation’.

And what about permits? That’s a vital point of contention for developers.

On that front, Argosy admitted the ‘constraints encountered … have prolonged this process’:

‘The 10,000tpa operation regulatory approval process is ongoing, however the Company is fully engaged with the Salta regulatory authority to expedite official approval receipt. The commitment of both parties to achieve this is reflected by the continued engagement to resolve the limited outstanding items, being clarification of hydrogeological queries related to the EIA submission, with a view to finalising and obtaining formal approval notice from the Mining Secretary.

‘The Company is maintaining regular and direct communication with the key regulatory authority officials and is mindful of the constraints encountered that have prolonged this process. However, it has not considerably impacted the project strategy, and in a period of increasing lithium market intensity and interest, this has resulted in improved strategic and long-term outcomes for the Company.’

Universal Store and Dusk continue to rebound

The mini-rally in bombed out consumer discretionary stocks continued on Monday.

Youth apparel retailer Universal Store [ASX:UNI] is up 7% this morning, and up 25% since late June.

Home fragrance merchant Dusk [ASX:DSK] is up 7% this morning, too. Since late June, Dusk is up nearly 30%.

An inevitable bump after being oversold or something more sustained, more bullish?

Greg and I discussed this very topic in the latest episode of What’s Not Priced In.

Rhythm Biosciences jumps 18%

Diagnostics technology developer Rhythm Biosciences [ASX:RHY] is up nearly 20% this morning.

The catalyst is seemingly an announcement that it has ‘further progressed its market entry strategy for ColoSTAT’ in the UK by establishing a fully-owned UK subsidiary.

RHY thinks the establishment of the subsidiary will help engage potential customers:

‘Having a local presence in the UK will provide the parent company the opportunity to engage directly with local customers and direct involvement with the supply chain requirements of ColoSTAT.’

Rhythm’s ColoSTAT is a blood test screening for colorectal cancer.

The announcement was not classified as market sensitive, however.

So is there a different reason the stock is moving?

Or is the administrative achievement of registering a subsidiary somehow a signal of RHY’s long-term intentions to commercialise ColoSTAT in the UK?

PSC Insurance down 10% after ASX price query response

Insurance services business PSC Insurance [ASX:PSI] is down ~10% in early trade after responding to the ASX’s queries about its recent price action.

PSI’s stock jumped 15% last Friday on no announcement from the firm, which caught the exchange’s eye.

PSC Insurance did shoot down any acquisition rumours, saying:

‘PSI are always seeking acquisition opportunities and at any one time we have a number in progress. We do not presently have any acquisitions in the pipeline that are significantly progressed or certain to proceed to execution or completion, further noting that none of these are at a stage where disclosure to the market would be required.’

Morningstar: ‘humble’ neighbourhood mall trading below fair value

Morningstar just published some research profiling a REIT ‘well-positioned to capitalise on long-term population trends’.

The real estate investment trust HomeCo Daily Needs REIT [ASX:HDN] stood out to Morningstar’s analysts due to its ‘portfolio of strong neighbourhood malls, large-format retail and health and services properties’.

But the REIT has struggled this year, down ~15% since February.

Initiating coverage on the stock, Morningstar’s Alexander Prineas wrote:

‘The main opportunity lies in converting lower-rent large-format retail to more attractive neighbourhood shopping centres, which typically command higher rents and are less cyclical than large-format retail.

‘Key valuation inputs are weighted average cost of capital of 7.2%, above-peer 3.5% estimated rental uplifts on existing leases for the next decade, and our expectation that HomeCo redevelops and remixes some malls.

‘Despite lower rents per square metre, large-format retail margins are reasonable due to low operating costs, and the REIT has been achieving good rental growth off a low base. The sizable weighting to bulky household goods retailers means exposure to new household formation.

‘HomeCo has longer-term tailwinds given it is likely to benefit more from population growth than rival REITs. HomeCo estimates population growth in its catchment areas of 1.9% from 2021 to 2026, versus a 1.5% nationwide average, a reasonable estimate given government policies support population growth and housing supply.’

New financial year, new opportunities

FY23 has come and gone.

What will FY24 bring?

More opportunities and hidden gems, according to Jun Bei Liu, lead portfolio manager for the Tribeca Alpha Plus Fund.

Bei Liu thinks the ‘best opportunities often emerge during times of market distress and dislocation’:

‘It is essential to recognise that the fluctuations and near-term weaknesses in the market are not indicative of a bleak future. Instead, they present a window of opportunity to identify undervalued assets with immense growth potential.

‘Sharemarkets are forward-looking and investors are trying to assess a company’s earnings potential 12 to 18 months ahead. As the momentum in downgrades to company earnings picks up in the coming months, savvy investors can capitalise on the dip in share prices that can potentially result in fruitful returns.’

"As we begin a new financial year, there are many enticing opportunities in Australia’s sharemarket, where bargain-hunting investors can uncover hidden gems with remarkable potential for growth and profitability."

👍👍👍https://t.co/3L3kdMfsTb— Callum Newman (@CalNewmanFT) July 2, 2023

Will the RBA raise rates tomorrow?

To raise or not to raise, that is the question.

The Reserve Bank board convenes tomorrow and another 25bp hike is on the menu.

What will the board decide?

The #RBA meets on Tuesday.

Will it raise rates or not? #auspol #ASX

— Fat Tail Daily (@FatTailDaily) July 2, 2023

Good morning, investors!

Good morning!

Hope you all had a relaxing week.

But now is the time to get back on the markets grind. We’ve got a busy one — what with the Reserve Bank meeting tomorrow.

As always, the question is will they or won’t they.

Here’s Bing’s depiction of a hedge fund manager perusing annual reports. Let’s hope his investing nous is as dexterous as his hands.

Source: Bing AI

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988