ASX News LIVE | XJO to Rise, S&P 500 Hits Record High as Megacap Tech Lifts Market

Market close update

The ASX 200 closed up 0.75% at 7,476.6 in a solid day for the Aussie benchmark.

Only Utilities and Materials were in the red today, with the rest of the market enjoying strong gains.

Discretionary closed the highest, up 1.68%, followed by Staples, up +1.33%.

Tech and Financials also had a great day with some big moves in individual stocks.

Stealing the show today was Zip, up 16.5% after saying it would return to semi-annual profitability for the first time since 2021.

Other big moves were seen by Block, up 3.1% and Life360, which rallied 4.8%.

The A2 Milk Company also recovered from recent losses, gaining 6.3%, while Star Entertainment also gained 5.1%.

The Big Four banks also had a strong day, with all up over 1%.

For now, it seems commodity prices will be the big thing to watch in the coming months as miners struggle with depressed prices across the battery metals supply chain.

China PBOC keeps rates on hold

China’s PBOC kept the one-year loan rate at 3.45%, in line with analyst expectations.

The move has seen China’s commercial banks also hold their lending rates in line with the decision.

Meanwhile, the five-year rates were also held at 4.2%, which is seen as the benchmark for mortgages.

The move comes after last week, when The People’s Bank of China (PBOC) refrained from reducing its rate on one-year policy loans and maintained its reserve requirement ratio (RRR).

All of this means China is holding back from large stimulus as it is wary of flooding the economy with monetary stimulus despite the economic woes.

Chinese stocks are down again today as the Chinese indices struggle.

The CSI Index is down -0.5%, while the SSE is down -0.86%.

The worst hit is the Hong Kong Hang Seng Index, which is down -2%. That is below 15,000, which is back to value at the 1997 handover of Hong Kong back to China.

Wow. The Hang Seng Index just fell below 15,000. It's at the same level as during the 1997 handover… pic.twitter.com/brYtnniRXJ

— David Ingles (@DavidInglesTV) January 22, 2024

Liontown loses loan as lithium prices remain down

Liontown Resources [ASX:LTR] has seen its share price drop by -21.13% today as the company lost its $760 million loan.

In its announcement, LTR said that it had ‘commenced discussions on a revised, smaller debt facility that will reflect the project review,’ but how much that actually ends up is still unknown.

The purpose of the loan was to support the company while it was pre-revenue and starting development of the Kathleen Valley mine in WA.

The miner was forced to take the loan after the failed takeover bid of Albemarle, which was worth $6.6 billion.

Liontown said it had $515 million cash on hand at the end of the year after drawing down existing available debt but markets are still concerned that the sum might not be enough to finish the project.

They assured investors that it would cover the cost of construction at Kathleen Valley but even if it finishes without issue, the larger problem is in the lithium prices.

Spodumene prices have fallen by close to 90% since January 2023, with the price now around US$7,500-7,790 per tonne.

The rapid fall of the key battery material has also affected similar critical battery materials, with nickel, palladium, and other rare earths also taking a beating.

Market expectation of Fed rate cuts

Here is another great chart by Jim Bianco outlining the changing expectations of future rate cuts at the Fed.

The important two to watch are the green and brown, which track the expectations of rate cuts in March and May.

The market has slashed bets recently that cuts are coming earlier, although expectations for the May meeting are still at 85% change of cuts.

My bet is that the cuts are coming later as inflation fears jump, as seen in the TIPS rate. Are markets still ahead of the Fed in cuts?

1/4

When will the Fed cut rates? What is the market pricing?

The red line is the next Fed meeting (Jan 31); only a 2% probability of a cut is priced in.

The brown line is the March 20 meeting. It has been fading; on Friday, it fell under 50% for the first time in a month.… pic.twitter.com/TlKDGbN92f

— Jim Bianco (@biancoresearch) January 21, 2024

Midday market update

The ASX 200 is up by 0.64% to 7,469.0 at midday. The move follows a strong US rally after the tech megacaps pushed the S&P 500 into records at the end of last week.

Australian tech followed suit today with strong gains seen by Block, which is up +2.88%. Zip is also one of the stand-out stocks today, up 11.02%, while accounting tech company Xero gained +2.24%.

Materials, Energy, and Utilities were the only sectors in the red today after a number of output downgrades weighed on the materials markets.

Commodity stocks have been under pressure after a raft of warnings from mining companies about falling metal prices–from copper to nickel and lithium.

Exploration activities and operations at some sites have been shuttered as a response. Former Fortescue chief executive Andrew Forrest announced the shutdown of the WA nickel mine in Wyloo as part of the cost-cutting.

Mining giants were subdued, with BHP Group up by +0.24% and Fortescue Metals flat. Rio Tinto was down -0.18%, but lithium stocks were again down.

Sayona Mining fell by -6.67%, Mineral Resources is down by -7.33%, and Pilbara Minerals lost -5.04%.

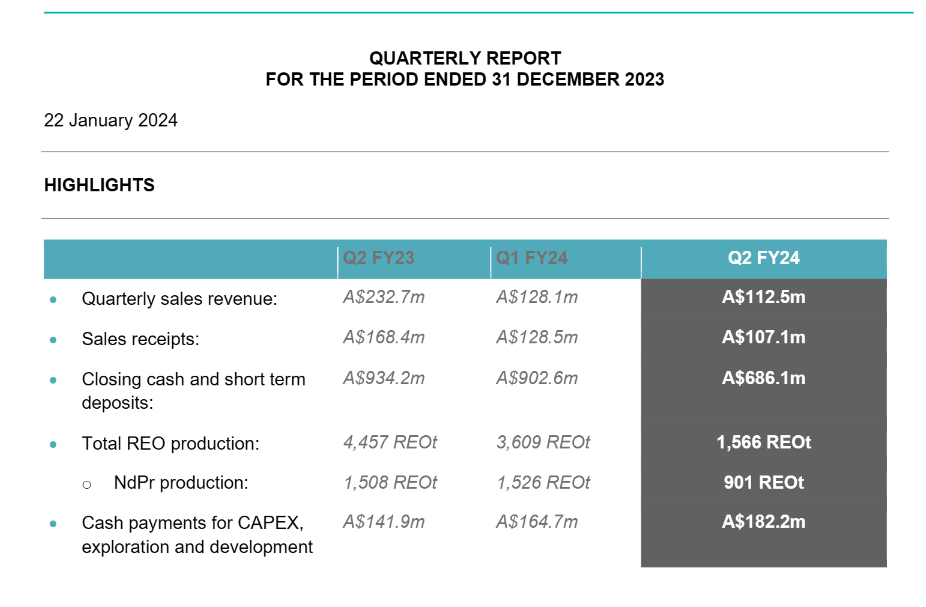

Lynas Rare Earths falls after falling Dec output

Lynas Rare Earths [ASX:LYC] is down by -1.85% today after the company released its December quarter report.

Here are the highlights from the report:

Source: Lynas Rare Earths

The biggest news from the report was the big drop in output for the quarter. The company said a temporary shutdown at its Malaysian site meant that output was down over half from the prior quarter at only 901 REOt.

The miner produced 1,566 tonnes of Rare Earth Oxide (REO), down from 3,609 tonnes in the prior quarter. Sales were also down as a result.

Looking ahead, the company said:

“Production in the March quarter is now expected to be approximately 1500 tonnes and production across the six months to June 2024 is expected to increase slightly from the previous estimate to be in the range of 3200 to 3400 tonnes.”

Morning market update

Good morning. Charlie here

The ASX 200 opened up 0.45% to 7,454.9, as the Tech giants pushed the S&P 500 to a record high for the first time in two years.

In ASX news this morning, Aussie miners have lowered their guidance outputs or reduced output, so expect movement in the mining sector.

South32 has lowered its copper guidance by 3%, while Lynas Rare Earths output dropped over 50% in the December quarter after a temporary shutdown at their Malaysian Project was scheduled for upgrades.

Fortescue Metals announced the shutdown of WA Nickel mine Wyloo due to the collapsing nickel prices from oversupply. The closure is expected to add to the already growing list of job losses from the falling nickel prices.

Meanwhile, Iron ore stabilised below US$130 a tonne after two weeks of falling prices.

Wall Street: Dow +1.05%, Nasdaq +1.70%, S&P 500 1.23%.

Overseas: FTSE flat, STOXX -0.095%, Nikkei +1.40%, SSE -0.47%

The Aussie dollar gained +0.06% to US 65.99 cents.

US 10-year bond yields fell -2 at 4.12%.

Australian 10-year bond yields flat at 4.26%.

Gold down -0.12% to US$2,027.46. Silver fell -0.24% to US$22.56.

Bitcoin fell -0.33% to US$41,558, while Ethereum fell -0.60% to US$2,455.

Oil Brent fell +0.11% to US$78.65, while WTI Crude fell -0.77% to US$73.51.

Iron ore fell +0.2% to US$129.65 a tonne.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988