ASX News LIVE | XJO Falls; Oil Marches Higher; GDP Data Fallout

ASX 200 records worst day in three weeks, BHP trades ex-dividend

The ASX 200 ended 1.2% lower on Thursday, its worst fall in three weeks.

ASX giant BHP dragged the benchmark index lower as it was trading ex-dividend.

But other large stocks also sank:

- Super Retail was down 7.6%

- Air New Zealand was down 7.2%

- Star Entertainment was down 5.7%

- BHP was down 5.2%

- Allkem was down 4.4%

Spotify’s $1 billion podcast bet hasn’t paid off

It’s all about return on investment.

And for Spotify, its splurge on podcasting is yielding paltry returns.

The Wall Street Journal reported that the streaming platform invested over US$1 billion in its podcast empire.

But the empire is full of rags, not riches.

The WSJ reports:

‘Most of its shows aren’t profitable, according to people familiar with the matter, and the company has recently cut staff and programming to slow its losses. The company, which has struggled to report consistent profits, lost €527 million, equivalent to about $565 million, in the six months ending in June, on €6.2 billion in revenue.

‘No one in the business is making much money on podcasts, but Spotify, which has spent far more on the medium than its rivals, has more to lose than most. Spotify’s competitors, including Amazon, Apple and Google, tech behemoths with their own audiostreaming services, have other, more profitable businesses.

‘Podcast revenue in the U.S. is expected to reach $2.3 billion this year, a 25% increase from 2022, according to the Interactive Advertising Bureau, an industry group, and is expected to more than double by 2025. That represents a tiny slice of the $200 billion digital-ad market. Spotify spent its way to the top of an industry that turned out to be less lucrative than it appeared when it began its podcast quest in 2018.’

Philip Lowe: interest rates not the reason Australian house prices are so high

Philip Lowe admitted interest rates influence housing prices, but they are ‘not the reason that Australia has some of the highest cost of housing in the world’.

‘It is certainly the case that the structurally lower nominal interest rates that followed the return of low inflation in the early 1990s contributed to the increase in housing prices. But the reason that Australia has some of the highest housing prices in the world isn’t interest rates, which have been at roughly similar levels across most advanced economies.

‘Rather, it is the outcome of the choices we have made as a society: choices about where we live; how we design our cities, and zone and regulate urban land; how we invest in and design transport systems; and how we tax land and housing investment.

‘In each of these areas, our society and politicians have made choices that lead to high urban land and housing costs. It is by tackling these issues that we can address the high cost of housing in Australia, which I view as a serious economic and social problem.’

Lowe stresses the importance of lifting productivity growth

I’ve talked quite a bit today about falling labour productivity and the related rise in labour unit costs.

Philip Lowe, in his final speech, made it a big focus, too.

Lowe said it is crucial to lift productivity growth.

‘Productivity growth is central to our future prosperity. It means rising living standards, higher real wages, a lift in our collective wealth, a bigger pie to help finance the public services the community values and less inflation pressure. It makes most things easier.’

Lowe then said something profound.

Australia doesn’t lack ideas to improve productivity. It lacks consensus to implement any of them:

‘The problem is not a lack of ideas. Instead, it is in building the consensus within society to implement some of these ideas. This is, fundamentally, a political problem, and it is a major problem. If we can’t build a consensus for changes, the economy will drift and there is a material risk that our living standards will stagnate.’

Now onto those labour unit costs:

‘For inflation to average 2½ per cent, we would expect that, on average, wages increase at the rate of productivity growth plus 2½ per cent. Given that the distribution of national income between wages and profits can and does vary, this relationship is not a hard and fast rule, but it is a reasonable benchmark.’

Let’s try a little napkin maths.

The latest ABS June quarter data dump showed GDP per hour worked fell 3.6% year on year.

So, for inflation to average 2.5%, given productivity growth of -3.6%, wages growth had to be -1.1%.

Last month, ABS’s wage price index showed annual wages growth in the June quarter was 3.6%.

Philip Lowe delivers final speech and reckons with legacy

Outgoing RBA governor Philip Lowe delivered his final speech today, hosted by the Anika Foundation.

Some highlights below.

Inflation will be more volatile in the years ahead:

‘My view is that it will be difficult to return to the earlier world in which inflation tracked in a very narrow range. The increased prevalence of supply shocks, deglobalisation, climate change, the energy transition and shifts in demographics mean either steeper supply curves or more variable supply curves. While this doesn’t mean that the inflation target can’t be achieved on average, it does mean that inflation is likely to be more variable around that target.’

2024 interest guidance was not a commitment but a conditional statement:

‘[The] issue that has defined my term more than any other is the forward guidance about interest rates that was provided during the pandemic. That guidance was widely interpreted as a commitment, rather than a conditional statement, that interest rates would not increase until 2024. As you know, interest rates started being increased in May 2022 and there has been much criticism since, especially by those who borrowed during the pandemic based on our guidance.’

The RBA ‘did too much’ in response to the pandemic:

‘With the benefit of hindsight, my view is that we did do too much. But hindsight is a wonderful thing. None of us can predict the future and we have had to make decisions under great uncertainty and with incomplete information. We got some things right, but we got other things wrong. I can assure you, though, that the staff of the RBA and members of the Reserve Bank Board have been relentless in their pursuit of doing the right thing and supporting the economic prosperity of the people of Australia. And I will leave the RBA after 43 years proud of our contribution to the stability of both our economy and financial system.’

Fiscal policy can lend central banks a helping hand:

‘The current global consensus is that monetary policy is the main cyclical policy instrument and should be assigned the job of managing inflation. This is partly because monetary policy is more nimble and it is not influenced by political considerations. Raising interest rates and tightening policy can make you very unpopular, as I know all too well. This means that it is easier for an independent central bank to do this than it is for politicians.

‘This assignment of responsibility makes sense and it has worked reasonably well. But it doesn’t mean we shouldn’t aspire to something better. Monetary policy is a powerful instrument, but it has its limitations and its effects are felt unevenly across the community.

‘In principle, fiscal policy could provide a stronger helping hand, although this would require some rethinking of the existing policy architecture. In particular, it would require making some fiscal instruments more nimble, strengthening the (semi) automatic stabilisers and giving an independent body limited control over some fiscal instruments. Moving in this direction is not straightforward, but some innovative thinking could help us get to a better place.’

From Glenn Stevens to Philip Lowe to Michele Bullock

Some things are meant to be passed down.

Like a coffee mug emblazoned with the message ‘half full’.

When former Reserve Bank governor Glenn Stevens ceded power to Philip Lowe, he gifted Lowe the coffee mug.

Today, when he finished delivering his final speech before bowing out as governor, Lowe regifted the mug to incoming governor Michele Bullock.

Such is the cycle of life.

BHP drags ASX 200 lower

The #ASX200 is on track for its worst decline in over three weeks. Its currently down 79pts or 1.1%, weighed heavily by $BHP trading ex dividend (-4.4%). All sectors are lower, with miners doing worst.

— CommSec (@CommSec) September 7, 2023

Boss Energy: ‘uranium price is heading only one way’

Uranium miner Boss Energy [ASX:BOE] released its FY23 report today and chairman Wyatt Buck made sure shareholders were upbeat.

Buck wrote that the ‘overwhelming consensus among industry participants and market watchers is that the uranium price is heading only one way’.

He elaborated:

‘These bullish forecasts are underpinned by simple supply and demand forecasts. They stem from the fact that the poor state of the market for over a decade has led to a to prolonged absence of investment in new supply and the drawdown of mobile inventory. Even at the current spot price, which stood at ~US$60 a pound at the time of writing, there is a lack of incentive to invest in new uranium mines.’

If the uranium market is in equilibrium — and the equilibrium price of ~US$60 offers no incentive to invest in new mines — then a shift in aggregate demand will push the price higher.

Or so Buck’s thinking goes.

Although, how come there are ‘so many nuclear power stations being built around the world’ yet the current spot price offers a ‘lack of incentive to invest in new uranium mines’?

Later in the report, management summed up its outlook thus:

‘With cash on hand at 30 June of $89M, a strategic uranium stockpile valued at $118 million , no long-term debt obligations, and a remaining estimated CAPEX spend of A$68.8M including contingency. Boss is well-positioned to transform Honeymoon into production and supply into a rising market as a producer with uncommitted supply.’

$BOE chairman Wyatt Buck wrote the '#uranium price is heading only one way' due to supply dynamics.

'Even at the current spot price … there is a lack of incentive to invest in new uranium mines.' $BOE.AX #ASX pic.twitter.com/3qL0tv2eKX

— Fat Tail Daily (@FatTailDaily) September 7, 2023

By the way, Greg Canavan and I spoke about nuclear energy in our latest episode of What’s Not Priced In.

You can check it out here.

Turns out, nuclear energy has the higher Energy Return on Investment (EROI) of all energy sources. But many countries — including Australia — are cagey about shifting to nuclear.

Boss Energy hits 52-week high

Uranium stock Boss Energy [ASX:BOE], up 40% this month, hit a new 52-week high earlier today.

The stock is now worth about $1.4 billion, gaining 90% this year.

Earlier this week, large uranium miner Cameco downgraded its production guidance at a time when the market for uranium was already tightening.

APA, Alumina, Ansell, Bega Cheese among stocks hitting 52-week lows

Some big names are hitting fresh 52-week lows this week.

- APA Group

- Alumina

- Ansell

- Bega Cheese

- Vulcan Energy

- KMD Brands

- Novonix

- Michael Hill

- Zip

Coolabah Capital’s Christopher Joye: ‘strong unit labour costs challenge RBA’

I’m not the only one fixating on the latest unit labour cost increase.

Coolabah Capital’s Christopher Joye also thinks the rise poses a challenge for our central bank.

‘Nominal unit labour costs increased by about 1½% in Q2 to be 7½% higher than a year ago, which, excluding the distortions caused by COVID-related policies, is the fastest growth since 1990, three years before the RBA adopted its 2-3% inflation target.

‘The RBA no doubt realises the scale of this challenge and will likely be aiming for a cyclical improvement in productivity, where companies cut hours worked, which raises a clear risk of some eventual job losses. ‘

Strong unit labour costs challenge the RBA – our analysis https://t.co/8hvs3dGI9u pic.twitter.com/hmFzrhMrjA

— christopher joye (@cjoye) September 6, 2023

Oil prices climb higher as the fight for our energy future intensifies: Ryan Clarkson-Ledward

Excerpt from Ryan Clarkson-Ledward’s latest piece for Money Morning.

***

Oil prices have just hit a fresh high for 2023.

Brent crude is now above US$90 per barrel, the first time it has reached this milestone since last November.

The driving catalyst is, of course, ongoing production cuts from the Saudis and Russia. OPEC’s stranglehold over the market continues to prove problematic.

That’s the whole point of a cartel, though.

And OPEC is one of, if not the most, pragmatic cartels in human history.

We can lay blame on them all we want, but at the end of the day, they are predictable. That’s why I believe the bigger issue lies beyond OPEC.

What we, as investors, should really be upset about is the fact that our politicians and corporate leaders have let this happen. I’ve spoken at length about the underinvestment and underappreciation of oil in 2023 and why it will come back to bite us.

You can check out my articles here and here if you want a refresher.

But let’s delve into how we can potentially prevent the next energy crisis before it begins…

Conflicting visions

The reality is, we need new oil and gas projects more than ever.

The problem is that funding and support for such projects are at an all-time low.

Just look at the recent mess going on with Fortescue [ASX:FMG]. Three executives, including the CEO and CFO, have walked away from the company without really saying why. All we can infer from off-handed comments from Andrew ‘Twiggy’ Forrest is that all three likely disagreed with his hydrogen vision.

In Forrest’s own words, they had a simple choice:

‘Get on the bus or get off the bus.’

Meaning the execs had to toe the line or find somewhere else to work. And they’ve chosen the latter.

I bring this up because I think it perfectly encapsulates the problem the energy industry has right now. Because as much as hydrogen will have a key role to play in our energy future, it isn’t the be all and end all.

Fossil fuels, love them or hate them, are still going to be vital for quite some time to come. But unless we start pumping money into new projects, we’re going to end up high and dry.

Fortunately, companies like Woodside are still doing their part. The company’s Trion deepwater venture in Mexico just got the green light from the regulator this week.

It brings Woodside one step closer to bringing roughly 478.7 million barrels of oil to the market. A reserve that will steadily come online from 2028 if all goes to plan.

One of the few glimmers of hope for those who see reason in a fossil fuel future.

https://www.moneymorning.com.au/20230907/oil-prices-climb-higher-as-the-fight-for-our-energy-future-intensifies.html

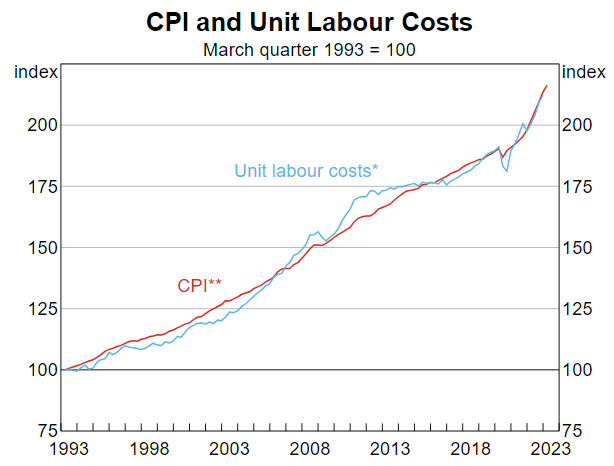

Why the RBA will worry about latest unit labour cost figure

I want to talk more about the latest unit labour cost figures.

In June, Philip Lowe gave an address at Morgan Stanley’s fifth Australia Summit.

A key section of the speech focused on unit labour costs.

Lowe said the RBA pays ‘close attention’ to the rate of growth in unit labour costs — the difference between growth in nominal wages and productivity.

Why?

Because there is a ‘close relationship between inflation and the rate of growth in unit labour costs.’

Here’s the kicker:

‘Over the entire inflation targeting period, the cumulative increase in the CPI has closely matched that in unit labour costs, although there have been periods of divergence.’

Lowe went on:

‘While the causation with inflation runs both ways, ongoing strong growth in unit labour costs would underpin ongoing high inflation outcomes. The best way to achieve a moderation in growth in unit labour costs is through stronger productivity growth, which would also underpin durable increases in real wages and our national wealth and make more resources available to fund the public services that people value.’

Why poor productivity will worry the RBA

In recent monthly statements following the Reserve Bank’s cash rate decision, Philip Lowe insisted that ‘wages growth has picked up over the past year but is still consistent with the inflation target, provided that productivity growth picks up.’

Well productivity growth is not picking up but dropping.

While we worked 6.8% more hours this year than last year, labour productivity fell 3.2% in annual terms.

GDP per hour worked fell 2% in the June quarter and is down 3.6% year on year.

The big thing for me was labour unit costs.

Labour unit costs measure wages growth in relation to productivity. Higher labour unit costs imply wages are rising without a related lift in productivity.

Real unit labour costs rose a substantial 3.2% in the quarter and are up 5.8% for the year!

Why is this a big deal?

A few months ago, Philip Lowe faced a Senate committee and said this:

‘If unit labour cost growth is 3½ to four per cent, then it’s hard to have 2.5 per cent inflation. So that’s the issue that I’m drawing attention to.

‘The best solution to this is a lift in productivity growth. If we’re going to have 2½ per cent inflation, we cannot have unit labour costs persistently growing at 3½ or four per cent. We have to have labour cost growth starting with a ‘2’.’

Current labour cost growth doesn’t start with a 2.

Household saving ratio falls to lowest level since 2008

Australia’s household saving ratio fell for the seventh straight quarter to 3.2%.

That’s the lowest level since 2008’s June quarter.

ABS’s Katherine Keenan said the fall was ‘driven by higher interest payable on dwellings, income tax payable and increased spending by households due to the rising cost of living pressures.’

For instance, households parted with $82.8 billion for mortgage interest payments during the year. The ABS said this was almost double last year’s interest bill.

Australia is in a GDP per capita recession

Australian gross domestic product (GDP) rose 0.4% in the June quarter and by 3.4% over the last 12 months.

That’s the good news.

On to the bad news.

Australia is in a recession, sort of.

For the second straight quarter, Australia’s GDP per capita fell 0.3%. And is down 0.3% year on year!

Population growth is outpacing the growth of our economic output.

On a per person basis, we aren’t doing so well.

And no wonder.

Household spending rose only 0.1% in the quarter, contributing a paltry 0.1% to GDP growth. And the only reason it grew at all was our spending on essential goods and services.

This pair was the main contributor to the modest lift in household spending. Discretionary spending took a dive, falling 0.5% in the June quarter, the third quarterly fall in a row.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988