ASX News LIVE | XJO Slips Again After Bearish Wall St Week; Qantas Signals $200m Higher Costs as Higer Fuel Prices Hit

Market Close

The ASX 200 turned around this morning’s losses to end the day slightly up 0.11% at 7,076.5.

Materials (-0.73%) and Financials (-0.21%) were the only two sectors down by the closing bell, with remarkable recoveries seen in the Information Technology Sector, which gained 1.92%.

Within Tech, Xero gained 2% to $116.97, while WiseTech Global gained 1.5% to $67.85 per share.

Weaker iron ore futures were the main culprit for bringing down the materials sector, as data from China showed the economy struggling to fire on all cylinders.

Iron Ore futures in Singapore dropped 4.1% to US$116.25 pt, down from nearly US$124pt last week.

Fortescue Metals fell 1.3% to $20.54, while Rio Tinto fell 1.2% to $113.18 per share.

Uranium continued its bull run as miners posted another day of strong gains.

Bannerman Energy gained 11.8% to $2.76 per share, while Paladin Energy gained 6.1% to $1.04, and Boss Energy was up 5.1% to $4.73.

$100m in funding for Hydrogen Hub in SA

State and Federal governments have committed $100 million for a hydrogen terminal near Whyalla in SA. The so-called ‘hydrogen hub’ is part of the government’s expectations of ‘large-scale’ global exports of ‘green hydrogen’ before the end of the decade.

‘Because there’s such available land there of course, there’s abundant solar and wind resources, South Australia is primed to become a world-class low-cost hydrogen supplier, and the government has a comprehensive plan to develop a hydrogen industry in the Spencer Gulf,’ Mr Albanese said today.

The government expects private businesses to also join in large-scale investments in the hub, which is expected to produce as much as 1.8 million tonnes of hydrogen by 2030. The location of the hub is also beside the Whyalla steelworks, which has been suggested could benefit from the energy.

‘You also have the potential for essentially green hydrogen, which is hydrogen created through renewable energy, to power the steel production, of green steel there in Whyalla for it to be an export hub as well,’ Mr Albanese suggested.

The funding commitment is part of the larger scale $2 billion Hydrogen Headstart program announced in this year’s federal budget to bring on projects to decarbonise the economy.

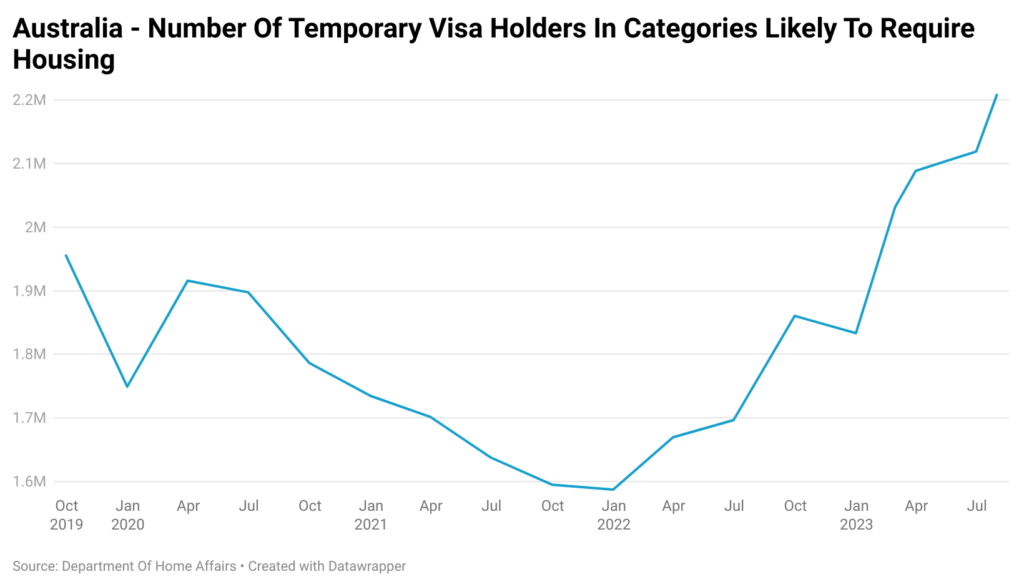

Australia’s rentals rising

Recent large increases in temporary visa holders have now eclipsed its seasonal pre-COVID peak in December.

Info from the ABS has the figures at 454,000 new migrants on a rolling 12-month basis. Prior to the pandemic, the high was 300,000, back in 2009.

Source: Dpt of Home Affairs

Since then, the number of newly arrived immigrants looking for housing has risen by a further 374,000 to an all-time high of slightly over 2.2 million.

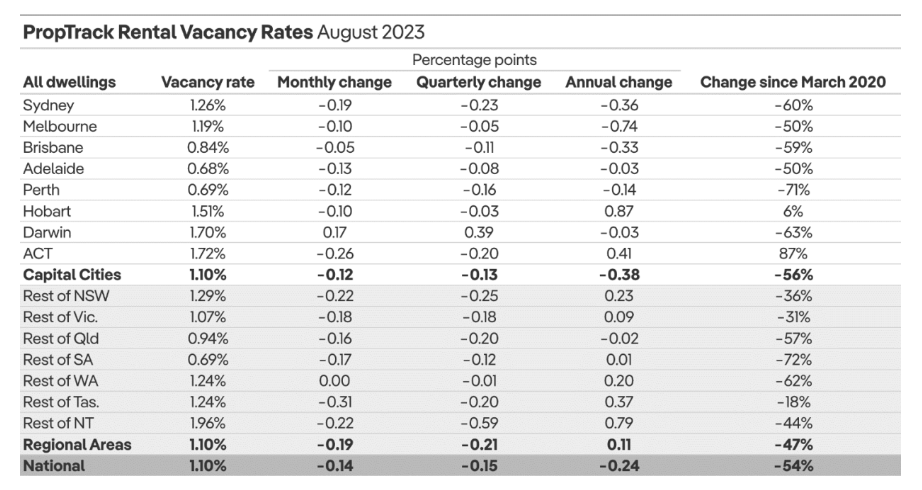

In August, we saw vacancy rates fall and rental prices skyrocket.

Asking rents across the capitals were up 0.2% for the month and 16.1% over the past year.

Source: PropTrack

The issue of immigration and housing supply has become a similar political issue across Britain and Canada in recent years, with Canada eventually bringing in foreign buyer restrictions in an attempt to ease the record prices there.

It seems for now the rental crisis is set to continue within Australia for some time.

Market update

ASX 200 slightly down around early afternoon after recovering somewhat from this morning’s losses.

Falling iron ore prices hit miners, while the big four also dragged the ASX down, with the Materials Sector down -1.0% and Financials down -0.49%.

The ASX200 is down 0.19%, trading at 7,055.2.

The markets maintain a slightly bearish outlook as we await the all-important CPI data out on Wednesday.

With rising fuel costs, many are concerned inflation could start creeping back through headline inflation.

In company news, Qantas [ASX:QAN] slips 1.6% as it highlights rising costs. Allkem [ASX:AKE] also fell 2.83% after flagging higher estimated costs in its lithium project.

Synlait [ASX:SM1] Posts $4.3m loss after ‘extremely challenging year’

NZ dairy producer has had a tough year and isn’t beating around the bush about it.

In its own telling, the dairy giant has had an ‘extremely challenging financial year, with a poor financial result delivered.’

The company pulled in total revenue of $1.6 billion, which was down 3% from last year as the average milk price for last financial year was down 11% at $8.49kgMS.

The company blamed lower margins as significant ERP implementation costs and inflationary pressures hurt the bottom line.

The poor results come as the background tiff with long-time partner A2 spilled into the public view as A2 pulled its exclusivity deal with Synlait after what it described as production shortfalls.

Despite the tough news today, the company’s share price is up 2.56% this morning as investors hold hopes on the completed strategy refresh.

Sneak peak stock picks

Here’s the latest from Editorial Director Greg Canavan, who is giving readers a sneak peek behind the curtain to what paid subscribers get when they sign up for Fat Tail investment advisory.

If you are looking for some smart positions as markets continue to look shakey, then look no further, as Greg brings his years of experience to the table.

Qantas signals $200m hit from fuel costs

Qantas flagged today that the recent fuel price spike will likely add another $200 million to the airline’s first-half fuel bill.

The airline said fuel prices have risen 30% since May as Oil prices continue to climb from oil production cuts from Russia and Saudi Arabia.

Amidst the recent scandals, Qantas also signalled a further $80 million will be spent on customer improvements as the company fights to regain its public image after a host of scandals led to the early retirement of ex-CEO Alan Joyce.

If these production cuts remain for the foreseeable future, then the higher fuel costs are likely to add another $2.8 billion to Qantas’s fuel bill in the first six months of 2024.

The new CEO, Vanessa Hudson, has also signalled a large spend to upgrade the airline’s aging fleet as well as the potential of a $250 million fine related to allegations it sold thousands of ‘ghost flight’ tickets to cancelled flights.

All of this spells huge costs for the airline in the future.

Crude Oil resumes its climb

Oil gave a brief respite last week, with WTI crude down 1.0% after three weeks of straight gains.

Now it seems oil prices are back in a bullish pattern as hedge funds piled into Energy as a defensive position as expectations of tightening supplies are continuing.

West Texas Intermediate futures and Crude Brent futures are up around 0.4%.

WTI is again trading above US$90 per barrel, while Brent hovers just short of US$ 94 per barrel.

JPMorgan & Chase laid predictions for an ‘oil supercycle‘ and prices above $100.

Oil has risen nearly 30% since the end of June as curbs from OPEC+ have been continued until December, in a move that has put inflationary pressure back on markets.

Russia last week also announced a temporary ban on diesel and gasoline exports while spiking European fuel prices, while low inventories have caused bidding wars between importers.

ASX Falls

ASX 200 is down 0.55% this morning at 7,030.1 as a broad risk-off continues across markets.

- $AUD flat +0.08% at 64.42 US cents

- ASX futures down -0.20% to 7,071.5

- S&P 500 down -0.23%

- NASDAQ flat -0.092%

- DOW down -0.31%

- FTSE flat +0.069%

- STOXX down -0.21%

- SSE up +1.55%

- Bitcoin down -1.64% to $US 26,134.91

- Spot gold flat -0.02% to $US 1,924.87

- Iron ore down -0.30% to $US 121.33

- Brent Crude down -0.42% to $US 93.66pb

All figures shown are from 10:50am AEST

Good Morning

Happy Monday all,

The Australian markets begin this week in a bearish phase as the ASX reflects growing concerns from the US as last week as the S&P500 had its worst week since March, falling 2.9%.

Big names that saw losses in the S&P500 were Tesla (-10.8), Amazon (-8.0%), and Alphabet (-5.2%).

The recession concerns were brought about after the Fed kept interest rates on hold last week but changed its outlook on interest rates for the year ahead. In the announcement, it shifted its end of CY24 interest rate expectations from 4.6% to 5.1%.

This ‘higher for longer’ has soured sentiments despite the reasons given by J. Powell and the Fed, being that the economy was still a little hot for their goals of bringing inflation under control.

As a response, long-rate worries sparked the largest weekly outflow of stocks within global equity funds since December.

The CNN Fear and Greed index also shifted from neutral to fear, signalling concerns within the market as higher fuel costs bring concerns over rising food costs and CPI inflation pressures.

The US also fell back into its almost ritualistic return to government shutdown brinkmanship as the two political parties fail to see eye to eye on the growing problem of US government debt, which has reached US$33 trillion.

That’s US$98,950 for each person in America.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988