ASX News LIVE | XJO Opens Lower as Rising Bond Yields Spook Markets

Novonix touts AI-adjacent development

When your stock is down 70% since October 2022 and you need a positive catalyst, what better catalyst is there right now than AI?

Struggling battery materials and technology firm Novonix [ASX:NVX] today released an announcement titled ‘Novonix receives funding for cathode & AI development work’.

Do cathodes and AI usually go together?

Not really. The funding will support two distinct research projects — one on cathodes, another on AI.

Novonix said its Battery Technology Solutions division is receiving ‘up to CAD$3 million in research and development funding and advisory services’ from the National Research Council of Canada’s Industrial Research Assistance Program.

AI is the eye-grabber here. So what AI research will NVX’s division conduct? Novonix elaborated:

‘Demand for lithium-ion batteries is rapidly growing and NOVONIX is working to support the global electrification trend by exploring critical technologies and materials that are required for long-life, high-performance battery applications. By leveraging SandboxAQ’s expertise in artificial intelligence with quantum analysis, NOVONIX is developing a data and analytics product offering that pairs effectively with the Company’s existing battery testing equipment and services offering.

‘NOVONIX’s planned product development is focused on implementing advanced analysis techniques, anomaly detection tools, and using machine-learning to create accurate lifetime prediction using NOVONIX’s UHPC testing equipment and data.’

Novonix touts AI-adjacent development

When your stock is down 70% since October 2022 and you need a positive catalyst, what better catalyst is there right now than AI?

Struggling battery materials and technology firm Novonix [ASX:NVX] today released an announcement titled ‘Novonix receives funding for cathode & AI development work’.

Do cathodes and AI usually go together?

Not really. The funding will support two distinct research projects — one on cathodes, another on AI.

Novonix said its Battery Technology Solutions division is receiving ‘up to CAD$3 million in research and development funding and advisory services’ from the National Research Council of Canada’s Industrial Research Assistance Program.

AI is the eye-grabber here. So what AI research will NVX’s division conduct? Novonix elaborated:

‘Demand for lithium-ion batteries is rapidly growing and NOVONIX is working to support the global electrification trend by exploring critical technologies and materials that are required for long-life, high-performance battery applications. By leveraging SandboxAQ’s expertise in artificial intelligence with quantum analysis, NOVONIX is developing a data and analytics product offering that pairs effectively with the Company’s existing battery testing equipment and services offering.

‘NOVONIX’s planned product development is focused on implementing advanced analysis techniques, anomaly detection tools, and using machine-learning to create accurate lifetime prediction using NOVONIX’s UHPC testing equipment and data.’

Is the market wrong about Chalice Mining?

Chalice Mining is down 55% this month and hit a new 52-week low.

The sell-off was brought about by a badly received scoping study that used commodity price assumptions too optimistic for the market’s liking.

But our resources expert and geologist James Cooper thinks the market has judged the scoping study too harshly and has too short-sighted a view. The following is an extract from his latest piece for Fat Tail Commodities.

***

Ask a geologist to name the number one greenfield discovery in Australia and there’s a good chance they’ll give you the name of Chalice Mining’s [ASX:CHN] Gonneville deposit.

The ore body was discovered by a small team of dedicated geologists in 2020.

It’s a high grade nickel-copper-platinum critical metal treasure chest located just 70 kilometres north-east of the Western Australian capital, Perth.

Yet, despite harbouring key ingredients for the green energy transition, Chalice’s share price has plummeted in recent months. The company has fallen around 70% since April 2023.

It begs the question…what will it take to get global capital back into the junior mining sector?

After all, Chalice’s Gonneville deposit is a poster child for the critical metal boom.

Without projects like this, the energy transition can’t happen.

Global capital continues to ignore the critical role of the junior mining sector.

Despite commodity prices remaining high, and mining giants continuing to post strong earnings results, there’s very little appetite for the small end of town.

That is, the sector that leads discovery and development.

Ultimately, these are the companies feeding future commodity supply chains.

But with the deep sell-off continuing, investor expectations have started to divorce reality.

Just take Chalice’s latest scoping study…

The company announced a two-year payback on a mine costing between $1.6 billion and $2.3 billion.

And with maiden production slated for the late 2020s…investors won’t have to wait decades to see the company turn into a profit generating machine.

Despite that, one of Australia’s most important critical metal projects now languishes in the dust and is still looking for a floor in its share price…

![Chalice Mining’s [ASX:CHN] Gonneville deposit](https://commodities.fattail.com.au/wp-content/uploads/2023/09/COM20230927_1_580.jpg) |

| Source: ProRealTime |

This shows you the gaping disconnect between investor expectations and what developers can deliver.

But without precious capital reaching these projects…future supply hangs in the balance.

Established producers, while generating income, are shrinking their asset base through mining.

Producers must replace depleting reserves through discovery or acquisition to maintain output.

Given big miners lack of interest in exploration over the last decade, acquisition remains the only option to replace declining reserves.

However, buy-outs do nothing to alleviate global supply pressures.

A deep disconnect remains between today’s income producing giants and those companies exploring for and developing the next generation of deposits.

So why does that matter to you?

Well, supply shocks come quickly in this game and so will the repricing of junior mining stocks.

It’s why investors waiting for a bottom in this market are likely to miss out.

We had a brief glimpse of that in the wake of Russia’s invasion of Ukraine.

Junior mining stocks surged into double and triple digit gains in a matter of days as the global economy panicked over future supplies of commodities.

Just look at the nickel explorer, Galileo Mining [ASX:GAL]…its share price jumped 875% in three weeks.

While GAL was a standout performer, junior mining stocks surged across the board in early 2022.

With supply chains remaining tight and long-term demand fundamentals strengthening, investors should consider maintaining at least some exposure to this sector.

In other words, do what the big miners are doing…

https://commodities.fattail.com.au/chalice-miningwhy-this-sell-off-matters-for-future-supply/2023/09/27/

Is the market wrong about Chalice Mining?

Chalice Mining is down 55% this month and hit a new 52-week low.

The sell-off was brought about by a badly received scoping study that used commodity price assumptions too optimistic for the market’s liking.

But our resources expert and geologist James Cooper thinks the market has judged the scoping study too harshly and has too short-sighted a view. The following is an extract from his latest piece for Fat Tail Commodities.

***

Ask a geologist to name the number one greenfield discovery in Australia and there’s a good chance they’ll give you the name of Chalice Mining’s [ASX:CHN] Gonneville deposit.

The ore body was discovered by a small team of dedicated geologists in 2020.

It’s a high grade nickel-copper-platinum critical metal treasure chest located just 70 kilometres north-east of the Western Australian capital, Perth.

Yet, despite harbouring key ingredients for the green energy transition, Chalice’s share price has plummeted in recent months. The company has fallen around 70% since April 2023.

It begs the question…what will it take to get global capital back into the junior mining sector?

After all, Chalice’s Gonneville deposit is a poster child for the critical metal boom.

Without projects like this, the energy transition can’t happen.

Global capital continues to ignore the critical role of the junior mining sector.

Despite commodity prices remaining high, and mining giants continuing to post strong earnings results, there’s very little appetite for the small end of town.

That is, the sector that leads discovery and development.

Ultimately, these are the companies feeding future commodity supply chains.

But with the deep sell-off continuing, investor expectations have started to divorce reality.

Just take Chalice’s latest scoping study…

The company announced a two-year payback on a mine costing between $1.6 billion and $2.3 billion.

And with maiden production slated for the late 2020s…investors won’t have to wait decades to see the company turn into a profit generating machine.

Despite that, one of Australia’s most important critical metal projects now languishes in the dust and is still looking for a floor in its share price…

| |

| Source: ProRealTime |

This shows you the gaping disconnect between investor expectations and what developers can deliver.

But without precious capital reaching these projects…future supply hangs in the balance.

Established producers, while generating income, are shrinking their asset base through mining.

Producers must replace depleting reserves through discovery or acquisition to maintain output.

Given big miners lack of interest in exploration over the last decade, acquisition remains the only option to replace declining reserves.

However, buy-outs do nothing to alleviate global supply pressures.

A deep disconnect remains between today’s income producing giants and those companies exploring for and developing the next generation of deposits.

So why does that matter to you?

Well, supply shocks come quickly in this game and so will the repricing of junior mining stocks.

It’s why investors waiting for a bottom in this market are likely to miss out.

We had a brief glimpse of that in the wake of Russia’s invasion of Ukraine.

Junior mining stocks surged into double and triple digit gains in a matter of days as the global economy panicked over future supplies of commodities.

Just look at the nickel explorer, Galileo Mining [ASX:GAL]…its share price jumped 875% in three weeks.

While GAL was a standout performer, junior mining stocks surged across the board in early 2022.

With supply chains remaining tight and long-term demand fundamentals strengthening, investors should consider maintaining at least some exposure to this sector.

In other words, do what the big miners are doing…

https://commodities.fattail.com.au/chalice-miningwhy-this-sell-off-matters-for-future-supply/2023/09/27/

Commonwealth Bank: headline inflation rise a ‘temporary hump’

Commonwealth Bank economist Stephen Wu said the rise in headline inflation registered by August’s CPI indicator was a ‘temporary hump’. Wu said the uptick was entirely expected due to the recent spike in the price of automotive fuel.

Wu elaborated:

‘We view the uptick in inflation in August as a temporary hump in the downward trend in train since December last year.

‘We think the RBA will be inclined to see it that way too when it meets next Tuesday for the October rate decision. We don’t anticipate the August CPI will alter their view the current cash rate of 4.1 per cent is restrictive enough to pull inflation back inside the target band.’

Commonwealth Bank: headline inflation rise a ‘temporary hump’

Commonwealth Bank economist Stephen Wu said the rise in headline inflation registered by August’s CPI indicator was a ‘temporary hump’. Wu said the uptick was entirely expected due to the recent spike in the price of automotive fuel.

Wu elaborated:

‘We view the uptick in inflation in August as a temporary hump in the downward trend in train since December last year.

‘We think the RBA will be inclined to see it that way too when it meets next Tuesday for the October rate decision. We don’t anticipate the August CPI will alter their view the current cash rate of 4.1 per cent is restrictive enough to pull inflation back inside the target band.’

Brainchip’s share price collapse

Brainchip was once one of the hottest stocks among retail investors.

Now, it is hitting fresh 52-week lows as excitement and optimism curdle to disappointment and jadedness.

In the last 12 months, Brainchip is down 80%. Since its all-time high in January 2022, the stock is down 90%.

ABS: COVID-19 the first infectious disease to be top 5 cause of death since 1970

COVID-19 is the first infectious disease to be in the top five causes of death in Australia since 1970.

That’s a pretty wild statistic!

In fact, COVID-19 was the third leading cause of death in 2022, accounting for one in twenty deaths, according to the latest figures from the ABS.

In 1970, influenza and pneumonia were the fifth leading cause of death.

ABS’s Lauren Moran, head of mortality statistics, said:

‘The top five causes of death in 2022 were ischaemic heart disease, dementia (including Alzheimer’s disease), COVID-19, cerebrovascular diseases (strokes) and lung cancer, which when combined, accounted for more than a third of all deaths.’

ABS: COVID-19 the first infectious disease to be top 5 cause of death since 1970

COVID-19 is the first infectious disease to be in the top five causes of death in Australia since 1970.

That’s a pretty wild statistic!

In fact, COVID-19 was the third leading cause of death in 2022, accounting for one in twenty deaths, according to the latest figures from the ABS.

In 1970, influenza and pneumonia were the fifth leading cause of death.

ABS’s Lauren Moran, head of mortality statistics, said:

‘The top five causes of death in 2022 were ischaemic heart disease, dementia (including Alzheimer’s disease), COVID-19, cerebrovascular diseases (strokes) and lung cancer, which when combined, accounted for more than a third of all deaths.’

Inflation for discretionary categories is weak or cooling

Inflation in discretionary categories is either weak or cooling. #auspol #ASX pic.twitter.com/nv8KryRPRB

— Fat Tail Daily (@FatTailDaily) September 27, 2023

Inflation for discretionary categories is weak or cooling

Inflation in discretionary categories is either weak or cooling. #auspol #ASX pic.twitter.com/nv8KryRPRB

— Fat Tail Daily (@FatTailDaily) September 27, 2023

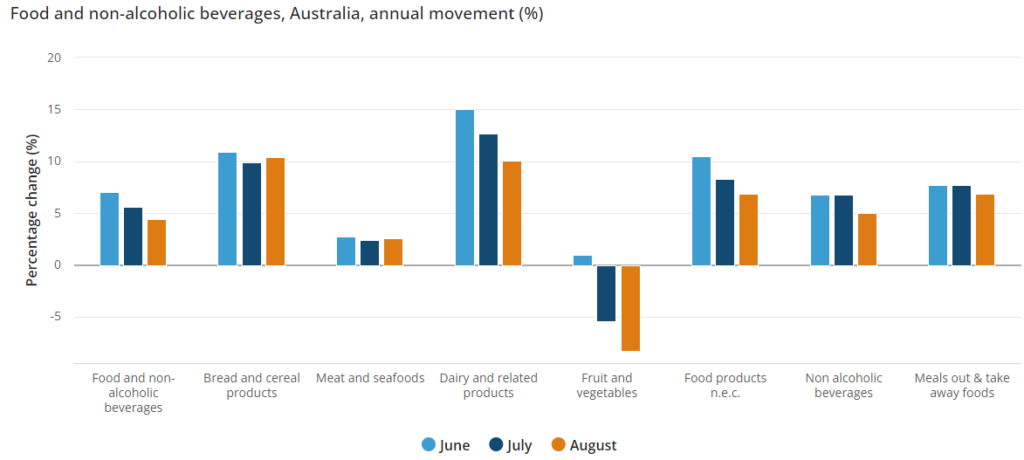

Good time to change your diet, according to latest CPI figures

It’s a good time to change your dietary habits.

At least according to the latest monthly CPI figures from the ABS.

Fruit and vegetable prices are 8.3% lower compared to 12 months ago. The ABS attributed this to improved growing conditions.

Good time to change your diet, according to latest CPI figures

It’s a good time to change your dietary habits.

At least according to the latest monthly CPI figures from the ABS.

Fruit and vegetable prices are 8.3% lower compared to 12 months ago. The ABS attributed this to improved growing conditions.

Aussie monthly inflation in line with expectations

Australia’s monthly CPI indicator for August rose in line with expectations.

The headline CPI indicator rose 5.2% in the 12 months to August, just as consensus estimates forecast. Finally, a win for the forecasters!

August’s annual increase of 5.2% is up from July’s 4.9%.

However, when you exclude volatile items, the monthly CPI indicator fell from 5.8% in July to 5.5% in August on an annual basis. A good sign.

We’ve all noticed rising fuel prices lately.

The ABS noted automotive fuel prices were up 13.9% on last year and rose 9.1% on a monthly basis in August.

Monthly CPI indicator for August in line with expectations, with the excluding volatiles measure retreating from July pic.twitter.com/MP2EsIORrw

— Alex Joiner 🇦🇺 (@IFM_Economist) September 27, 2023

Aussie monthly inflation in line with expectations

Australia’s monthly CPI indicator for August rose in line with expectations.

The headline CPI indicator rose 5.2% in the 12 months to August, just as consensus estimates forecast. Finally, a win for the forecasters!

August’s annual increase of 5.2% is up from July’s 4.9%.

However, when you exclude volatile items, the monthly CPI indicator fell from 5.8% in July to 5.5% in August on an annual basis. A good sign.

We’ve all noticed rising fuel prices lately.

The ABS noted automotive fuel prices were up 13.9% on last year and rose 9.1% on a monthly basis in August.

Monthly CPI indicator for August in line with expectations, with the excluding volatiles measure retreating from July pic.twitter.com/MP2EsIORrw

— Alex Joiner 🇦🇺 (@IFM_Economist) September 27, 2023

The S&P 493 is basically flat in 2023

The Magnificent Seven largely account for most of the S&P 500’s gains.

Apollo Management’s Torsten Slok recently noted that, ex-Magnificent Seven, the S&P 500 has basically gone nowhere this year.

Slok then concluded:

‘If you buy the S&P500 today, you are basically buying a handful of companies that make up 34% of the index and have an average P/E ratio around 50.‘

Food for thought?

The S&P 493 is basically flat in 2023

The Magnificent Seven largely account for most of the S&P 500’s gains.

Apollo Management’s Torsten Slok recently noted that, ex-Magnificent Seven, the S&P 500 has basically gone nowhere this year.

Slok then concluded:

‘If you buy the S&P500 today, you are basically buying a handful of companies that make up 34% of the index and have an average P/E ratio around 50.‘

Food for thought?

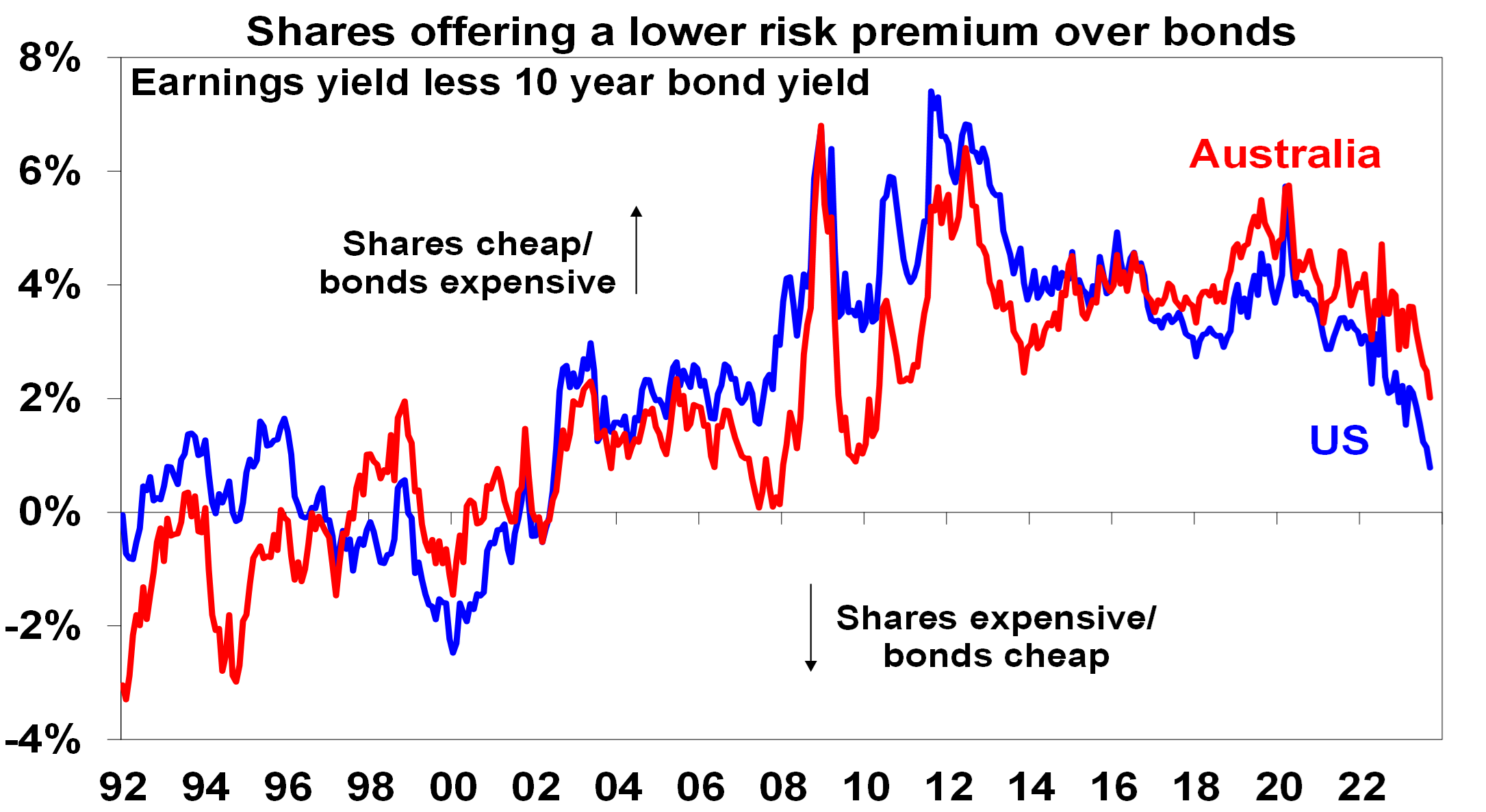

Aussie and US shares offering a lower risk premium over bonds

With bond yields rising and P/E ratios for stocks remaining high, the equity risk premium is shrinking to historically low levels.

A slim equity risk premium implies stocks are expensive relative to safe assets like bonds.

A tiny equity risk premium means you are getting almost no extra compensation for investing in equities, which are riskier than bonds.

As AMP’s chief economist Shane Oliver said in a recent note:

‘PE ratios for shares point to a medium-term return potential of around 10% for Australian shares but just 5% for US shares (see the red lines on the PE charts earlier). Allowing for the rise in bond yields – by subtracting 10-year bond yields from the earnings yields (using forward earnings) – shows US and Australian shares now offer a reduced return premium over bonds of around 0.8% in the US and 2% in Australia.

‘For the US this is the lowest risk premium over bonds since after the tech wreck whereas current uncertainties (around interest rates, recession risk & geopolitics) suggest the risk premium should ideally be higher. Fortunately, that for Australian shares is more attractive. But ideally bond yields need to fall to improve the prospects for shares. If we are right and inflation continues to fall over the year ahead, then this should allow lower bond yields and provide some support to shares. But in the near term the risk of a further correction in share markets led out of the US remains high reflecting the deterioration in US share valuations particularly for tech stocks which are very sensitive to bond yields.’

Aussie and US shares offering a lower risk premium over bonds

With bond yields rising and P/E ratios for stocks remaining high, the equity risk premium is shrinking to historically low levels.

A slim equity risk premium implies stocks are expensive relative to safe assets like bonds.

A tiny equity risk premium means you are getting almost no extra compensation for investing in equities, which are riskier than bonds.

As AMP’s chief economist Shane Oliver said in a recent note:

‘PE ratios for shares point to a medium-term return potential of around 10% for Australian shares but just 5% for US shares (see the red lines on the PE charts earlier). Allowing for the rise in bond yields – by subtracting 10-year bond yields from the earnings yields (using forward earnings) – shows US and Australian shares now offer a reduced return premium over bonds of around 0.8% in the US and 2% in Australia.

‘For the US this is the lowest risk premium over bonds since after the tech wreck whereas current uncertainties (around interest rates, recession risk & geopolitics) suggest the risk premium should ideally be higher. Fortunately, that for Australian shares is more attractive. But ideally bond yields need to fall to improve the prospects for shares. If we are right and inflation continues to fall over the year ahead, then this should allow lower bond yields and provide some support to shares. But in the near term the risk of a further correction in share markets led out of the US remains high reflecting the deterioration in US share valuations particularly for tech stocks which are very sensitive to bond yields.’

Star hits all-time low

Star’s discounted raise has sent it to a new all-time low. Not a 52-week low, but an all-time low.

The stock is down 82% since its public listing.

That’s a colossal destruction of value.

$SGR hits all-time low after discounted capital raise. $SGR.AX is embarking on a big refinancing and equity raising to strengthen balance sheet after stating 'existing debt structure is no longer fit for purpose'. #ASX $XJO pic.twitter.com/EYKSEYCKjo

— Fat Tail Daily (@FatTailDaily) September 27, 2023

Star hits all-time low

Star’s discounted raise has sent it to a new all-time low. Not a 52-week low, but an all-time low.

The stock is down 82% since its public listing.

That’s a colossal destruction of value.

$SGR hits all-time low after discounted capital raise. $SGR.AX is embarking on a big refinancing and equity raising to strengthen balance sheet after stating 'existing debt structure is no longer fit for purpose'. #ASX $XJO pic.twitter.com/EYKSEYCKjo

— Fat Tail Daily (@FatTailDaily) September 27, 2023

Star Entertainment falls 14% after capital raise

Star Entertainment is currently down 14% after raising $565 million at 60 cents a share.

Star last closed at 75 cents a share.

The discounted raise is why the stock is falling today.

Star is ‘undertaking a broader refinancing process to improve its funding arrangements and capital structure’.

Apart from the capital raise, Star also secured $450 million in new debt facilities from Barclays and Westpac.

These mammoth initiatives will strengthen the balance sheet, according to Star.

The firm expects ‘all existing debt to be repaid and cancelled’, with ‘no debt maturities until 2H28’.

In no major surprise, dividends will be suspended until the adjusted net leverage ratio is below 1.5x, the AUSTRAC civil processing is resolved, and the QWB debt refinancing is complete.

Yet another shot

Yet another shot.

But also, an interesting point from David Scutt.

The irony is the greater the belief rates will be higher for longer, the quicker rates will be cut.

— David Scutt (@Scutty) September 26, 2023

Shot shot shot (push-up push-up push-up)

New drinking game.

Take a shot every time you read or hear about 'higher for longer' interest rates.

For the abstemious, ten push-ups. pic.twitter.com/NVzbBRi78b

— Fat Tail Daily (@FatTailDaily) September 27, 2023

New drinking game for investors

Good morning.

Here’s a quick rundown of market news — an espresso shot of news.

Both the Nasdaq and the S&P 500 fell sharply overnight as investor mood sours.

Since hitting their 2023 highs in July, both indices are down over 7%.

Coincidentally, market sentiment — according to CNN’s Fear and Greed Index — was at Extreme Greed in July.

It has now fallen all the way to Fear and is a few points away from Extreme Fear reading. It’s the lowest reading since March 2023.

That’s partly to do with the a recent rise in bond yields.

US 10-year bond yields lifted to 4.54% overnight, a 16 year high.

Yields are rising on market bets of central banks keeping interest rates high for a while yet.

Or, as the popular mantra has it — — higher for longer.

Here’s a new drinking game to poison your liver. Take a shot every time you hear or read about ‘higher for longer’ interest rates. For the abstemious, do ten push ups.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988