ASX News LIVE | XJO Flat; Woolworths, Domino’s, WiseTech, Santos Report

The race of the decade is building gigafactories: Selva Freigedo

It’s been almost 10 years since Tesla announced it was building its first Gigafactory.

These massive factories produce lithium-ion batteries, and Tesla wanted to start manufacturing its own batteries to put them in their electric vehicles (EVs).

You see, when it comes to EVs, the battery is the most crucial part…and the most expensive.

So, the idea was that by bringing manufacturing in-house and using economies of scale, Tesla would be able to cut costs, hence reducing the price of their Teslas.

The company constructed its first Gigafactory in Nevada and has continued to build.

It now has factories in California, Texas, New York, Berlin, and Shanghai, and it is looking to build a seventh in Mexico.

The plan is to continue to expand to hit their EV manufacturing goals.

As Elon Musk said in a meeting last year:

‘Ultimately, we will end up building, I don’t know, probably at least 10 or 12 Gigafactories.’

Tesla may have been the first, but more and more are now following its steps…

As EV sales grow, more automakers and battery makers are looking at building gigafactories to secure their supply chains and drive down costs.

To give you an idea, just three years ago, there were 115 Gigafactories in the pipeline scheduled to be in operation by 2030. That number has now ballooned to over 400, according to Benchmark Minerals.

China is the leader when it comes to building gigafactories. After all, China is the largest battery and EV manufacturer in the world.

But both the US and Europe are racing to catch up.

As Bill Russo, former chief of Chrysler in China said:

‘China’s problem with internal combustion engines was they were forever playing the game of catch-up. Now, the US has to play the game of catch-up with EVs.’

And we’re seeing a lot of investment flowing into creating these EV supply chains.

For instance, last year the US launched the Inflation Reduction Act. One of the main objectives was to bring in more cleantech manufacturing into the US and expedite EV uptake by offering tax credits to consumers.

But for electric vehicles to qualify for these credits, there are some caveats.

https://commodities.fattail.com.au/the-race-of-the-decade/2023/08/23/

The race of the decade is building gigafactories: Selva Freigedo

It’s been almost 10 years since Tesla announced it was building its first Gigafactory.

These massive factories produce lithium-ion batteries, and Tesla wanted to start manufacturing its own batteries to put them in their electric vehicles (EVs).

You see, when it comes to EVs, the battery is the most crucial part…and the most expensive.

So, the idea was that by bringing manufacturing in-house and using economies of scale, Tesla would be able to cut costs, hence reducing the price of their Teslas.

The company constructed its first Gigafactory in Nevada and has continued to build.

It now has factories in California, Texas, New York, Berlin, and Shanghai, and it is looking to build a seventh in Mexico.

The plan is to continue to expand to hit their EV manufacturing goals.

As Elon Musk said in a meeting last year:

‘Ultimately, we will end up building, I don’t know, probably at least 10 or 12 Gigafactories.’

Tesla may have been the first, but more and more are now following its steps…

As EV sales grow, more automakers and battery makers are looking at building gigafactories to secure their supply chains and drive down costs.

To give you an idea, just three years ago, there were 115 Gigafactories in the pipeline scheduled to be in operation by 2030. That number has now ballooned to over 400, according to Benchmark Minerals.

China is the leader when it comes to building gigafactories. After all, China is the largest battery and EV manufacturer in the world.

But both the US and Europe are racing to catch up.

As Bill Russo, former chief of Chrysler in China said:

‘China’s problem with internal combustion engines was they were forever playing the game of catch-up. Now, the US has to play the game of catch-up with EVs.’

And we’re seeing a lot of investment flowing into creating these EV supply chains.

For instance, last year the US launched the Inflation Reduction Act. One of the main objectives was to bring in more cleantech manufacturing into the US and expedite EV uptake by offering tax credits to consumers.

But for electric vehicles to qualify for these credits, there are some caveats.

https://commodities.fattail.com.au/the-race-of-the-decade/2023/08/23/

Is gold really set for a bull market?

Goehring & Rozencwajg released its latest market dispatch, avidly read by investors in the resources sector.

The firm believes gold is set for a bull market.

Here are some excerpts:

‘Those with long memories might remember how gold became the “must-own” asset of the 1970s. We believe the same thing is happening today. Gold demand will come from speculators seeking a short-term profit and generalist investors seeking protection from financial turmoil and mounting inflationary pressures. Gold and silver were radically undervalued in 1971. Over the next decade, they were the best-performing asset class. Between 1970 and the peak in January 1980, gold and silver surged 2,000% and 2,800%, respectively. After peaking in 1980, gold spent the next 20 years drifting lower. By 1999, it had become as cheap as ever on many metrics. Between 1999 and today, gold advanced more than eight-fold, significantly outperforming stocks and bonds. Despite its strong appreciation, we believe gold remains exceptionally cheap based on our framework. In the following essay, we will describe our valuation techniques and show that gold still has a considerable upside, irrespective of what occurs in global financial markets.’

‘We are not gold bugs. Over the long term, gold protects monetary debasement; however, unlike equities, gold will provide little real return. If an investor can identify periods when gold becomes extremely undervalued, it can offer exceptional excess returns, often uncorrelated with other financial assets. The key is figuring out when gold is undervalued and overvalued.’

Is gold really set for a bull market?

Goehring & Rozencwajg released its latest market dispatch, avidly read by investors in the resources sector.

The firm believes gold is set for a bull market.

Here are some excerpts:

‘Those with long memories might remember how gold became the “must-own” asset of the 1970s. We believe the same thing is happening today. Gold demand will come from speculators seeking a short-term profit and generalist investors seeking protection from financial turmoil and mounting inflationary pressures. Gold and silver were radically undervalued in 1971. Over the next decade, they were the best-performing asset class. Between 1970 and the peak in January 1980, gold and silver surged 2,000% and 2,800%, respectively. After peaking in 1980, gold spent the next 20 years drifting lower. By 1999, it had become as cheap as ever on many metrics. Between 1999 and today, gold advanced more than eight-fold, significantly outperforming stocks and bonds. Despite its strong appreciation, we believe gold remains exceptionally cheap based on our framework. In the following essay, we will describe our valuation techniques and show that gold still has a considerable upside, irrespective of what occurs in global financial markets.’

‘We are not gold bugs. Over the long term, gold protects monetary debasement; however, unlike equities, gold will provide little real return. If an investor can identify periods when gold becomes extremely undervalued, it can offer exceptional excess returns, often uncorrelated with other financial assets. The key is figuring out when gold is undervalued and overvalued.’

Jaws of Death remain open

The Jaws of Death we’ve spoken about in recent weeks remain open.

Jaws, Wall Street style: Look at the difference between current stock valuations and a standard discounted cash-flow model (which assumes 6% long-term EPS growth and a 4% ERP) on one side, and what is suggested by real rates and the Fed on the other. That spread is a beast. pic.twitter.com/RpxxupnBsd

— Jurrien Timmer (@TimmerFidelity) August 22, 2023

Jaws of Death remain open

The Jaws of Death we’ve spoken about in recent weeks remain open.

Jaws, Wall Street style: Look at the difference between current stock valuations and a standard discounted cash-flow model (which assumes 6% long-term EPS growth and a 4% ERP) on one side, and what is suggested by real rates and the Fed on the other. That spread is a beast. pic.twitter.com/RpxxupnBsd

— Jurrien Timmer (@TimmerFidelity) August 22, 2023

China’s abandoned, obsolete EVs piling up in cities

Here’s a great feature from Bloomberg about discarded electric vehicles piling in China.

***

‘On the outskirts of the Chinese city of Hangzhou, a small dilapidated temple overlooks a graveyard of sorts: a series of fields where hundreds upon hundreds of electric cars have been abandoned among weeds and garbage.

‘Similar pools of unwanted battery-powered vehicles have sprouted up in at least half a dozen cities across China, though a few have been cleaned up. In Hangzhou, some cars have been left for so long that plants are sprouting from their trunks. Others were discarded in such a hurry that fluffy toys still sit on their dashboards.

‘The scenes recall the aftermath of the nation’s bike-sharing crash in 2018, when tens of millions of bicycles ended up in rivers, ditches and disused parking lots after the rise and fall of startups backed by big tech such as Ofo and Mobike.

‘This time, the cars were likely deserted after the ride-hailing companies that owned them failed, or because they were about to become obsolete as automakers rolled out EV after EV with better features and longer driving ranges. They’re a striking representation of the excess and waste that can happen when capital floods into a burgeoning industry, and perhaps also an odd monument to the seismic progress in electric transportation over the last few years.’

Source: Bloomberg

China’s abandoned, obsolete EVs piling up in cities

Here’s a great feature from Bloomberg about discarded electric vehicles piling in China.

***

‘On the outskirts of the Chinese city of Hangzhou, a small dilapidated temple overlooks a graveyard of sorts: a series of fields where hundreds upon hundreds of electric cars have been abandoned among weeds and garbage.

‘Similar pools of unwanted battery-powered vehicles have sprouted up in at least half a dozen cities across China, though a few have been cleaned up. In Hangzhou, some cars have been left for so long that plants are sprouting from their trunks. Others were discarded in such a hurry that fluffy toys still sit on their dashboards.

‘The scenes recall the aftermath of the nation’s bike-sharing crash in 2018, when tens of millions of bicycles ended up in rivers, ditches and disused parking lots after the rise and fall of startups backed by big tech such as Ofo and Mobike.

‘This time, the cars were likely deserted after the ride-hailing companies that owned them failed, or because they were about to become obsolete as automakers rolled out EV after EV with better features and longer driving ranges. They’re a striking representation of the excess and waste that can happen when capital floods into a burgeoning industry, and perhaps also an odd monument to the seismic progress in electric transportation over the last few years.’

Source: Bloomberg

Investing in absolute scarcity like this Greek philosopher: Ryan Dinse

Excerpt from Ryan Dinse’s piece for The Insider.

***

I want to do something a bit different for today’s Insider and tell you the tale of one famous Greek philosopher who made his fortune with just one perfectly timed trade.

Most importantly, he did it by understanding the concept of ‘absolute scarcity.’

What’s that?

Here’s the formal definition of ‘absolute scarcity’ from Investopedia.

‘Something that has a fixed limit on its supply. In other words, no matter how much demand grows you cannot create more of it. This means the price can rise exponentially if demand rises.’

Opportunities like this are rare.

After all, when demand for something increases, usually, the supply will increase too as producers look to share in the profits.

With something that’s absolutely scarce, that doesn’t happen.

When demand goes up, supply stays exactly the same.

The only thing that can react is the price.

This means with absolutely scarce assets, the price can go absolutely vertical when demand shoots higher.

This was key to how our old Greek friend nailed the perfect trade more than 2,600 years ago.

Here’s what happened…

It’s 600 BC, and you’re living in Ancient Greece, the heart of the civilised world.

It’s an exciting time to be alive. The world is changing, and new ideas are being debated daily by the intellectual giants of the day.

You’re interested in it all.

Astronomy, philosophy, geometry…everything.

There’s only one problem.

Money.

Or, more accurately, lack of it.

While you’d much rather wile away your days working out how to calculate the various dimensions of a circle…or be down at the forum arguing what the fundamental building blocks of life are…instead, you’re stuck in the daily grind.

The 9–5 of ancient Greek life (or more like the 5–9 back then). Some things never change!

In fact, this was the pickle a bloke called Thales of Miletus found himself in.

Thales was a smart guy, but he was also poor, so no one who mattered took him seriously.

He was determined to change that…

So, the ambitious Thales started looking for an asymmetric investing opportunity. An opportunity where he could risk a little for the possibility of earning a lot.

He needed to make money as fast as possible so he could spend his life doing what he wanted to do, not ‘working.’

As a mathematician, he naturally hit upon an investing idea that followed the basic precepts of supply and demand — namely, the concept of absolute scarcity.

He knew if he could find something that was limited in supply just before demand increased, the price would rise exponentially.

But where could he find such an opportunity?

The answer was staring him in the face.

Or, rather, on his dinner plate.

Olives.

Back in those days, olives were used for many things aside from eating, especially oil.

Olive oil was used as a perfume, as fuel for lamps, in funeral ceremonies, as a type of soap to collect dirt and sweat from the body, and, as it is today, for cooking.

Olives also had a religious connotation and were considered by Athenians as a gift from the God Athena herself.

All of this made olive oil very valuable to the ancient Greeks.

And Thales saw the huge opportunity coming from this…

You see, the general consensus that year was that the coming olive harvest was going to be a poor one.

Everyone said so.

But Thales thought differently.

He’d done his homework, studied the stars and the weather patterns, and he thought it was actually going to be a bumper crop.

Today, we’d call such insight ‘alpha’ — something that the market hasn’t priced in.

But how could he make the most of this alpha?

Here’s what Thales did…

Bit by bit, he proceeded to rent out all the olive presses used for making olive oil in the region before the harvest season.

He managed to rent them out cheaply because ‘everyone’ knew it was going to be a poor harvest that year. So, if you owned a press, why not guarantee some income ahead of time?

By the time harvest time came along, Thales basically had a monopoly on all the presses on Miletus and Chios.

It was a license to print money!

When the bumper crop he predicted arrived, he was able to re-let the presses out to the olive producers at a considerable profit.

Such was this financial success; Thales did indeed manage to retire early and spend his days philosophising about the universe.

Today, he’s remembered as one of the first in a line of Ancient Greek thought that led to the likes of Socrates, Plato, and Aristotle.

He was a pioneer of rationality over superstition.

But his shrewd olive oil play is also one of the earliest recorded examples of an investor using the concept of absolute scarcity to their advantage.

Remember: this refers to the supply of something that cannot be increased no matter how much demand for it goes up.

Thales knew it wasn’t possible to whip up industrial-scale olive oil presses in time for the harvest, no matter how many olives there were.

Investing in absolute scarcity like this Greek philosopher: Ryan Dinse

Excerpt from Ryan Dinse’s piece for The Insider.

***

I want to do something a bit different for today’s Insider and tell you the tale of one famous Greek philosopher who made his fortune with just one perfectly timed trade.

Most importantly, he did it by understanding the concept of ‘absolute scarcity.’

What’s that?

Here’s the formal definition of ‘absolute scarcity’ from Investopedia.

‘Something that has a fixed limit on its supply. In other words, no matter how much demand grows you cannot create more of it. This means the price can rise exponentially if demand rises.’

Opportunities like this are rare.

After all, when demand for something increases, usually, the supply will increase too as producers look to share in the profits.

With something that’s absolutely scarce, that doesn’t happen.

When demand goes up, supply stays exactly the same.

The only thing that can react is the price.

This means with absolutely scarce assets, the price can go absolutely vertical when demand shoots higher.

This was key to how our old Greek friend nailed the perfect trade more than 2,600 years ago.

Here’s what happened…

It’s 600 BC, and you’re living in Ancient Greece, the heart of the civilised world.

It’s an exciting time to be alive. The world is changing, and new ideas are being debated daily by the intellectual giants of the day.

You’re interested in it all.

Astronomy, philosophy, geometry…everything.

There’s only one problem.

Money.

Or, more accurately, lack of it.

While you’d much rather wile away your days working out how to calculate the various dimensions of a circle…or be down at the forum arguing what the fundamental building blocks of life are…instead, you’re stuck in the daily grind.

The 9–5 of ancient Greek life (or more like the 5–9 back then). Some things never change!

In fact, this was the pickle a bloke called Thales of Miletus found himself in.

Thales was a smart guy, but he was also poor, so no one who mattered took him seriously.

He was determined to change that…

So, the ambitious Thales started looking for an asymmetric investing opportunity. An opportunity where he could risk a little for the possibility of earning a lot.

He needed to make money as fast as possible so he could spend his life doing what he wanted to do, not ‘working.’

As a mathematician, he naturally hit upon an investing idea that followed the basic precepts of supply and demand — namely, the concept of absolute scarcity.

He knew if he could find something that was limited in supply just before demand increased, the price would rise exponentially.

But where could he find such an opportunity?

The answer was staring him in the face.

Or, rather, on his dinner plate.

Olives.

Back in those days, olives were used for many things aside from eating, especially oil.

Olive oil was used as a perfume, as fuel for lamps, in funeral ceremonies, as a type of soap to collect dirt and sweat from the body, and, as it is today, for cooking.

Olives also had a religious connotation and were considered by Athenians as a gift from the God Athena herself.

All of this made olive oil very valuable to the ancient Greeks.

And Thales saw the huge opportunity coming from this…

You see, the general consensus that year was that the coming olive harvest was going to be a poor one.

Everyone said so.

But Thales thought differently.

He’d done his homework, studied the stars and the weather patterns, and he thought it was actually going to be a bumper crop.

Today, we’d call such insight ‘alpha’ — something that the market hasn’t priced in.

But how could he make the most of this alpha?

Here’s what Thales did…

Bit by bit, he proceeded to rent out all the olive presses used for making olive oil in the region before the harvest season.

He managed to rent them out cheaply because ‘everyone’ knew it was going to be a poor harvest that year. So, if you owned a press, why not guarantee some income ahead of time?

By the time harvest time came along, Thales basically had a monopoly on all the presses on Miletus and Chios.

It was a license to print money!

When the bumper crop he predicted arrived, he was able to re-let the presses out to the olive producers at a considerable profit.

Such was this financial success; Thales did indeed manage to retire early and spend his days philosophising about the universe.

Today, he’s remembered as one of the first in a line of Ancient Greek thought that led to the likes of Socrates, Plato, and Aristotle.

He was a pioneer of rationality over superstition.

But his shrewd olive oil play is also one of the earliest recorded examples of an investor using the concept of absolute scarcity to their advantage.

Remember: this refers to the supply of something that cannot be increased no matter how much demand for it goes up.

Thales knew it wasn’t possible to whip up industrial-scale olive oil presses in time for the harvest, no matter how many olives there were.

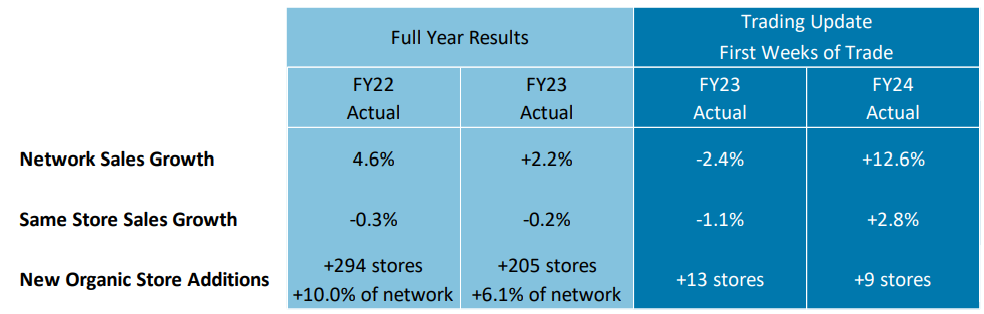

Domino’s Pizza up 7.5% despite profit sinking 74%

Pizza chain Domino’s Pizza [ASX:DMP] is up 7.5% in late afternoon trade despite FY23 net profit falling 74% to $40.6 million.

Based on that figure, the pizza merchant is trading on a trailing P/E ratio of 112.

Quite the multiple for a franchise doling out pepperoni pizzas.

The surge in the stock is surprising, too, given consensus estimates compiled by Market Screener had Domino’s net profit reaching over $80 million.

That’s quite the miss, isn’t it?

Maybe the jump today is about a better than expected outlook?

Domino’s said it expects FY24 to deliver ‘material sales and earnings improvements’, mainly stemming from ‘structural savings’.

It also gave a positive trading update for the first seven weeks of FY24.

Network sales grew 12.6% during the stretch and same store sales rose 2.8%.

Source: Domino’s

On the face of it, somewhat rare to see a stock rally when the CEO makes the below pledge. I guess they know their value proposition. $DMP. pic.twitter.com/6G8kCFN3vl

— David Berthon-Jones (@berthon_jones) August 23, 2023

Domino’s Pizza up 7.5% despite profit sinking 74%

Pizza chain Domino’s Pizza [ASX:DMP] is up 7.5% in late afternoon trade despite FY23 net profit falling 74% to $40.6 million.

Based on that figure, the pizza merchant is trading on a trailing P/E ratio of 112.

Quite the multiple for a franchise doling out pepperoni pizzas.

The surge in the stock is surprising, too, given consensus estimates compiled by Market Screener had Domino’s net profit reaching over $80 million.

That’s quite the miss, isn’t it?

Maybe the jump today is about a better than expected outlook?

Domino’s said it expects FY24 to deliver ‘material sales and earnings improvements’, mainly stemming from ‘structural savings’.

It also gave a positive trading update for the first seven weeks of FY24.

Network sales grew 12.6% during the stretch and same store sales rose 2.8%.

Source: Domino’s

On the face of it, somewhat rare to see a stock rally when the CEO makes the below pledge. I guess they know their value proposition. $DMP. pic.twitter.com/6G8kCFN3vl

— David Berthon-Jones (@berthon_jones) August 23, 2023

Buy the dip on this fake China crisis: Callum Newman

I had to laugh yesterday. A mate of mine had me on the phone wondering if the ASX was about to take a big dive.

Apparently, investor Michael Burry is short the US market. The reason I chuckled is that in January, my buddy had me on the phone…wanting to get in the market for some action!

Why does anyone care about Burry, anyway?

The movie The Big Short made Burry famous for his big trade shorting the US market before the 2008 collapse. I guess he’s going for number two. Or is it three, four, or five?

What I mean is that many investors and traders who ‘predicted’ the 2008 collapse also did so in the years before and after it happened too.

As in, if you keep saying the same thing for long enough…hey, eventually you’ll be right!

Burry’s short gives Aussie investors a bit more to quake in their boots about alongside the fact that everyone is again worried about China.

I say again, because it’s pretty much been a constant theme for the last 10 years.

Here’s my problem with it: the problems in the Chinese property market are obvious and well known. The market has already priced in what is obvious.

Yes…Chinese youth unemployment is high. I get it.

Have you ever been to Spain? Half the people under 35 still live with their parents and think a permanent work contract is as likely as seeing a unicorn in the local bar.

You don’t hear the Western press worrying about Europe’s effort in this metric do you?

Then there’s the little problem of iron ore for the China bears.

Back in 2015, when China and the world were looking at lot worse than now, the iron ore price was less than US$50 a tonne.

If you check your paper today, you’ll see that it’s around US$110 now and at a three-week high.

Whatever you think about the world right now, the fact is this is historically a high price and Aussie miners are still rocking great margins off this.

BHP’s dividends last financial year were still the fourth highest in its history. This is after Chinese property has been on the ropes since about August 2021.

Personally, I think this current China spook is already over. The Aussie market has been down almost the entire month of August. It’s battered…but the world keeps turning.

Take a step back and, if you can, put your emotions aside. The volatility in the stock market can jerk you around like a washing machine.

What I’ve found works for me is understanding and researching the actual businesses that trade on the stock market.

You have to see the current market for what it is…that’s a chance to accumulate cheap stocks!

When else do you get a look at the best prices except when everyone has their knickers in a knot and would rather huddle in cash in the delusion they’re getting a 5% return. Inflation at 5% means your return is actually zero.

https://www.moneymorning.com.au/20230823/buy-the-dip-on-this-fake-china-crisis.html

Buy the dip on this fake China crisis: Callum Newman

I had to laugh yesterday. A mate of mine had me on the phone wondering if the ASX was about to take a big dive.

Apparently, investor Michael Burry is short the US market. The reason I chuckled is that in January, my buddy had me on the phone…wanting to get in the market for some action!

Why does anyone care about Burry, anyway?

The movie The Big Short made Burry famous for his big trade shorting the US market before the 2008 collapse. I guess he’s going for number two. Or is it three, four, or five?

What I mean is that many investors and traders who ‘predicted’ the 2008 collapse also did so in the years before and after it happened too.

As in, if you keep saying the same thing for long enough…hey, eventually you’ll be right!

Burry’s short gives Aussie investors a bit more to quake in their boots about alongside the fact that everyone is again worried about China.

I say again, because it’s pretty much been a constant theme for the last 10 years.

Here’s my problem with it: the problems in the Chinese property market are obvious and well known. The market has already priced in what is obvious.

Yes…Chinese youth unemployment is high. I get it.

Have you ever been to Spain? Half the people under 35 still live with their parents and think a permanent work contract is as likely as seeing a unicorn in the local bar.

You don’t hear the Western press worrying about Europe’s effort in this metric do you?

Then there’s the little problem of iron ore for the China bears.

Back in 2015, when China and the world were looking at lot worse than now, the iron ore price was less than US$50 a tonne.

If you check your paper today, you’ll see that it’s around US$110 now and at a three-week high.

Whatever you think about the world right now, the fact is this is historically a high price and Aussie miners are still rocking great margins off this.

BHP’s dividends last financial year were still the fourth highest in its history. This is after Chinese property has been on the ropes since about August 2021.

Personally, I think this current China spook is already over. The Aussie market has been down almost the entire month of August. It’s battered…but the world keeps turning.

Take a step back and, if you can, put your emotions aside. The volatility in the stock market can jerk you around like a washing machine.

What I’ve found works for me is understanding and researching the actual businesses that trade on the stock market.

You have to see the current market for what it is…that’s a chance to accumulate cheap stocks!

When else do you get a look at the best prices except when everyone has their knickers in a knot and would rather huddle in cash in the delusion they’re getting a 5% return. Inflation at 5% means your return is actually zero.

https://www.moneymorning.com.au/20230823/buy-the-dip-on-this-fake-china-crisis.html

Pepper Money down 15% after half-year NPAT falls 28% and originations plummet

Non-bank lender Pepper Money [ASX:PPM] is down 15% after the latest half-year results showed a drop in profit, net interest margin (NIM) and originations.

- Statutory NPAT fell 28% YoY to $52 million

- NIM fell 23bp YoY to 2.06%

- Originations fell 38% YoY to $3.5 billion

PPM chief executive Mario Rehayem said the Reserve Bank’s rate hikes had a ‘pronounced impact on credit demand in mortgages’.

He further said the mortgage market ‘has been challenging with intense competitive behaviour as the major banks sought to gain share through cash back offers and other incentives driving higher levels of customer attrition’.

Pepper Money’s mortgage originations fell 58% YoY to $1.7 billion.

$PPM is down 15% after the latest half-year results showed a drop in profit, NIM and originations.

– Statutory NPAT fell 28% YoY to $52 million

– NIM fell 23bp YoY to 2.06%

– Originations fell 38% YoY to $3.5 billion$PPM.AX #ASX #PepperMoney pic.twitter.com/SYdq0OeYzv— Fat Tail Daily (@FatTailDaily) August 23, 2023

Pepper Money down 15% after half-year NPAT falls 28% and originations plummet

Non-bank lender Pepper Money [ASX:PPM] is down 15% after the latest half-year results showed a drop in profit, net interest margin (NIM) and originations.

- Statutory NPAT fell 28% YoY to $52 million

- NIM fell 23bp YoY to 2.06%

- Originations fell 38% YoY to $3.5 billion

PPM chief executive Mario Rehayem said the Reserve Bank’s rate hikes had a ‘pronounced impact on credit demand in mortgages’.

He further said the mortgage market ‘has been challenging with intense competitive behaviour as the major banks sought to gain share through cash back offers and other incentives driving higher levels of customer attrition’.

Pepper Money’s mortgage originations fell 58% YoY to $1.7 billion.

$PPM is down 15% after the latest half-year results showed a drop in profit, NIM and originations.

– Statutory NPAT fell 28% YoY to $52 million

– NIM fell 23bp YoY to 2.06%

– Originations fell 38% YoY to $3.5 billion$PPM.AX #ASX #PepperMoney pic.twitter.com/SYdq0OeYzv— Fat Tail Daily (@FatTailDaily) August 23, 2023

WiseTech’s soft guidance the likely culprit for steep fall

A soft FY24 outlook is likely the reason for WiseTech’s sharp fall on Wednesday.

WiseTech’s updated FY24 guidance now sits at:

- Revenue of $1,040-$1,095 million (up 27-34%)

- EBITDA of $455-$490 million (up 18-27%)

If we look at WTC’s FY24 consensus forecasts, we see that WiseTech’s guidance came in below the market’s expectations.

The market pencilled in FY24 revenue of $1,087 million and EBITDA of $539 million.

On that front, WTC’s EBITDA guidance is well below what the market expected.

The lower EBITDA was attributed to recent acquisitions, which the company said ‘will continue to dilute the overall EBITDA margin while being integrated.’

WiseTech does anticipate EBITDA margins to return above 50% in FY26.

Meaning it expects EBITDA margins to stay below 50% for the next few years.

WiseTech did not provide a net profit guidance but we can hazard a guess.

In FY23, WiseTech’s net profit to EBITDA margin was about 55%. If we take the midpoint of WTC’s FY24 EBITDA guidance of $472.5 million and assume the margin remains at 55%, we get a net profit estimate of $259.9 million.

That seems too high — and WTC wouldn’t have hesitated to broadcast the figure.

At a 50% margin, FY24 net profit reduces to $236.3 million. At 45%, net profit slumps to $212.6 million.

$WTC said recent acquisitions will 'continue to dilute the overall EBITDA margin while being integrated'. #WiseTech expects EBITDA margins to be above 50% in FY26. $WTC.AX #ASX pic.twitter.com/4WfN0oxzLh

— Fat Tail Daily (@FatTailDaily) August 23, 2023

WiseTech’s soft guidance the likely culprit for steep fall

A soft FY24 outlook is likely the reason for WiseTech’s sharp fall on Wednesday.

WiseTech’s updated FY24 guidance now sits at:

- Revenue of $1,040-$1,095 million (up 27-34%)

- EBITDA of $455-$490 million (up 18-27%)

If we look at WTC’s FY24 consensus forecasts, we see that WiseTech’s guidance came in below the market’s expectations.

The market pencilled in FY24 revenue of $1,087 million and EBITDA of $539 million.

On that front, WTC’s EBITDA guidance is well below what the market expected.

The lower EBITDA was attributed to recent acquisitions, which the company said ‘will continue to dilute the overall EBITDA margin while being integrated.’

WiseTech does anticipate EBITDA margins to return above 50% in FY26.

Meaning it expects EBITDA margins to stay below 50% for the next few years.

WiseTech did not provide a net profit guidance but we can hazard a guess.

In FY23, WiseTech’s net profit to EBITDA margin was about 55%. If we take the midpoint of WTC’s FY24 EBITDA guidance of $472.5 million and assume the margin remains at 55%, we get a net profit estimate of $259.9 million.

That seems too high — and WTC wouldn’t have hesitated to broadcast the figure.

At a 50% margin, FY24 net profit reduces to $236.3 million. At 45%, net profit slumps to $212.6 million.

$WTC said recent acquisitions will 'continue to dilute the overall EBITDA margin while being integrated'. #WiseTech expects EBITDA margins to be above 50% in FY26. $WTC.AX #ASX pic.twitter.com/4WfN0oxzLh

— Fat Tail Daily (@FatTailDaily) August 23, 2023

WiseTech opens 15% lower on FY23 results

WiseTech is down 15% in early trade after releasing its FY23 results.

While total revenue came in slightly ahead of consensus forecasts, up 29% to $816.8 million (forecast $811 million), net profit undershot consensus estimates.

Net profit rose 9% to $212.2 million. Consensus estimates had net profit coming in at $235 million.

EBITDA was also below expectations, rising 21% to $385.7 million (forecast $399 million).

Quick market recap

Good morning!

Retail and tech stocks had diverging fates to start the week.

Adairs closed 15% lower on Monday and Kogan closed 11% lower on Tuesday.

It suggests we haven’t hit peak pessimism yet about the industry.

The worst hasn’t yet been priced in. If it was, these stocks wouldn’t fall so sharply on the results.

But tech stocks enjoyed a great day yesterday.

Altium closed 25% higher, Megaport closed 17% higher, HUB24 close 11% higher, Nuix and Audinate finished about 10% higher.

The whole Information Technology sector rose a whopping 5.2% yesterday.

The Aussie information tech index is up 38% year to date, while the ASX 200 is up only 2.5%. Since its June 2022 low, the tech index is up 50% and is knocking on its 52-week high.

Question: Is this through realised earnings growth or multiple expansion driven by optimistic growth forecasts 1-5 years ahead?

And then we had Supermarket stalwart Coles nearly hit a 52-week low on Tuesday after sinking 7% following the release of its FY23 results.

That’s a hefty move for a stock of its stature.

Part of the sell-off was due to unmet expectations. COL’s revenue and profit both undershot consensus forecasts.

Coles said total price inflation in supermarkets is moderating. Inflation was 5.8% in the fourth quarter, down from 6.2% in the third quarter.

Woolworths reported today, too. Along with Domino’s Pizza. More on those later.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988