ASX News LIVE | XJO Falls; Janus Henderson, Link, Solvar Feature

Biden reneges on oil reserve resupply as prices rises: Ryan Clarkson-Ledward

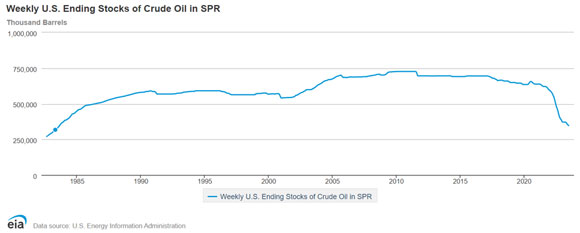

Do you remember President Biden’s oil gambit?

In March last year, Joe Biden made the drastic decision to free up US oil reserves. At the time, he called for 180 million barrels to be released in order to cool petrol prices.

In reality, it would be much more over the course of the past 14 months or so.

Just look at the dent his mandate has put in the Strategic Petroleum Reserve (SPR):

Source: Forbes

This vital release of oil has pushed the reserve to its lowest amount in more than 40 years. It was a move that sparked plenty of debate about the long-term energy security of the US.

However, Biden’s administration has stated that it’s committed to refilling the reserves. Energy Secretary Jennifer Granholm bluntly stated that ‘the bottom line is we are going to replenish’.

The real question, though, is when it will be replenished…

Because earlier this week, on Tuesday, Biden’s team backed out of an offer to buy 6 million barrels of oil. According to a spokesman knowledgeable on the deal, market conditions didn’t suit the US Government’s goals.

In other words, with oil prices on the up, they didn’t want to pay overs.

But that just begs the question, what happens if or when they need to buy in a few months’ time?

https://www.moneymorning.com.au/20230803/biden-reneges-on-oil-reserve-resupply-as-prices-soar.html

US downgrade not the culprit for global selloff

In the latest Chanticleer column, James Thomson took issue with the easy explanation for the global sell-off yesterday.

The US downgrade is not to blame.

Look to bond yields instead:

‘While the downgrade of the United States’ credit rating by Fitch on Tuesday night was the talk of the financial world … investors were more spooked by the action in US bond markets, where the 10-year US Treasury hit its highest point in 2023, briefly touching 4.12 per cent before drifting lower.

‘Two factors pushed bond yields higher.

‘Firstly, there was more good news on the US jobs front, with a survey of private payrolls by the ADP Research Institute showing jobs increased by 324,000, well above expectations for a gain of 190,000. Resilience in employment is notionally good for the US economy, but the concern among bond traders is that a too-hot labour market could force the Federal Reserve to raise rates further still.

‘The second factor to push yields higher was news from the US Treasury Department, which said it plans to sell $US103 billion ($158 billion) of long-term debt next week, which was up from its previous estimate of $US96 billion and more than most analysts had expected. This news also put upwards pressure on 10-year Treasury yields, as investors bet the US government might have to offer better terms to attract demand for its bond sale.’

Solvar continues to tumble

Solvar is now down nearly 40% in morning trade after forecasting its net profit after tax to crater in FY24.

Today’s steep fall means the lender is now trading at a new 52-week low of ~1.06 a share. It closed yesterday at $1.75 a share.

Next 12 months will throw up fantastic opportunities: Callum Newman

The Reserve Bank kept interest rates on hold.

Overall, the reaction was muted. I’d say most stocks had moved in advance of the official announcement.

However, looking out to the end of the year, there’s good news for investors in all of this.

It’s likely rates stay on hold until next year some time.

Rising rates have been a big headwind for the market over the last 12 months.

Now investors can move confidently knowing that monetary policy is more predictable.

In fact, they already are.

I can say that with reasonable confidence because some of the stocks in my portfolios for Small-Cap Systems and Australian Small-Cap Investigator have lifted quite strongly since March.

For my money, the most astonishing thing about Tuesday had nothing to do with the RBA.

A company called Credit Corp [ASX:CCP] came out with its financial year results.

Look at what the Australian Financial Review observed about it:

‘The number of Australians struggling to pay their credit card bills is small and showing few signs of growth, despite repeated interest rate rises, the soaring cost of living and a softening economy.

‘Credit Corp boss Thomas Beregi, whose business buys books of distressed credit card and personal loans customers off the banks, says the Australian consumer is “still in really good shape” with few borrowers either in arrears or default.’

Hey, I want hours of my life back!

The drumbeat of negativity since the start of 2022 has almost never ended. I’ve been reading a mountain of it ever since.

There were calls for a 30–40% drop in house prices, mortgage cliffs, and recession.

The reality is the ASX today is within striking distance of its all-time high.

By hook or by crook, Australia has gone through the fastest rate hike in a generation and come through it in reasonable shape.

However, it wasn’t smooth sailing.

Here’s a chart of volatility (via the VIX Index) over 2022 as all these fears washed through the market.

It went haywire:

|

| Source: Optuma |

This is part of what made the 2022 market so hard through the middle of the year.

The good news is volatility has waned substantially in 2023.

This should make ‘momentum’-style trading and positioning much easier to achieve than last year.

Volatility is the opposite of trend.

What’s good about that?

It’s less stressful, for a start! Plus, you can get some ripping runs that, at times, feel effortless.

There’s nothing without risk, of course, but I expect the next 12 months to throw up some fantastic investment and trading opportunities.

Lake Resources falls to new low

Once a retail favourite, now a retail reject.

Lithium hopeful Lake Resources [ASX:LKE] is down over 5% today, sinking to a new 52-week low of ~20 cents a share.

The last time LKE shares were this low was in January 2021.

Source: CommSec

When should you sell stocks?

It is a common refrain that investors sell winners too early and losers too late. A horticultural variant gets to the same idea; investors cut the flowers and water the weeds.

But why?

This backward tendency has a name in academic literature — the disposition effect.

Countless studies have shown individual investors are more likely to sell a stock that has gone up than one that has gone down.

But the literature is ambivalent on why. An oft-cited paper in The Journal of Finance writes:

‘While the disposition effect is a fundamental feature of trading, its underlying cause remains unclear. Why do individual investors have a greater propensity to sell stocks trading at a paper gain rather than those trading at a paper loss? In a careful study of the disposition effect, Odean (1998) shows that the most obvious potential explanations — explanations based on informed trading, rebalancing, or transaction costs — fail to capture important features of the data.’

In the absence of clear explanations, behavioural economists suggest the answer lies in our aversion to risk.

According to prospect theory — espoused by Kahneman and Tversky — we are more sensitive to losses than gains.

In a weird twist, we are risk-averse to gains but risk-seeking to losses. As the earlier mentioned paper explains:

‘Prospect theory, a prominent theory of decision-making under risk proposed by Kahneman and Tversky (1979) and extended by Tversky and Kahneman (1992), posits that people evaluate gambles by thinking about gains and losses, not final wealth levels, and that they process these gains and losses using a value function that is concave for gains and convex for losses. The value function is designed to capture the experimental finding that people tend to be risk-averse over moderate-probability gains (they typically prefer a certain $100 to a 50:50 bet to win $0 or $200), but tend to be risk-seeking over moderate-probability losses (they typically prefer a 50:50 bet to lose $0 or $200 to a certain loss of $100).’

That’s very interesting.

Investors sitting on a $1,000 paper loss tend to prefer a 50/50 bet of either breaking even or losing $2,000 over booking a certain loss of $1,000.

This rings true. How many times have you heard people say, ‘I’ve already lost XX% on this stock, I might as well hold in case it turns around’.

But this response contains a subtly different explanation for the disposition effect.

https://www.moneymorning.com.au/20230801/when-to-sell-stocks-2.html

Solvar cautious on FY24 outlook, expects big hit to NPAT

Solvar expects to grow its loan book in FY24 ‘in excess of $1 billion’ but for EBITDA to be largely flat, ‘broadly consistent with FY23’.

Bad debt performance is expected to remain in the range of 3.5% to 4.5%.

Quite steep.

Despite forecasting loan book growth, Solvar said it will ‘temporarily slow loan book growth in New Zealand with an increasing focus on servicing existing customers’ loans’.

The firm will also aim to lift ‘front book margin’ and implement ‘productivity initiatives’ to improve efficiency ratios.

However, the biggest news was the expected hit to net profit after tax.

Solvar expects FY24 NPAT between $24 million to $30 million, well down on FY23. FY22, and FY21.

FY24’s NPAT will be the lowest since FY20, when it totalled $22.2 million.

Commenting on the news, management said:

‘FY24 NPAT will be impacted by the full year cost of central banks rate rise cycle. Increases in funding costs are being passed through on new loans written, however it reduces the profit contribution from the back book. Management expects profitability to exceed historical levels beyond FY24, as we continue to maintain and expand yield on new loan originations.’

Some gold miners having a better day

After yesterday’s broad sell-off in the mining sector, some Aussie gold companies are having a better day today.

As of this morning, the mining sector is down 1%, but there are some pockets of gold.

Tietto Minerals [ASX:TIE] announced today that it managed to increase gold production to 11,643 ounces of gold in July.

This was with less than half the total tonnage of ore processed in previous months, as the company said it moved into a higher grade 1.0 g/t ore.

Bellevue Gold [ASX:BGL] said it had encountered an ‘exceptionally high-grade’ mineralisation with results including 18.4m at 52.9 g/t gold while conducting infill drilling at the Bellevue Gold Project.

Gold exploration junior Kalamazoo Resources [ASX:KZR] also announced ‘exceptionally high’ gold assay results (up to 74 g/t) from rock chip samples from its Mt Piper Gold Project in Central Victoria.

Solvar crashes 25% on market update

Solvar [ASX:SVR] — formerly Money3 — is down 25% after releasing a trading update the market did not take kindly to.

The automotive finance firm said, ‘subject to audit’, its FY23 results are in line with guidance.

Net profit after tax is expected to be $47.6 million, with revenue up 11.4% to $209.3 million. In FY22, NPAT came in at $51.6 million.

Solvar’s total loan book lifted 24.1% to $910.1 million n FY23.

In May, Solvar’s subsidiary Money3 Loans, was served with proceedings by ASIC. The regulator alleged that between 2019 and 2021, Money3 Loans breached its responsible lending obligations and failed to adequately train its staff.

The firm said it will defend the charges levied by ASIC.

Who is Fitch and why did they downgrade U.S credit?

Fitch is one of the top three credit rating agencies internationally, along with Moody’s and Standard & Poor.

Most rating agencies use the same letter system to rate the viability of investments relative to the likelihood of default.

AAA: companies are of exceptional quality.

AA: Still high quality with low default risk

All the way down to D, where the company has defaulted.

Fitch Ratings downgraded the US credit rating from AAA to AA+, citing the country’s repeated debt limit standoffs and last-minute resolutions.

This is the second time the US has been downgraded, the first being in 2011 by S&P Global Ratings.

The downgrade means that the US no longer has the highest credit quality, but it is still considered to be a very strong borrower.

The impact of the downgrade on financial markets is likely to be short-lived, as investors are more focused on the Federal Reserve’s interest rate hikes.

The group of countries that still have top ratings is declining, and China’s rating is three notches lower than the US.

Morning market update

ASX 200 opened down 0.29% today at 7,333.2 following global markets after Fitch rating agency downgraded US credit from AAA to AA+.

A fairly inconsequential move paved the way for a brutal day on Wall Street, with S&P 500 experiencing its biggest drop since April of 1.38% , while the tech-heavy Nasdaq fell 2.17%.

European and Asian stocks also followed suit overnight, with Hong Kong’s Hang Send index dropping 2.5% and the Stoxx Euro 600 closed down 1.4%

The Aussie dollar fell sharply overnight, losing 1.0% to its US counterpart.

- $AUD down -1.0% at 65.44 US cents

- ASX futures up slightly +0.07% to 7,246.5

- S&P 500 down -1.38%

- NASDAQ down -2.17%

- DOW down -0.98%

- FTSE down -1.36%

- STOXX down -1.31%

- SSE down -0.89%

- Bitcoin down -1.92% to $US 29,154.47

- Spot gold down -0.80% to $US 1,936.75

- Iron ore down -3.68% to $US 108.32

- Brent Crude down -0.22% to $US 83.38pb

All figures shown are from 10:10am AEST

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988