ASX News LIVE | XJO Down, Treasury Yields Hit 16-Year High as Market Braces for Fed Meeting

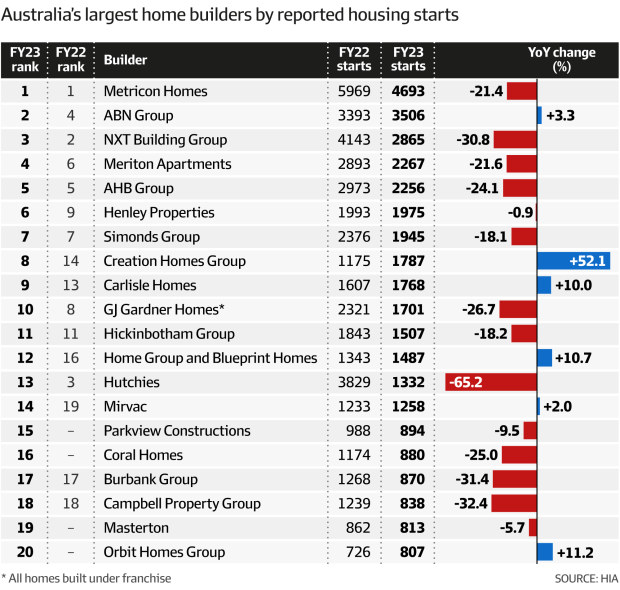

Biggest Aussie builders struggle as housing starts fall

On the topic of housing supply, the AFR just reported that Australia’s biggest home builders have suffered a 23% fall in new housing starts last year.

Housing starts for Australia’s 100 largest builders fell to a decade-low in FY23, the lowest since 2013.

And while starts fell, insolvencies rose 73% as builders, saddled with fixed price contracts, struggled with labour shortages and rising input costs.

Biggest Aussie builders struggle as housing starts fall

On the topic of housing supply, the AFR just reported that Australia’s biggest home builders have suffered a 23% fall in new housing starts last year.

Housing starts for Australia’s 100 largest builders fell to a decade-low in FY23, the lowest since 2013.

And while starts fell, insolvencies rose 73% as builders, saddled with fixed price contracts, struggled with labour shortages and rising input costs.

AMP’s Shane Oliver calls for immigration level to be reduced to improve housing affordability

AMP’s chief economist Shane Oliver thinks the ‘level of immigration should be reduced’ to improve ‘poor’ housing affordability in Australia.

In a research note, Oliver wrote:

‘The role of high immigration levels (now about 500,000 per annum) can’t be ignored. On our estimates it needs to be cut back to nearer 200,000 people a year to line up with building industry capacity & to reduce the supply shortfall.’

Oliver argued ‘deteriorating housing affordability is something to be concerned about as it is driving increasing inequality and could threaten social cohesion’.

Threaten social cohesion! Interesting claim.

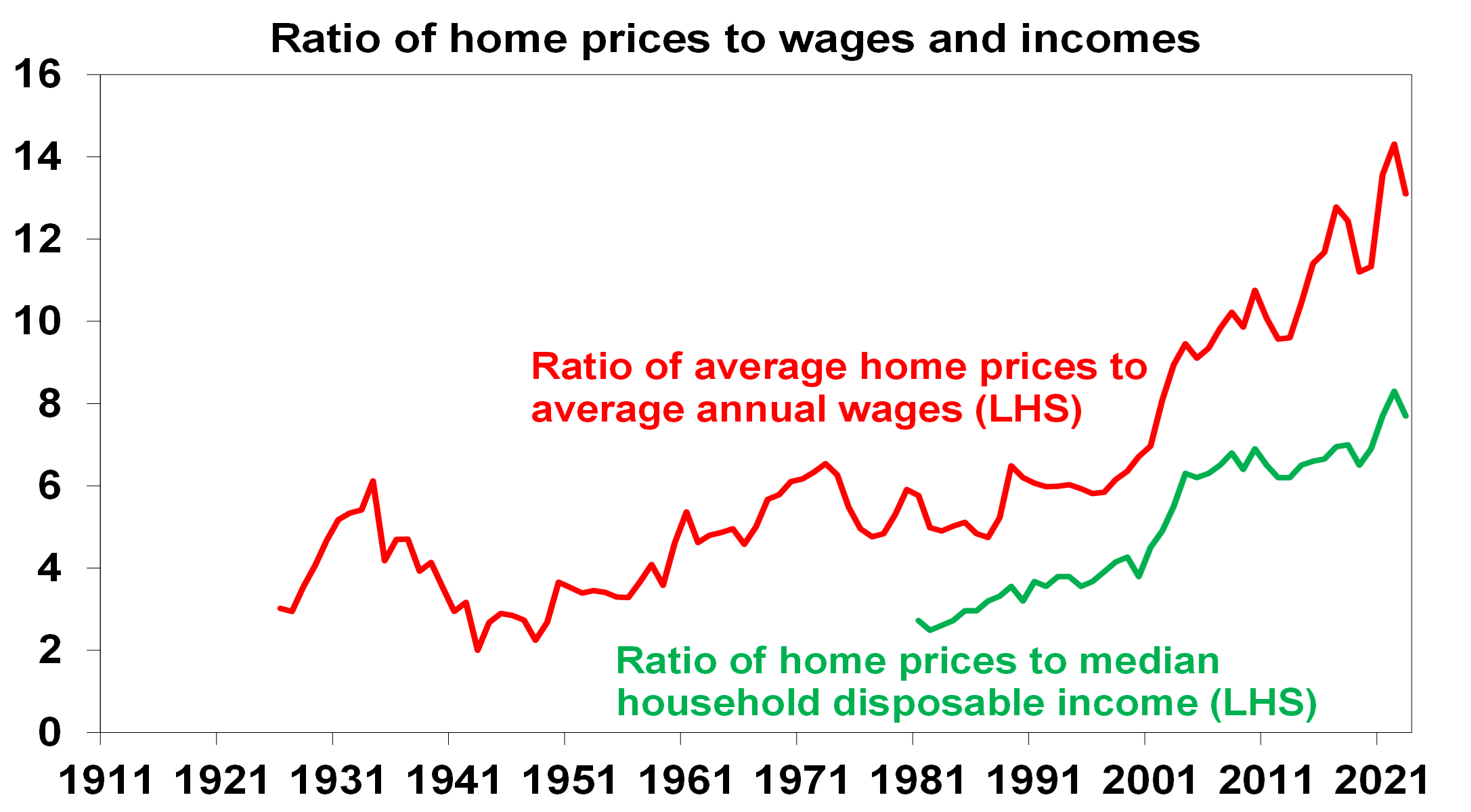

What’s not in any doubt is that housing affordability is deteriorating.

Oliver provided a great chart to illustrate:

Oliver cited the 2023 Dermographia Affordability Survey, which found the median multiple of house prices to income for major cities in Australia is 8.2 times versus about 5 times in the UK and the US.

Sydney has a median multiple of 13.3 times!

Why the level of immigration should be reduced. The attached note looks at the key drivers of poor housing affordability in Australia and particularly the role played by high immigration levels. https://t.co/jiWXtkMgKa

— Shane Oliver (@ShaneOliverAMP) September 20, 2023

Sigma Healthcare flat on half-year results

Sigma Healthcare [ASX:SIG] is flat in late trade on Wednesday after publishing its half-year results.

- 1H24 net revenue down 8.4% to $1.68 billion

- EBITDA up 77.6% to $36.7 million

- NPAT up to $11.2 million from a $1.5 million loss

How did revenue fall but profitability jump?

Sigma said 1H24 operating expenses fell 21% YoY.

As for the revenue drop, Sigma attributed it to ‘discontinued operations in the current year’ and waning sales of rapid antigen tests (RATs).

Adjusted for sales of RATs and the disposal of hospital assets, ‘wholesale sales’ were up 7.5% to $1.5 billion.

It’s interesting sales of RATs are down, considering I just bought ten after contracting COVID for the very first time.

BNPL Sezzle up nearly 20% after trading update

BNPL firm Sezzle [ASX:SZL] is up 18% in afternoon trade after an August trading update.

The buy now, pay later firm is having a better year than its peers, actually eking out a 12-month gain of 7%.

Its nearest coeval — Zip [ASX:ZIP] — is down 65% over the past 12 months.

Others, like Openpay [ASX:OPY], have collapsed entirely.

So why is Sezzle sizzling today (sorry)?

Revenue for the month of August rose 44% YoY to US$14 million and 12% month on month.

Total revenue as a percentage of underlying merchant sales (UMS) continued to rise, up 188bps YoY to 8.7%.

How is Sezzle managing to raise its take in these times?

It didn’t say.

In August, Sezzle managing to record a net profit of US$600,000, ending the month with US$60.7 million in cash on hand.

Seek: job ads fell 20.5% YoY in August

Interesting data yesterday from Seek.

Australian job ads are down 20.5% on a year ago.

And applications per job ad rose for the six straight month in August, up 6.5% from July alone.

According to @seekjobs Australian job ads fell by 1.8% in August 2023 and were 20.5% lower compared with a year ago. Applications per job ad increased for the sixth consecutive month, rising 6.5% from the month prior. #ausecon #auspol @CommSec pic.twitter.com/9XP3hbYxW4

— CommSec (@CommSec) September 18, 2023

Petrol prices hit record high

Australian petrol prices hit a record high this week — as many of us have noticed, gasping at the bowser.

Regular unleaded prices peaked at an average of $2.22 a litre.

City Index market analyst David Scutt blamed the weak Aussie dollar and the rising oil price.

As Scutt told Nine News:

‘The Aussie dollar has been very weak over the past two months.

‘At the same time, you’ve had crude oil prices and gasoline prices that have surged on the back of very tight marketplaces and the like.’

It’s even worse across the Tasman.

The New Zealand Herald reported yesterday retail petrol prices are expected to rise as much as NZ$3.50 (A$3.22) a litre for 91 octane by Christmas.

Happy holidays.

Doing my bit to support Australian inflation expectations.

Petrol prices hit record high and show no sign of coming down, motorists warned https://t.co/hXtubRBC1n

— David Scutt (@Scutty) September 20, 2023

Are most ASX stocks fairly priced?

90% of stocks are fairly priced.

At least, that’s what some buy-side analysts think.

Retired hedge fund manager Brett Caughran — who now runs Fundamental Edge — frequently points out 90% of stocks are ‘somewhat fairly priced’.

But he didn’t take this as bad news.

Because, at ‘nearly all times, at least 10% of stocks are meaningfully mispriced’.

The smart money chases those exceptions.

That’s where the alpha lies…

But how much of this is true?

Are markets really that efficient?

What if we take five stocks at random from the ASX 200 and value them? Will the valuations be similar to the market’s?

That’s what I sought to find out.

https://www.moneymorning.com.au/20230919/are-most-asx-stocks-efficiently-priced.html

Lower and sooner interest rates?

Speaking of ‘higher for longer’ interest rates.

The latest episode of What’s Not Priced In focused heavily on the topic.

For Greg Canavan, the consensus of ‘higher for longer’ may be disrupted by ‘lower and sooner’.

Is inflation re-accelerating?

Will rising oil prices push central banks to raise rates further?

Is a recession still likely?

And are markets overvalued?

As for what's not priced in? Recession continues to be a risk underpriced by the market. https://t.co/P4iiqZBRce

— Fat Tail Daily (@FatTailDaily) September 14, 2023

Lower and sooner interest rates?

Speaking of ‘higher for longer’ interest rates.

The latest episode of What’s Not Priced In focused heavily on the topic.

For Greg Canavan, the consensus of ‘higher for longer’ may be disrupted by ‘lower and sooner’.

Is inflation re-accelerating?

Will rising oil prices push central banks to raise rates further?

Is a recession still likely?

And are markets overvalued?

As for what's not priced in? Recession continues to be a risk underpriced by the market. https://t.co/P4iiqZBRce

— Fat Tail Daily (@FatTailDaily) September 14, 2023

US Treasury yields highest since 2007

Higher for longer.

That seems to be the mantra of the firming consensus.

US Treasury yields have hit a 17-year high overnight, suggesting the market is positioning for the Fed to keep rates high well into 2024.

The influential 10-Year Treasury yield reached a session high of 4.371% overnight, the highest level since November 2007.

US Treasury yields highest since 2007

Higher for longer.

That seems to be the mantra of the firming consensus.

US Treasury yields have hit a 17-year high overnight, suggesting the market is positioning for the Fed to keep rates high well into 2024.

The influential 10-Year Treasury yield reached a session high of 4.371% overnight, the highest level since November 2007.

Good morning

Good morning.

Hope everyone is well.

The market is not exactly exciting at the moment. But let’s see what’s making the news.

Good morning

Good morning.

Hope everyone is well.

The market is not exactly exciting at the moment. But let’s see what’s making the news.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988