ASX News LIVE | US CPI Stokes Rally, Tech and Lithium Stocks Soar

Will Lake Resources run out of money?

Lake Resources [ASX:LKE] was once a lithium star, now a lithium dud.

Down over 80% in the past 12 months, the stock has been rejected by the market after investors foisted big expectations on it that didn’t materialise.

But I’m not here to do a price chart rundown.

Late last month, the company released its September quarter accounts.

The cash holdings caught my eye.

Lake burnt through $35.6 million in the quarter, ending it with $60.3 million in cash and cash equivalents.

If that cash burn continues, Lake will run out of dosh in less than two quarters.

But LKE’s accounts state it has 7.5 quarters of funding left.

How come?

$206 million of unused financing on tap from Acuity Capital.

Lake entered into an at-the-market (ATM) facility with Acuity back in August 2018 and has extended it to January 2026.

This ATM facility is very interesting. As Lake says:

‘There are no requirements on the Company [Lake] to utilise the Agreement and it may terminate the Agreement at any time, without cost or penalty.’

Without cost or penalty.

What kind of deal is this?! Does Acuity have lines of firms queuing at its offices for funding?!

And how guaranteed is this deal? Can Lake really bank on securing those funds from Acuity?

Acuity gets ‘paid’ in LKE shares. In Lake’s latest annual report, published in September, Acuity was the third-largest holder, with a 4.60% stake.

What’s Acuity thinking right now? It’s funding facility of $206 million is almost LKE’s whole market cap ($240 million).

Life360 up 7% on 3Q23 results

LIfe360 [ASX:360] is up 7% in late trade after releasing 3Q23 results.

The family safety and location app — the ‘technology platform used to locate the people, pets and things that matter most to families — grew September quarter revenues 38% YoY to $78.6 million.

Despite the revenue boost, and charging core customers more, Life360 ended the quarter with a net loss of $6.5 million.

Of course, on an ‘adjusted EBITDA’ basis, Life360 made $5.5 million.

Have your say (vote) 2.0

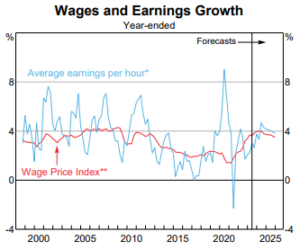

Australia's Wage Price Index rose 1.3% in the Sep Q and 4% YoY.

It was the highest quarterly growth in the 26-year history of the WPI.

YoY growth, at 4%, was the highest for the index since 2009.

Is Australia's wages growth more significant than the US CPI for #ASX stocks?

— Fat Tail Daily (@FatTailDaily) November 15, 2023

Does latest wages growth matter more than the US CPI?

Sorry, important meeting called. I’m back.

The All Ords is still up ~1.35% in late afternoon trade, down 0.5% since a midday peak.

Clearly, the latest Wage Price Index data didn’t phase the market.

But I wonder if it’ll phase the Reserve Bank.

Services inflation is the bank’s bugbear. It’s stickier than officials anticipated, forcing them to revise upwards inflation forecasts. Wages comprise much of services inflation.

So the RBA won’t receive the record wages growth in the September quarter well.

High wages growth is fine if productivity is high, too.

But Australia’s productivity is poor.

In the latest Statement, the RBA said:

‘Even so, the cost of labour for firms also depends on growth in labour productivity, which has been very weak. As a result, growth in the cost of labour is very high and is adding to firms’ overall cost pressures; the forecasts assume that productivity growth will pick up, which will be needed for labour cost growth to be consistent with the inflation target.’

But what if productivity doesn’t pick up? The RBA’s forecasts were wrong before.

The RBA expects the WPI to stabilise at ~4% before declining gradually:

‘Growth in the Wage Price Index (WPI) – which seeks to measure changes in base wage rates for a given quantity and quality of labour – is forecast to rise a little further over the second half of 2023 to stabilise at around 4 per cent before declining gradually as the labour market eases (Graph 5.9). Inertia in the wage-setting process and some lagged catch-up in real wages mean that the decline in [nominal] wages growth is forecast to be slower than the decline in inflation.’

Australia’s wages growth highest in at least 26 years

US inflation is cooling.

But Aussie wages aren’t.

The Wage Price Index rose 1.3% in the September quarter and 4% for the year. The ABS said it was the highest quarterly growth in the 26-year history of the WPI.

The annual growth, at 4%, was the highest for the index since the March quarter in 2009.

What will the market think of that?

Hardly good news, considering the RBA was taken aback by sticky services inflation, of which wages are a huge part.

Have your say (vote)

Is the rally in stocks stoked by better than expected US CPI data justified?

Or will it be short-lived? #SP500 #ASX #NASDAQ

— Fat Tail Daily (@FatTailDaily) November 15, 2023

US bond yields fall the most since Silicon Valley Bank collapse in March

The US CPI print sent bond yields lower.

Sharply lower. The benchmark US 10-Year note fell 0.191% to 4.440% overnight.

The last time US bond yields fell this much was the collapse of Silicon Valley Bank in March.

But are the two events really that comparable in their impact or implication?

The latest inflation report was good, for sure.

But is it really feasible that one monthly report on one indicator is enough to knock expected interest rates over the next *decade* down by one-sixth of a percentage point?https://t.co/axFn95rpO1

— Justin Wolfers (@JustinWolfers) November 14, 2023

Market eggheads offer their take

How did the market boffins react to the inflation data? Here’s a sample.

JPMorgan’s Jamie Dimon:

“Personally I think people overreacted to short-term numbers and they should stop doing that. I’m afraid inflation may not go away that quickly.”

Goldman Sachs’ chief US economist David Mericle:

“The hard part of the inflation fight now looks over.”

PGIM Fixed Income’s chief global economist Daleep Singh:

“Considering the scars left by the inflation spike, there’s little to be gained and much to lose by declaring the end of the tightening cycle. But the reality is they are very likely done with rate hikes.”

ARK Investment’s Cathie Wood:

“The Federal Reserve has overdone it, we’re going to see a lot more deflation going forward. If we’re right, and they’ve gone way too far, they’ll have to cut fairly significantly.”

Fed unlikely to hike ‘but not a slam dunk’ yet

The latest US inflation data is raising hopes the most important central bank in the world is done hiking.

But there’s another inflation report before the year ends.

If it’s anything like yesterday’s, the market will bet the Fed’s hiking days are behind it.

Today's low inflation reading definitely reduces (a lot!) the chances of the Fed raising rates at its next meeting. It's not a slam dunk though, because there's one more inflation report (Dec 12) that arrives before its next meeting.

— Justin Wolfers (@JustinWolfers) November 14, 2023

Not out of the woods yet

Jason Furman, a prominent US economist, said the latest US inflation data was a ‘pleasant surprise’.

Headline inflation — often reported first in headlines — was a fat zero in October.

The more telling core inflation — excluding jumpy items like food and energy — was an annualised 2.8% in October. Lower than expected!

But…

Core inflation is still above the Fed’s target over the last three, six, and twelve months.

The CPI data was a pleasant surprise. Headline was 0 inflation in October, which happened because volatile gasoline fell 5%. More important, core CPI (excluding food and energy) was 2.8% annualized in October, lower than expected.

Not out of woods: still 3%+ over 3/6/12 months. pic.twitter.com/244tPm10jQ

— Jason Furman (@jasonfurman) November 14, 2023

Hooray?

Good morning. It’s Kiryll!

The market is moving today.

Let’s all rejoice? Is this the start of a bull market?

You’d think that from some of the commentary.

But how relieved (or exuberant) should we be following the better than expected US inflation data overnight?

Let’s delve on that today.

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988