ASX News Live | Aussie CPI Hotter Than Expected at 7.8% as Earnings Season Kicks Into Gear

Hindenburg Research publishes short report on Indian conglomerate Adani Group

“In this report, we highlight what we believe to be one of, if not the most egregious examples of corporate fraud in history.

“We have uncovered evidence of brazen accounting fraud, stock manipulation and money laundering at Adani, taking place over the course of decades. Adani has pulled off this gargantuan feat with the help of enablers in government and a cottage industry of international companies that facilitate these activities.

“These issues of corruption permeate multiple layers of government. According to numerous sources we spoke with, Indian securities regulator SEBI seems more inclined to protect the perpetrators than punish them.”

Today we reveal the findings of our 2-year investigation, presenting evidence that the INR 17.8 trillion (U.S. $218 billion) Indian conglomerate Adani Group has engaged in a brazen stock manipulation and accounting fraud scheme over the course of decades. (2/x)

— Hindenburg Research (@HindenburgRes) January 25, 2023

Jeremy Grantham: stocks can fall 20% further from here

Jeremy Grantham, co-founder of investment firm GMO, argued in his latest research note that the first stage of the bubble has passed but markets have more pain in store.

Grantham likes to call out irrational exuberance as he sees it, making his name by calling bubbles.

In his latest note After a Timeout, Back to the Meat Grinder, Mr Bubble predicted the S&P 500 to fall 20% from current levels by the end of 2023.

“My calculations of trendline value of the S&P 500, adjusted upwards for trendline growth and for expected inflation, is about 3200 by the end of 2023. I believe it is likely (3 to 1) to reach that trend and spend at least some time below it this year or next. Not the end of the world but compared to the Goldilocks pattern of the last 20 years, pretty brutal. And several other strategists now have similar numbers. To spell it out, 3200 would be a decline of just 16.7% for 2023 and with 4% inflation assumed for the year would total a 20% real decline for 2023 – or 40% real from the beginning of 2022. A modest overrun past 3200 would take this entire decline to, say, 45% to 50%, a little less bad than the usual decline of 50% or more from previous similarly extreme levels.”

How Australia’s fintelligentsia reacted to the CPI print

Australia’s financial community — the fintelligentsia — has passed judgement on the latest inflation data.

Macroeconomist Warren Hogan labelled the CPI print ‘absolutely shocking’ and a ‘sad day for the Australian economy’.

Absolutely shocking set of inflation numbers just released in Australia. Housing and food up almost 10% over the year. Broad measure of non discretionary items up 8.4%. Major policy failure that can only be fixed with unpopular policy decisions. Sad day for the Australian economy

— Warren Hogan (@_warrenhogan) January 25, 2023

Stephen Koukoulas, former economic advisor to the Gillard government, was more upbeat, calling for ‘the more excitable folk’ to relax.

In August 2022, RBA was forecasting year end CPI to be 7.8%.

In November, this was revised to 8.0% even with hikes of 125bps in total in Sep, Oct, Nov & then Dec.

I suggest the more excitable folk have a bex, a cup of tea & a good lie down.

The RBA has called it brilliantly.— Stephen Koukoulas (@TheKouk) January 25, 2023

AMP’s chief economist Shane Oliver was more reserved, arguing inflation has likely peaked but that the RBA will be compelled to pass another 25 basis point hike in February.

Inflation has likely now peaked. However,even tho the CPI rise was < the RBA’s exp for +8%yoy, the rise in trimmed mean infl to 6.9%yoy will concern the RBA. As such its likely the Dec qtr CPI plus still strong retail sales will now tip the RBA over into another 0.25% hike in Feb

— Shane Oliver (@ShaneOliverAMP) January 25, 2023

Chief economist at IFM investors Alex Joiner concurred, saying another 25 basis point hike in February ‘now seems assured’.

Material upside surprise for AU CPI, with both headline and trimmed mean measures coming in above the market's and/or RBA's expectations. Another 25bp move in Feb now seems assured. pic.twitter.com/MHouYNGlqd

— Alex Joiner 🇦🇺 (@IFM_Economist) January 25, 2023

Joiner also spared an economist’s thought for the hip pockets of those planning to have a BBQ tomorrow.

If you happen to be having an Australia Day BBQ tomorrow inflation is hitting you pretty hard. pic.twitter.com/2VkuhXgaRb

— Alex Joiner 🇦🇺 (@IFM_Economist) January 25, 2023

The race to cheaper energy

Manufacturing, bringing supply chains closer to home, onshoring, nearshoring…for all this, you need cheap electricity to be competitive.

At the moment, manufacturers are struggling with high energy costs. At the same time, renewables have become the cheapest forms of power today.

So the global competition is on to shift into the cheapest source of energy out there.

And going back to Credit Suisse’s report, the bank expects investment from the IRA could give the US a leg up when it comes to cheaper electricity.

As a piece in The Atlantic states:

‘The U.S. is “poised to become the world’s leading energy provider,” according to the bank. America is already the world’s largest producer of oil and natural gas. The IRA could further enhance its advantage in all forms of energy production, giving it a “competitive advantage in low-cost clean electricity and hydrogen production, infrastructure, geologic storage, and human capital,” the report states. By 2029, U.S. solar and wind could be the cheapest in the world at less than $5 per megawatt-hour, the bank projects; it will also become competitive in hydrogen, carbon capture and storage, and wind turbines.’

So while much of the reasoning for the energy transition has been touted as being for the climate, it’s also about energy security and having access to cheap electricity as countries bring more manufacturing onshore.

This is a megatrend that will continue to play, in particular into commodities.

https://www.moneymorning.com.au/20230125/the-race-to-cheaper-energy.html

Simandou: Iron ore’s Amazon moment

Everybody loves to talk about battery minerals, but iron ore is still where the big money is.

The same month, we have the price going back to more than US$120 a tonne, we also find China pushing deeper into Africa.

The Australian Financial Review reports that the fabled Simandou project in the West African country of Guinea could be a lot closer to fruition than previously presupposed.

Simandou has hung over the iron ore market for years, something akin to the Spanish gold dream of El Dorado.

In this case, it’s not that the Chinese can’t find it, it’s just getting the Simandou ore to port that’s difficult.

The Simandou deposit is 550 kilometres from the coast. And as yet there are no rail lines, bridges, or tunnels to get it there.

The Chinese look set to flex their muscles, at least in terms of money, to build the necessary infrastructure.

Whether Guinea can stay stable and clean to allow the project to start shipping iron ore out by 2025 remains to be seen.

Generally, Aussie investors view Simandou the same way they did Amazon before its arrival here in Australia: with suspicion it’s coming to wreck the party for the incumbents.

I’m not so sure. It’s possible the world needs major investment into the iron ore industry to keep it well supplied.

Here’s a chart I shared with my paid readers in their last monthly report. It shows the major drop off in iron ore capital spending over the last 10 years:

Source: Champion Iron

Granted, Simandou is not an Australian project.

But the fact that the Chinese are so willing to fund this suggests iron ore demand could stay robust for the next five years and potentially beyond. That’s a good sign for Australia.

And as stated above, iron ore is back to a booming price of US$120 a tonne.

The profits are huge for BHP, Fortescue, and Rio Tinto at this price. And they make a big proportion of index weighting…hence why the ASX is back very close to all-time highs.

Here’s another thing…both Rio Tinto and BHP released their quarterly production reports this month. Both are running at full speed to basically match what they did last year.

Point being: Everybody is always worried that the iron ore market will go into oversupply and kill the price.

There’s another scenario worth thinking about: that demand for iron ore keeps pressing ahead and the Aussie miners are already too stretched to lift production.

https://www.dailyreckoning.com.au/simandou-iron-ores-amazon-moment/2023/01/23/

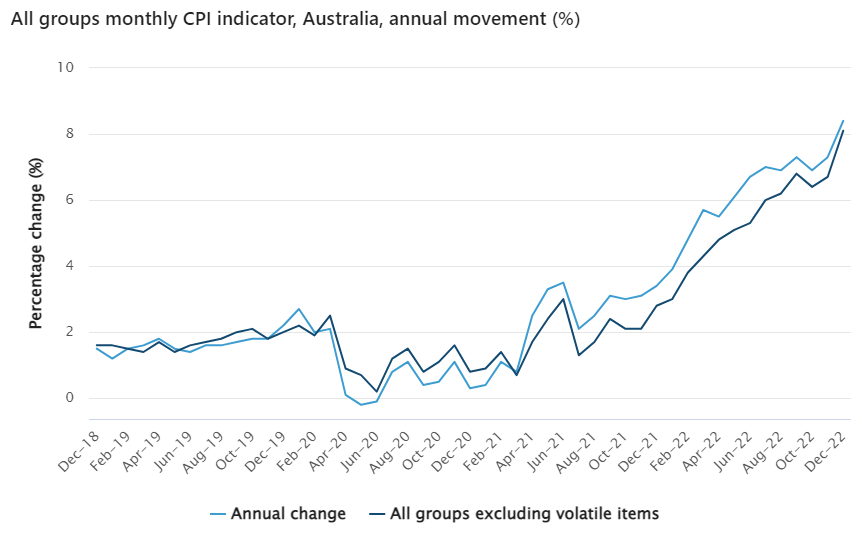

Monthly CPI rose 8.4% on the back of a 29.3% rise in holiday travel and accommodation

The December quarter inflation data is pretty grim. The monthly CPI data isn’t any better.

The monthly CPI rose 8.4% in the 12 months to December, up from 7.3% in November and 6.9% in October. It was the highest annual movement since the start of the monthly indicator series.

The annual movement for the monthly CPI excluding volatile items rose a whopping 8.1%.

One of the biggest contributors to the December monthly CPI was holiday travel and accommodation, which rose a whole 29.3% in the year to December, up from 12.8% in November.

“Increased demand during the Christmas holiday period contributed to prices rises for both Domestic holiday travel and accommodation and International holiday travel and accommodation. December saw the largest annual and monthly increase for Holiday travel and accommodation since the series began in 2018,” the ABS release said.

Source: ABS

ASX falls 0.55% on CPI print

The All Ords fell 0.55% immediately after the December quarter CPI print, which came in much hotter than expected.

Trimmed mean inflation — the key inflation measure monitored by the Reserve Bank of Australia — rose to the highest level since the measure was introduced by the ABS in 2003.

Annual trimmed mean inflation reached 6.9% in the December quarter, up substantially from 6.1% recorded in the September quarter.

Source: ABS

Australia’s headline inflation hotter than forecast

Australia’s Consumer Price Index (CPI) rose 1.9% in the December 2022 quarter and 7.8% annually. Crucially, annual trimmed mean inflation was the highest since 2003, rising 6.9% from 6.1% in the September quarter.

Michelle Marquardt, ABS head of prices statistics, said:

“This is the fourth consecutive quarter to show a rise greater than any seen since the introduction of the Goods and Services Tax (GST) in 2000. The increase for the quarter was slightly higher than the quarterly movements for the September and June quarters last year (both 1.8 per cent).”

Australia's #CPI rose 1.9% in the December 2022 quarter and 7.8% annually, coming in hotter than consensus forecasts. #inflation #auspol https://t.co/uyRR7x3spE

— Fat Tail Daily (@FatTailDaily) January 25, 2023

From the ABS:

The most significant contributors to the rise in the December quarter were Domestic holiday travel and accommodation (+13.3 per cent), Electricity (+8.6 per cent), and International holiday travel and accommodation (+7.6 per cent).

“Strong demand, particularly over the Christmas holiday period, contributed to price rises for domestic holiday travel and international airfares,” Ms Marquardt said.

“The rises seen for domestic and international travel were notably higher than historical December quarter movements.”

“The main factor influencing the rise in electricity prices was the unwinding of the $400 electricity credit offered by the Western Australian Government to all households last quarter. This was partially offset by the ongoing impact of the Queensland Government’s $175 Cost of Living rebate from September 2022, and the introduction of the Tasmanian Government’s $119 Winter Bill Buster electricity discount for concession households.”

Growth in prices for New dwellings (+1.7 per cent) slowed relative to recent quarters (+3.7 per cent in September and +5.6 per cent in June) but remained stronger than historic norms.

“Labour and material costs are driving price growth in this area, with signs of material cost pressures easing,” Ms Marquardt said.

“Slowing demand for new dwelling construction was reflected in a lower quarterly rate of inflation for new dwellings this quarter compared with the past five quarters”.

Food prices continued to rise, driven by Meals out and takeaway foods (+2.1 per cent) as dining establishments pass through rising costs for inputs including ingredients and labour. Vegetables (-10.2 per cent) partially offset the rise, as the effects of unfavourable weather earlier in the year eased.

Material upside surprise for AU CPI, with both headline and trimmed mean measures coming in above the market's and/or RBA's expectations. Another 25bp move in Feb now seems assured. pic.twitter.com/MHouYNGlqd

— Alex Joiner 🇦🇺 (@IFM_Economist) January 25, 2023

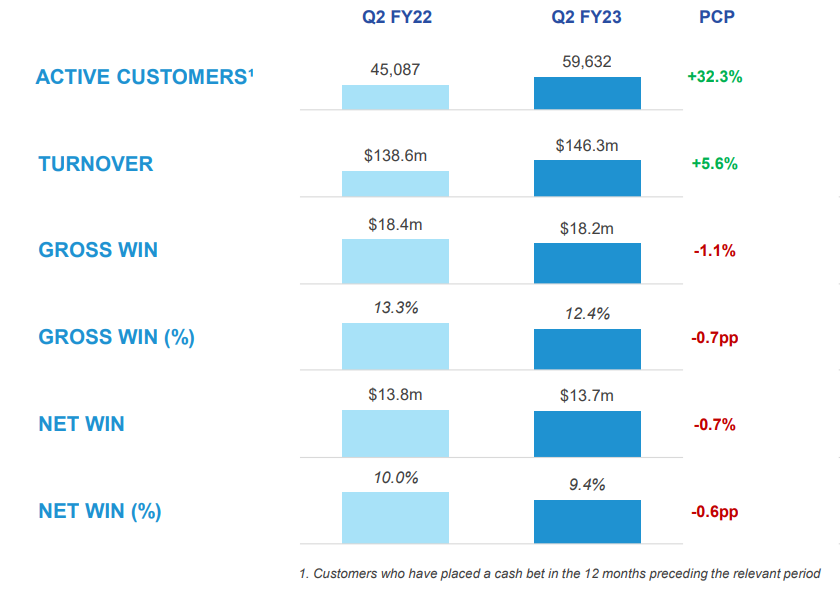

BlueBet up on Q2 FY23 results

Online bookmaker BlueBet (ASX:BBT) said it continues to gain share in Australia while ‘making progress’ in the key US market.

Wagering turnover rose 6.6% to $147.7 million on the prior corresponding quarter as the bet count hit 3 million, up 9.9%.

However, while turnover rose 6.6%, active customers rose a much larger 32.3% to 59,632, despite BBT’s net win barely budging.

BlueBet’s net win remained unmoved at $13.7 million but the net win percentage fell from 10% to 9.4%. As BlueBet explained in its prospectus:

“BlueBet generates Turnover when a customer puts a stake (money) at risk through placing a bet on an event. BlueBet’s Gross Win is the dollar amount received from customers who placed losing bets less the dollar amount paid to customers who placed winning bets. Net Win is equal to Gross Win less customer promotional costs.”

Source: BlueBet

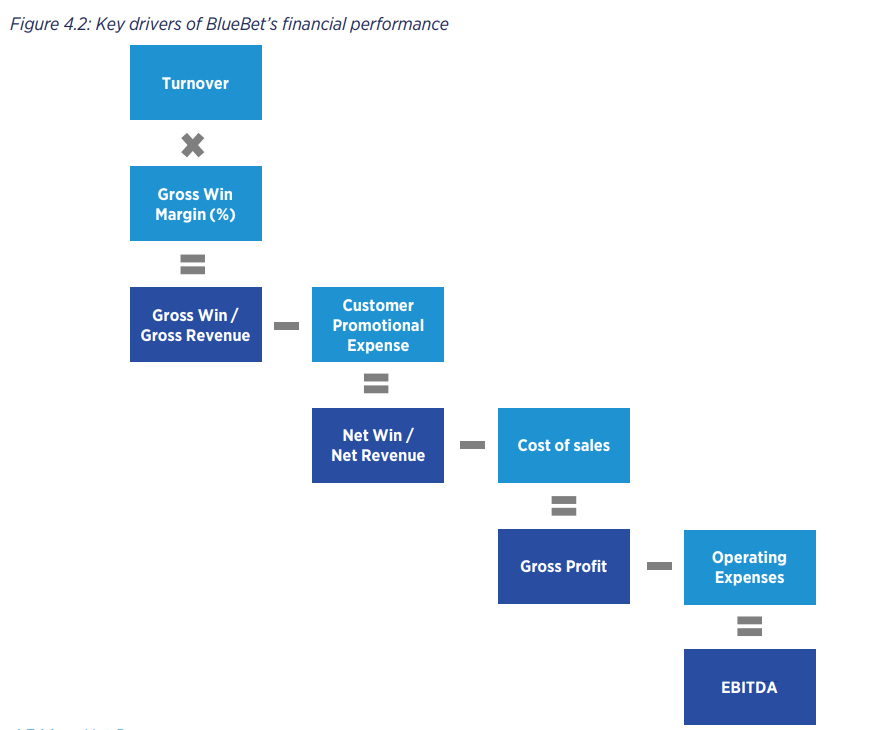

By the way, this is how BlueBet classified the key drivers for its financial performance.

Will Australia follow New Zealand with inflation surprising to the upside?

New Zealand’s headline inflation rose 1.4% in the December quarter, slightly ahead of the forecasted 1.3%. On an annual basis, New Zealand’s CPI grew 7.2%, versus the expected 7.1%.

Will Australia’s CPI print likewise surprise to the upside?

Consensus forecasts have Australia’s headline inflation hitting 7.5% year on year in the December quarter, with trimmed mean inflation reaching 6.5%.

Westpac’s chief economist Bill Evans thinks inflation should ‘ease substantially in both Australia and the US in 2023.’

“Inflation is expected to ease substantially in both Australia and the US in 2023. Supply issues, which represent global pressures, associated with housing; goods; food; and fuel will all generate downward pressure on inflation. However, the key services inflation cycle looks to be ahead for Australia while it is slowing in the US. Wage inflation in Australia is still lifting as labour markets remain tight through the first half of the year. Headline inflation in Australia will also be held up in 2023 by rising gas and electricity prices. The high starting point for inflation and initially slow progress should mean that both the Federal Reserve and RBA have more work to do before remaining on hold in the second half of 2023.”

Dusk CEO Peter King resigns

Candle and diffuser retailer Dusl (ASX:DSK) is down over 3% after announcing the resignation of CEO and managing director Peter King.

King was at the helm for almost nine years but believes now — with macroeconomic clouds ahead — is the ‘right time for someone else to take the company forward.’

Chairman John Joyce said:

“The Board would like to thank Peter for the invaluable contribution he has made since 2014. The Company has been transformed under his leadership. Peter has built an outstanding executive team, dramatically grown our revenues and earnings, driven the omnichannel transformation strategy, and led the IPO in 2020. He will leave the business in excellent shape.”

Dusk is set to release its 1H23 results on 24 February.

Over the last 12 months, Dusk is down 20%.

Home fragrance retailer $DSK is down over 3% after CEO and managing director Peter King resigned.

King was at the helm for 9 years but believes now — with macroeconomic clouds ahead — is the ‘right time for someone else to take the company forward.’#ASX #Dusk

— Fat Tail Daily (@FatTailDaily) January 24, 2023

BNPL fintech Laybuy announces voluntary delisting

The crowded Australian buy now, pay later scene has its first casualty.

Small BNPL fintech Laybuy (ASX:LBY) wants out of the public markets — submitting a formal request to the ASX to be removed from the official list.

The delisting already has in-principle approval from the ASX but must be put forward for shareholder approval at a special meeting to be held late next month.

The #ASX may soon say goodbye to #BNPL fintech $LBY, who announced a voluntary delisting.

Laybuy cited several reasons, chief among them the market's 'undervaluation' of the stock. pic.twitter.com/0m4ervTFpS

— Fat Tail Daily (@FatTailDaily) January 24, 2023

Laybuy’s management thinks the stock is being persistently undervalued by public markets, causing a cascade of problems.

LBY’s low valuation — unfair in managmenet’s estimation — means the company cannot raise funds without significant dilution to shareholders. Capital raising themselves are proving difficult and impractical:

“The composition of the Company’s share register combined with low market capitalisation, a low trading price and resulting low liquidity have made it difficult for the Company to seek to raise public capital and attract broader institutional ownership. If the Company was able to raise further capital whilst listed on ASX (either now or in the short to medium term), this would likely impose a higher dilutionary cost on non-participating shareholders than if the Company was more fairly valued.”

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988