ASX News Live | ASX Up; Zip Sinks, Myer Spikes, Spotify Lays Off Staff

Myer records best sales on record

March 2020 was a low point for many. But Myer’s nadir may have been one of the deepest.

Already a floundering public company with its best years seemingly behind it, Myer’s stock price cratered to around 10 cents a share.

10 years back, in March 2010, Myer was trading for about $3.10 a share. In that decade, Myer shed 95% of its value.

But the retailer is turning things around and embracing online.

Since the March 2020 low, the stock is up nearly 800%.

In March 2020, $MYR hit its nadir, trading for ~10 cents a share.

10 years before, #Myer was trading for ~$3.10. In that decade, $MYR shed 95% of its value.

But the retailer is turning things around.

Since the March 2020 low, the stock is up nearly 800%. #ASX pic.twitter.com/wgERdafGHj

— Fat Tail Daily (@FatTailDaily) January 24, 2023

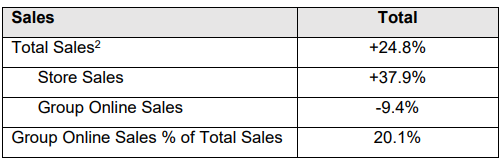

Things are looking up once more, with Myer reporting its ‘ best sales on record for the first five months’ of a financial year. Its financial records go back to FY04.

In 1H23, Myer’s total sales rose 24.8%, driven by a 37.9% increase in store sales as online sales actually fell 9.4% on 1H22 with shoppers choosing brick and mortar experiences.

Total sales were up 18.9% on 1H20 — the most recent period unaffected by COVID-19 disruption.

Myer now expects its 1H23 NPAT to be between $61 and $66 million, up between 54% and 67% on 1H20.

But markets are ruthless; past performance matters little to the future-facing discounting machine. Will Myer’s strong sales hold up in a recession or declining macroeconomic conditions?

Myer CEO John King addressed this concern by saying the department store will remain vigilant:

“As with most retailers, we remain cautious on the macroeconomic environment for the remainder of the calendar year but are equally confident in the continuing momentum we have within the Customer First Plan and a range of initiatives we are executing.”

Extract: the short-term effect of liquidity flows on stock prices

Exclusive extract from Fat Tail Investment Research editorial director Greg Canavan‘s latest research note.

The US economy is all but in recession, the Fed is still on a tightening path, as is the RBA, and the Aussie market is approaching all-time highs!

What’s driving the market higher, then?

Why, if growth is about to reverse in the world’s largest economy (and corporate earnings with it), are stocks continuing to march higher?

Well, obviously, the China reopening story is benefiting sentiment, particularly in Australia. But there’s a liquidity angle to all this that’s important to understand.

The liquidity story — what is it and where does it come from

It’s important to understand that the market and the economy are hardly ever in sync. The market moves ahead of the economy. And the market is also influenced by short-term liquidity flows.

And it’s this topic of market liquidity that we need to look into now because it explains the recent movements in the S&P 500 nicely and will give us some clues about what comes next.

Let’s take a look…

Let’s start with QE, or ‘quantitative easing’. This is how the Fed provides monetary stimulus when the interest rate they control — the fed funds rate — is already at zero.

They do this by buying assets like US Treasury bonds and mortgage-backed securities in return for ‘fed funds’, which the Fed simply creates out of thin air. These funds, akin to cash, circulate in the financial system (but not the real economy). They lead to an inflation of asset prices but not inflation in goods and services.

Fed balance sheet

The assets the Fed buys go onto its balance sheet as an asset, while the Fed Funds created and injected into the banking system are the corresponding liability. The Fed’s balance sheet size is therefore a good barometer of the extent of QE.

QE was in effect from roughly 2008–15. During that time, the Fed’s balance sheet went from around US$900 billion to US$4.5 trillion. It was a very good time for risk assets in general. Most asset prices went up.

The balance sheet then stabilised for a few years before the Fed introduced the policy of QT (balance sheet shrinkage) during 2018 and 2019.

It managed to reduce its assets by around US$740 billion before it had to turn around and start buying assets again. It’s hard to cut the addict off from its sugar hit.

This was well before COVID hit too.

In January 2020, the Fed’s balance sheet was US$4.15 trillion. Then came the COVID response. Six months later, it was US$7.16 trillion. It peaked in April 2022 at US$8.965 trillion.

It had more than doubled in just over two years.

The 2020–22 increase is a huge amount of liquidity to inject into the market in a short space of time. It’s why there was such a speculative boom in US assets markets especially.

Treasury General Account

The post-2020 environment is a bit like the post-2008 environment in that the game has changed. The old rules don’t apply.

You can’t just look at the Fed’s balance sheet as a broad measure of financial liquidity.

COVID saw fiscal policy play a major role in getting money into the real economy.

It was only when governments started to run massive emergency deficits, financed directly by the Fed, that inflation got out of control.

This brings me to the ‘Treasury General Account’, or the TGA. When the Treasury, AKA the US Government, needs funds, it issues Treasury securities in exchange for cash. Before spending the proceeds, it parks this cash at the Fed in the TGA.

In 2020, it did this on a massive scale. As you can see in the chart below, the TGA went from a balance of around US$400 billion in January 2020 to a peak of US$1.8 trillion in July.

In effect, the US Government was taking cash out of the market at the same time as the Fed was putting it in:

Source: St Louis Fed

But that was only while the government worked out its spending programs. The TGA soon began to fall sharply as the government spent that US$1.8 trillion into the real economy. Note the sharp decline in the TGA occurred in 2021, which was the height of the speculative fervour in the US.

The point to note is that a rising TGA has a negative impact on overall liquidity, while a falling TGA injects liquidity.

Reverse repos

Now for the final piece in the overall liquidity puzzle — reverse repurchase agreements, or ‘repos’.

All you need to know is that they’re a way for the Fed to absorb some of the excess liquidity they created in response to COVID.

Remember, the Fed’s balance sheet exploded from around US$4 trillion to nearly US$9 trillion in two years. That’s a huge amount of liquidity. They needed to absorb some of it.

They did this (and continue to do so) via the reverse repo facility. It’s basically the Fed swapping a treasury security for fed funds, which removes liquidity from the market.

The liquidity equation

Now, let’s put it all together to get a sense of the real net liquidity picture.

Here’s the equation:

Net liquidity = the size of the Fed’s balance sheet — TGA balance — reverse repo balance

And how does this equation correlate with the S&P 500? As you can see below, it’s a decent fit:

Source: Fidelity

So while the Fed continues its policy of QT to the tune of US$95 billion per month, that’s not the only game in town. Movements in the other two accounts can have a greater or lesser effect on overall liquidity.

For example, since topping out in May around US$950 billion, the TGA has declined to a current level of US$370 million. That’s a US$580 liquidity injection, or more than six months’ worth of QT.

But as the chart shows, while there are ups and downs, over the past 12 months, net liquidity has declined. I expect this trend to continue.

Net liquidity is in a declining trend…

M2 (a proxy for US money supply to the real economy) is about to turn negative year-on-year for the first time ever…

A recession is coming. But the market is pricing in a soft landing and still positive earnings growth this year. In a recession, corporate earnings per share usually contract by 20%.

And finally, it’s only a matter of time before the Fed starts talking tough on interest rates again. Its next board meeting starting on 31 January would be a good place to start.

ASX stocks join global market rally

Do you get the sense the markets are regaining their euphoria?

The S&P/ASX 200 is up 7.4% so far in January alone, hitting a nine-month high.

Since 3 October 2022, the ASX 200 has been up 15%.

If we were to be a bit cheeky, we could say the ASX is running on annualised gains of about 88%.

Clearly absurd, but it does highlight the recent price action.

The animal spirits aren’t just animating the ASX.

Last week, European shares also hit a nine-month high, a pattern across global markets.

US equities — often bolstered by their pacy tech stocks — are underperforming the rest of the world.

Source: Financial Times

In fact, it’s Chinese tech stocks leading the way. They have staged a remarkable US$700 billion rally upon China’s reopening.

Hong Kong’s Hang Seng TECH Index is up 60% from last October’s lows.

Source: Financial Times

The weakening of the US dollar, the easing of inflationary pressures, and China’s loosening of COVID-19 restrictions are helping markets stage a recovery.

But is this a rational recovery or irrational exuberance? Are animal spirits back?

https://www.moneymorning.com.au/20230124/asx-stocks-join-global-market-rally.html

How have 2022’s worst performing ASX stocks started 2023?

Recently, I’ve haphazardly noticed some big jumps in stocks heavily beaten down last year.

I wanted to know how wide the phenomenon was, so I turned to last year’s 10 worst-performing ASX stocks of 2022.

How are these stocks faring since?

Eight of the 10 have started the year in the black, with battery stock Novonix [ASX:NVX], software firm FINEOS [ASX:FCL], and BNPL fintech Zip Co [ASX:ZIP] the standouts.

Zip’s performance has since been dented by the release of its 2Q23 results, showing a decline US active customers.

Zip’s customer growth stalls, US customers decline

Zip talked up the performance of its US arm, which was cash EBTDA positive in the last two months of 2022. Zip US is now expected to exit FY23 cash EBTDA positive.

But not all is well with its key market.

Zip’s total active customers have not budged since the last quarter and actually fell 1% year on year.

$ZIP's reporting of active customers is all over the place.

In 1Q23, $ZIP distinguished between total customers and active customers.

The former are all who have a live account. The latter have transacted in the last 12 months. https://t.co/fpqcHQtH9B pic.twitter.com/JMH0DY1mJd

— Fat Tail Daily (@FatTailDaily) January 24, 2023

US active customers, however, fell 7% year on year to 4 million.

ANZ active customers rose 5% to 2.3 million.

BNPL $ZIP talked up the performance of its US segment, expecting Zip US to exit FY23 cash EBTDA positive.

But not all was well with its key market. $ZIP's US active customers fell 7% YoY despite rise 3% QoQ. #ASX #BNPL pic.twitter.com/CrRwpHXMgk

— Fat Tail Daily (@FatTailDaily) January 24, 2023

Zip touts revenue growth

Buy now, pay later fintech Zip (ASX:ZIP) said it was ‘on target’ in its 2Q23 update. Zip mentioned that it hit record quarterly revenue of $188 million (up 12% YoY) on record transaction volume of $2.7 billion.

The fintech’s cash transaction margin rose to 2.6% for the quarter, a ‘great result in a rising interest rate environment’.

Zip said its key growth engine — the US market — performed strongly. Its US business was cash EBTDA positive in November and December. Zip US is now on track ‘to exit FY23 cash EBTDA positive on a sustainable basis.’

That expected sustainability is important as Zip has $78.5 million available in cash and liquidity as of the end of December 2022.

The company thinks the &78.5 million is ‘sufficient reserves to support [it] through to cash EBTDA profitability.’

ZIP shares are up 55% since late December but are still down 75% over the last 12 months.

UBS upgrades lithium outlook

UBS expects lithium to remain in a physical deficit for the near-to-medium term and has upgraded its price forecasts for lithium chemicals by up to 50%.

Lachlan Shaw, UBS analyst, said:

“We believe lithium markets will remain in deficit for the near and medium term before moving to structural deficit long term. This needs a demand rationing price, for which we have seen no evidence in the past 12 months despite record-high prices that are orders of magnitude above costs.”

Big updates of the day as ASX stocks begin to release December quarterlies

Which companies have announced important updates today?

- Sandfire Resources released its December 2022 quarterly report, with operations ‘continuing to deliver strong margins’ but copper production coming ‘below budget’ for the quarter

- Selfwealth released its 2Q23 update, reporting ‘record revenue’ of $7.8 million despite weaker customer trading activity in Q2. Revenue was boosted by increase in bet interest of $1.1 million from Q1.

- Myer released a half-year trading update, showing total sales rose 24.8% on prior corresponding period. Store sales surged 37.9% while online sales declined 9.4% as customers returned to brick and mortar stores.

- Zip released its 2Q23 trading update. Despite record transaction volume of $2.7 billion, up 22% quarter on quarter, it rose only 4% year on year, suggesting Zip’s growth is maturing. Transactions, also, only rose 1% YoY to 22.6 million.

- Codan released its 1H23 trading update, showing revenue came in at the top end of guidance and net profit after tax likely to exceed guidance.

Morning market summary

Good morning!

Here’s a quick summary of what went down overnight as we start another day on the ASX.

- US stocks finished higher overnight, with the Nasdaq finishing 2% higher. Markets worldwide are continuing their strong start to 2023 on bets the worst is likely behind us.

- Big earnings week coming up for US companies, with Microsoft, Tesla, Mastercard and Visa set to release results.

- Microsoft recently announced significant staff cuts and Tesla slashed prices for some of its EV models so it will be interesting to see how these giants perform and how the market reacts. Will corporate earnings remain resilient in spite of the inflationary pressures?

- Interestingly, despite Microsoft culling a chunk of its workforce, it is going ahead with a further investment in OpenAI, creator of ChatGPT.

- And about ChatGPT, Bill Gates has warned generative AI could be a threat to white collar jobs:

- “As you make a doctor’s job more efficient [with AI tools] it doesn’t mean you need less doctors, but there are some areas where things change, for example when radial tyres were invented, people didn’t drive more, so we have less tyre factories. Over time that labour went off and did other jobs, but now there will be a lot of angst about the fact that AI is targeting white-collar work.”

- Spotify joined Big Tech in announcing layoffs. The music and podcasting streaming platform will cut ~6% of its workforce, blaming macroeconomic conditions.

- The US Fed is meeting next Wednesday and the markets are heavily predicting a 25 basis point interest rate increase.

- According to CME’s Fedwatch, the market is placing a 99.8% probability on a 25 basis point hike.

- The Wall Street Journal reported that markets are projecting inflation will fall as fast as it has done only three times in the last 75 years.

Source: OpenAI’s Dall.E

Speaking of OpenAI, here’s an image created by OpenAI’s image generator Dall.E. The prompt was, ‘A watercolour painting of a stack of newspapers with a steaming cup of coffee and a fountain pen nearby.’

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988