ASX News LIVE | ASX Up, S&P 500 Notches 3-Month Losing Streak, Novonix and Regal Jump

Domino’s sales rise in first weeks of FY24

In a trading update during its AGM, Domino’s Pizza said network sales rose 12.7% in the first weeks of FY24 compared to the same time last fiscal year.

Same store sales were up 2.7% on FY23.

Same store sales in Asia were down nearly 7% but up 7% in Australia & New Zealand and up 3.8% in Europe.

While Europe’s FY24 year-to-date sales pleased management, France underperformed expectations.

Domino’s management said France is ‘yet to achieve the same momentum as the other larger markets and we are applying a high level of focus to this market’.

The pizza merchant does not expect any changes to its previous earnings forecast.

While earnings in 1H24 are expected to be ‘materially higher’ than 2H23, the ‘full year over year growth will be delivered’ in 2H24.

Sometimes I like to parse company earnings calls to glean insights about business models. DMP’s FY23 earnings call had this gem from chief executive Donald Meij:

‘Our business has always been about a high-volume mentality. It’s the leverage through more order count growth that our franchise partners win, and we ultimately win if they’re winning. And we — and that’s where we lost it last year. We lost order counts. You can’t make more money out of less customers, and that created a lot of pain in the business.’

Novonix up on US$100 million grant finalisation

Battery materials and battery tech firm Novonix [ASX:NVX] is up ~15% in late afternoon trade after finalising a US$100 million grant award from the US Department of Energy.

The finalised grant is slated to expand NVX’s production of synthetic graphite anode materials at its Riverside facility in Tennessee.

As part of the deal, Novonix must match the US$100 million, meaning it has to fork up around $160 million to expand the facility.

As of the end of September, NVX had US$88 million cash on hand.

Interestingly, Novonix was initially considered for a DOE grant of US$150 million to build a new synthetic graphite manufacturing facility with a starting output of 30,000 tonnes per annum.

After negotiations with the DOE, Novonix ‘reallocated the funding more immediately to its Riverside facility which has a target production of up to 20,000tpa and, accordingly, resized the award to US$100 million.’

Did it voluntarily ‘resize’ the award by asking the DOE for less, or did the DOE unilaterally offer less?

What are the emerging threats to financial stability?

Yesterday, RBA assistant governor Brad Jones addressed the Australian Finance Industry Association on ’emerging threats’ to financial stability.

Did Jones have anything interesting to say?

He certainly started with a bang, citing the ‘sardonic’ imprecation — ‘may you live in interesting times’.

Philip Lowe’s parting words to successor Michele Bullock, allegedly…

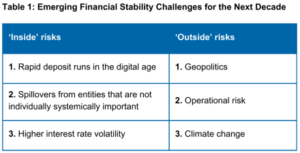

Anyway, Jones listed some ‘inside’ and ‘outside’ risks facing financial systems in the next decade.

The three that stood out:

- Rapid deposit runs in digital age (will the digital age make deposit runs easier?)

- Spillovers from entities ‘not individually systematically important’ but important once individual failures aggregate to a systematic problem?

- Climate change (malfunctioning insurance markets, falling commercial real estate, displacement?)

Bank runs in a millennial world

Jones noted that Silicon Valley Bank lost 30% of its deposit base in just a few hours and was slated to lose 50% more the following day.

‘In our current system,’ warned Jones, ‘any bank would struggle to survive a run of this magnitude’.

Any bank would struggle, but not any bank would be susceptible to a run like Silicon Valley Bank. Right?

Jones said:

‘Herding effects associated with social media present a new challenge for financial regulators. And it is clearly easier to withdraw deposits at the stroke of a keyboard than it is to stand for hours in the rain outside a bank branch and bury cash in the yard. But I see the role of technology here more as an amplification mechanism, not a root cause.’

Jones then made an interesting point about friction.

Friction in finance relates to transaction costs that impede or delay or hinder transactions.

Regulators and authorities seek to reduce this friction, like Zamboni trucks on ice rinks.

But sometimes, the lack of friction is a problem.

Here’s Jones explaining:

‘First, money can now flow out of institutions and markets with unprecedented speed in response to the rapid spread of information and misinformation, including that amplified through social media. In normal times, fewer frictions in the flow of money and information should lead to better economic outcomes – few advocate for the frictions and stale information of yesteryear. But the issue is more complex in periods of heightened stress. As noted by the Financial Stability Board in its recent review, the ubiquity of social media, combined with 24/7 access to banking and payment services and more globally connected trading platforms, raises the possibility that a shock somewhere in the financial system metastasizes into a broader self-fulfilling crisis of confidence.’

IMF: Australia needs higher interest rates

Michele Bullock and her predecessors have a tough job.

The whole country has an opinion on where rates should be. And now it’s international institutions, too.

The International Monetary Fund urged the Reserve Bank to lift the cash rate in its latest annual report on the Aussie economy.

Talk about presumption, Bullock and crew may be thinking.

The IMF said:

“Although inflation is gradually declining, it remains significantly above the RBA’s target and output remains above potential. Staff therefore recommend further monetary policy tightening to ensure that inflation comes back to the target range by 2025 and minimise the risk of de-anchoring inflation expectations.”

The IMF then recommended more coordination between Australia’s fiscal and monetary policy, something Philip Lowe mentioned in his last speech as governor.

If the Commonwealth government doesn’t take a measured approach to fiscal policy, the RBA may have to raise rates ‘even higher’:

‘In that context, continued coordination between monetary and fiscal policy is key to securing more equitable burden sharing. The Commonwealth Government and state and territory governments should implement public investment projects at a more measured and coordinated pace, given supply constraints, to alleviate inflationary pressures and support the RBA’s disinflation efforts. Otherwise, interest rates would have to be even higher, putting the burden of adjustment disproportionately on mortgage holders.

‘All levels of government need to improve expenditure outcomes and contain structural spending growth in health, aged care, and the NDIS. The new national wellbeing framework, designed to improve the quality of lives, can turn the focus on achieving better outcomes by fostering cooperation across different levels of governments.’

Living costs continue to rise: ABS

The ABS must be a warren of activity.

Each day a new data release.

Some days, of course, more important than others.

Today, the ABS released the latest living costs data, showing living costs for employee households rose 2% in the September quarter, up from the 1.5% rise in the June quarter.

Employee households’ living costs grew at almost twice the rate of the CPI, which rose 1.2% in the September quarter.

Growth in age pensioner living costs undershot the CPI in the quarter and in the last 12 months.

Employee households were severely affected by mortgage repayments. These repayments also explain away the difference with the CPI data, which excludes mortgage interest charges.

ABS’s Marquardt said:

‘Mortgage interest charges rose 9.3 per cent following a 9.8 per cent rise in the June 2023 quarter. While the Reserve Bank of Australia has not increased the cash rate since July 2023, previous interest rate increases and the rollover of some expired fixed-rate to higher-rate variable mortgages resulted in another strong rise this quarter.’

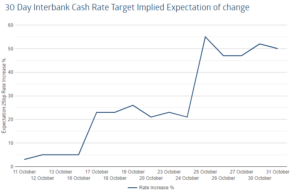

50/50 chance of rate hike next week

The market thinks there’s a 50/50 chance the RBA will raise the cash rate to 4.35% next week.

The probability of a 25bp hike has steadily risen this month.

The market is pricing in the RBA rate to peak at about 4.515% late next year, with the first cut not anticipated until November 2024.

‘Higher for longer’ and whatnot.

Bullock: rising house prices tend to result in higher consumption

More on the last post.

Our new RBA governor, Michelle Bullock, addressed the Commonwealth Bank Global Markets Conference last week.

There, she also fielded questions. Some of her answers addressed house prices.

Some snippets:

‘Housing prices are on the rise again and we know from history that rising housing prices tend to result in high consumption, so there’s that as well which is impacting things. So it is a balancing act and they’re the sorts of things we’ll be looking at, the inflation numbers obviously and our new set of forecasts.’

‘Household balance sheets on average, in aggregate, are actually pretty solid. They’ve still got lots of savings and they’re still saving. The savings rate in Australia is still positive. So, they’ve got lots of buffers, lots of saving. We are seeing housing prices rising again, so wealth is rising again, so household balance sheets in that respect are solid.’

Aussie home values expected to hit record high ‘within weeks’

Something caught my eye yesterday. An article from the Sydney Morning Herald.

Apparently, Aussie home values are set to reach a record high within weeks.

The latest CoreLogic home value index report showed national house values rose 0.9% in October. Since a low in January, house values are up 7.6% nationally.

CoreLogic’s research director Tim Lawless told the Herald only a further 0.5% rise in national home values is needed to set a new record.

Lawless thinks this is feasible by mid-November.

Will this play a role in the RBA’s upcoming rate decision?

Good day!

Good day, everyone!

It’s Kiryll, here. I’m back from a trip to London.

What a city it is!

Anyway…

There’s market news to get to. So let’s get to it.

(Hope you’re enjoying the new look of Fat Tail Daily, by the way).

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988