ASX News Live | ASX Trips Up; A2 Milk, Nuix, NIB, Adairs All Feature

Adairs posts record sales in 1H23 but margins soften

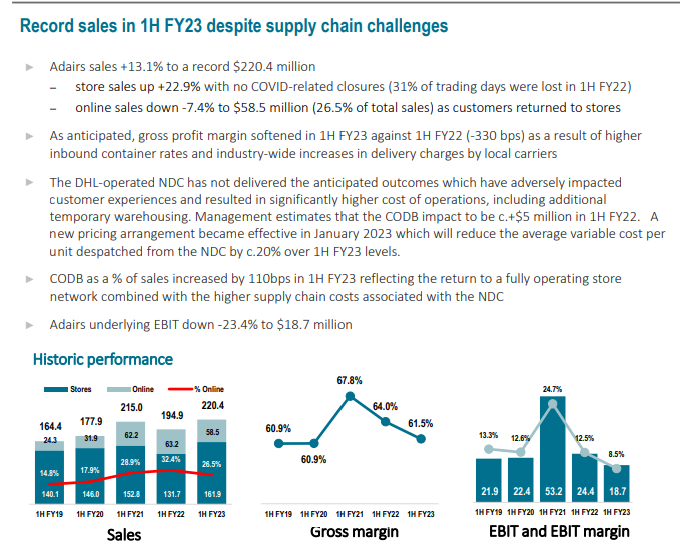

Home furnishings retailer Adairs (ASX:ADH) posted record sales in the six months to December 2022.

Sales rose 34% to $324.1 million while statutory net profit after tax rose 24% to $21.8 million. The strong performance led to an interim dividend of 8 cents a share.

However, gross margin did slip 330 basis points due to ‘higher inbound container rates and … delivery charges by local carriers.’

The core Adairs brand contributed sales growth of 13%, totalling $220.4 million.

One thing to note is that the prior corresponding period was impacted by store closures. Adairs lost 31% of trading days in 1H22 so the comparison was also bound to be favourable.

For instance, the core Adairs segment delivered total sales of $215 million in 1H21. Meaning the core segment’s sales grew 2.5% to 1H23.

Adairs said the gross profit margin of its core business was hurt by container rates and delivery chargers by local carriers like DHL.

Adairs singled out DHL for not delivering the ‘anticipated outcomes which have adversely impacted customer experiences’.

Source: Adairs

Adairs also saw a dip in sales in recent acquisition Mocka.

Mocka sales fell 27% on 1H22, with Mocka’s EBIT taking a 95% dive to $300,000 from $5.7 million.

Adairs commented on Mocka’s performance:

“Mocka sales fell -26.8% to $25.1 million as the brand resolved the operational issues of 2H FY22 and cleared excess inventory. The impact of customers returning to stores has been felt by most pure play online businesses with the impact on Mocka amplified by its operational issues.”

GPT: office property market remains challenging

$9 billion REIT GPT Group (ASX:GPT) reported a full year 2022 net profit after tax of $469.3 million, well down on a FY21 of $1.4 billion.

The sharp decline was attributed to ‘negative investment property movements’.

GPT also said that remote work is hurting demand for office space.

“The office leasing market remains challenging, with tenant demand being impacted by the adoption of hybrid work arrangements and the expectation of softer economic conditions. While the occupancy of our Office portfolio declined in the period due to a number of larger tenant expiries in the second half, we remain confident that our portfolio will benefit from the tenant flight to quality we are seeing in the market.”

GPT’s office portfolio occupancy fell from 92.9% to 87.9%, with 9% of its office portfolio lease income set to expire in 2023.

GPT also gave a downbeat outlook on the impact of rising interest rates on the property sector:

“Global economies including Australia are facing ongoing inflationary pressures and central banks including the Reserve Bank of Australia have raised interest rates materially over the past 12 months. The rise in interest rates has increased GPT’s cost of debt impacting the FFO outlook for the year ahead. GPT has 78% of its drawn debt hedged to reduce the exposure to further rate rises in 2023. The effect of rising bond yields is also observed in the slowing of investment capital flows and general economic uncertainty, increasing the potential for further softening of investment metrics adopted for valuations. Further tightening of monetary conditions is expected to moderate economic growth over the next 12 months.

“GPT’s Retail portfolio is well positioned with strong retail sales productivity, high occupancy, fixed rental increases and ongoing tenant demand. There has been a strong recovery in sales performance across GPT’s Retail portfolio in 2022, supporting tenant financial strength, buoyed by low unemployment and elevated levels of household savings. However, given the persistent rise in interest rates over the past 12 months and further increases expected, together with inflationary pressures on households, it is anticipated that retail sales growth will moderate during the course of 2023.”

Interest rates may have to stay high for longer if the real neutral rate rises

The natural — or neutral — rate of interest is the rate of interest compatible with a stable level of economic activity where the price level is constant.

It is the natural rate of interest that neither impedes nor stimulates the economy — the equilibrium rate, if you will.

The natural rate is important for central banks, who benchmark their interest rate decisions on the perceived real interest rate.

For instance, if the market rate is below the natural rate, it can excite the economy. Conversely, market rates above the natural rate can dampen activity.

Take the Dallas Fed explaining the importance of the neutral rate in monetary policy-making:

“The reason is that, despite the relatively wide confidence bands around these estimates [of the natural rate], they can provide an indication, albeit imperfect, of whether our monetary stance is accommodative, neutral or restrictive. Making a judgment on the stance of monetary policy is a key part of my job as a central banker.

“Monetary policy is accommodative when the federal funds rate is below the neutral rate. When this is the case, economic slack will tend to diminish—the economy will tend to grow faster, the unemployment rate should decline and inflation should tend to rise. When the federal funds rate is above the neutral rate, monetary policy is restrictive. When this is the case, economic slack will tend to increase—economic growth will tend to slow, the unemployment rate should tend to rise and the rate of inflation should be more muted or decline. The challenge for the Federal Reserve is managing this process and getting the balance right.”

For many years after the global financial crisis, the neutral rate was thought to be close to zero. Hence why many central banks followed the neutral rate down and lowered their official interest rates.

Now, however, questions are rising whether the neutral rate is getting up from the canvas and pushing well above zero.

In a research note released last week, a team at JPMorgan mused that the neutral rate may be rising, making it more difficult for central banks. And making it likelier that official interest rates will hover higher for longer.

The note states:

“We attribute the ineffectiveness of last decade’s low-for-long stances to powerful disinflationary forces unleashed by the GFC outside the control of central banks. Importantly, conditions have changed dramatically. In contrast to last decade’s post-GFC balance sheet adjustment and regulatory tightening, the pandemic and has improved private sector balance sheets and created pent-up demand. In addition, fiscal policy shocks during this cycle have generally been positive thus far, a radically different backdrop to the aggressive European and US tightening through the first half of the last expansion. Finally, the supply shocks related to the pandemic have altered the inflation process in a way that is likely raising short-term inflation risk premia. In all, these developments suggest that neutral policy rates have moved higher from estimates at the end of the last expansion.”

Interestingly, JPMorgan suggests that Australia’s own real neutral rate is well in the negative territory, meaning that the RBA may still have a while to go in its interest rate hikes.

The truth about nuclear power | Ryan Dinse

Today, 2.3 billion humans have to rely on cow dung for heating and cooking fuel. And three million people die annually because they can’t afford cleaner fuel.

Let’s be clear on this…

These will be the people that suffer the most if we try to move to renewables too fast and without a proper plan.

Germany has been the canary in the coalmine on this front.

But if you believe CO2 emissions are an imminent existential threat and we have no choice but to act now, what then?

Well, the only sensible answer is this: nuclear energy.

No single variable probably explains the rise in standards of living as energy.

You can see it very clearly here:

Long story short, we’re going to need more and more energy or condemn billions of people to poverty.

For example, for India to have the same standard of living a China, their energy consumption has to increase more than 400%.

And the only way we can do that in a fast enough timeline and in a ‘green’ way is nuclear.

Now, I’ve heard a lot of pushback saying nuclear is too expensive, too dangerous, and takes too long.

However, when you actually look at the data, you find the opposite is true.

https://www.moneymorning.com.au/20230220/the-truth-about-nuclear-power.html

Magnis Energy in trading halt following ‘material transaction’

Magnis Energy (ASX:MNS) is in a trading halt pending a further announcement regarding a ‘material transaction’.

Magnis owns a majority interest in iM3NY, a lithium-ion battery plant in New York.

Last week, MNS reported that the iM3NY hit a delay in its independent certification process after a test showed an ‘irregular result’ in one of the battery cells.

As a consequence, iM3NY had to start the certification process again with a new batch of cells.

While iM3NY waits for its independent certification, it is ‘stockpiling’ battery cells to ‘ensure delivery can occur in a timely manner’ for future customers.

Douugh rises 10% on Australian app launch

Small-cap fintech Douugh (ASX:DOU) is up 10% right now after launching its money management app in Australia.

At the moment, the app offers only micro-investing services, allowing customers to invest in diversified portfolios managed by BlackRock and ‘high-conviction single stocks like Tesla, Apple, Microsoft, and Disney’.

Douugh expects to make money through account, instant funding, foreign exchange fees, and interest on cash balances.

DOU says it offers ‘some of the lowest fees in the market with unlimited trading for … $2.99 per month’.

In its latest quarterly, Douugh reported just $31,000 in customer receipts, which were unsurprisingly dwarfed by staff, admin, and even marketing costs.

Cash outflows from operating activities totalled $1.9 million, with Douugh ending the December quarter with ~$3.4 million in cash and cash equivalents.

Were it not for the $1.9 million raised from equity issues, the fintech would have had about 1 quarter of funding available.

The low fees may be great for its customers … not so much for its bottom line.

In today’s release, Douugh said it has about $5.4 million in funds under management with 1,200 active customers on the platform.

a2 Milk says China still offers a ‘significant growth opportunity’

For a2 Milk, China loomed as the most lucrative market for a premium infant formula producer.

But after years of strong growth in the region, a2 Milk hit snags following the pandemic.

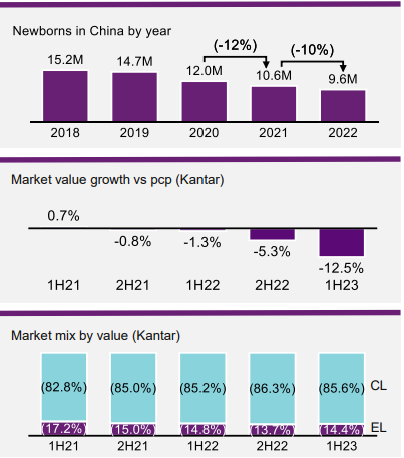

Its daigou channels were disrupted and local companies began to assert themselves. Not to mention China’s declining birth rate.

a2 Milk reported today that the number of births in China declined 10% in CY22 to 9.6 million.

As a result, the overall China infant milk formula market shrank 11% in volume and 12.5% in value in 1H23.

English label products declined more than the overall market, highlighting the shifts in consumer sentiment.

a2 Milk said daigou sales in the English label channels saw ‘significant declines’ of ~40% in 1H23.

Despite the ‘challenging’ conditions, A2M thinks China still presents a ‘significant growth opportunity’.

Source: a2 Milk

A2 Milk profit rises but shares slump

Baby formula merchant a2 Milk (ASX:A2M) is down 7% in early morning trade after the release of its 1H23 results.

A2 Milk categorised its half-year performance as strong, given the ‘very challenging market’.

1H23 result was in line with management’s expectations.

Revenue rose 18.6% to $783.3 million. Net profit after tax rose 22.1% to $68.5 million.

Importantly for the company, China & Other Asia sales rose 54%, despite Australian & New Zealand sales shrinking 24.6%.

Looking out, A2 Milk expects FY23 revenue to moderate, forecasting ‘low double-digit’ growth for the full year.

Management sees the EBITDA margin coming in at a ‘similar’ level to FY22.

Source: a2 Milk

Pilbara Minerals sells 15k worth of spodumene concentrate outside of BMX auction

Pilbara Minerals has eschewed selling a cargo of spodumene via its BMX platform auction after ‘receiving [a] strong offer from a chemical converter’.

PLS entered a sales arrangement for 15,000 tonnes of spodumene concentrate for delivery in the March quarter.

Pilbara said it was the ‘first sale of its kind’ for the producer, reflecting a new commercial model based on lithium hydroxide tolling.

Pilbara explained:

“The sale, which was made to a chemical converter, was structured to be based on a tolling arrangement under which Pilbara Minerals will receive the value of lithium hydroxide price for the product sold less an agreed amount for conversion and other costs. This is the first time Pilbara Minerals has utilised such a pricing methodology, which has the potential to be highly favourable to the Company and opens the door for future tolling arrangements.

“Under the terms of the agreement, based on today’s pricing for lithium hydroxide, pricing for the cargo would be aligned with previous spot sales including those achieved on the BMX platform. The actual price received for this cargo will however be calculated using future lithium hydroxide pricing at the time of conversion to lithium hydroxide.”

$PLS eschewed its BMX auction process to sell a 15k cargo of spodumene concentrate via a 'new commercial model based on lithium hydroxide tolling.' #ASX #lithium pic.twitter.com/ehK4vGz1IO

— Fat Tail Daily (@FatTailDaily) February 19, 2023

Lithium stocks tumble at the open

Lithium stocks are not starting the week well.

All the heavy hitters are down this morning — produces and juniors alike.

- Piedmont Lithium is down 13.5%

- Sayona Mining is down 4.7%

- Pilbara Minerals is down 4.5%

- Leo Lithium is down 4.4%

- Lake Resources is down 4%

- Ioneer is down 3.8%

- Allkem is down 3.5%

- Galan Lithium is down 3%

- Liontown Resources is down 2.2%

- Core Lithium is down 1%

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988