ASX News Live | ASX Rebounds; BHP, Ioneer, Smartpay, Santos Feature

IEA: Oil demand to hit record level in 2023 on China reopening

Oil demand could rise to record levels as China’s reopening surprises many by its swiftness, according to the latest International Energy Agency Oil Market Report (OMR).

The IEA estimates global oil demand will rise by 1.9 mb/d in 2023. China accounts for half the gain after loosening strict COVID-19 restrictions.

IEA expects a rise in global demand despite OECD demand falling by 900 kb/d in 4Q22 as ‘weak industrial activity and weather effects’ lowered use. Non-OECD use was 500 kb/d higher.

The IEA forecasts oil demand to reach 101.7 mb/d in 2023, the highest ever. But two ‘wild cards’ will dominate the narrative — China and Russia:

“Two wild cards dominate the 2023 oil market outlook: Russia and China. This year could see oil demand rise by 1.9 mb/d to reach 101.7 mb/d, the highest ever, tightening the balances as Russian supply slows under the full impact of sanctions. China will drive nearly half this global demand growth even as the shape and speed of its reopening remains uncertain.”

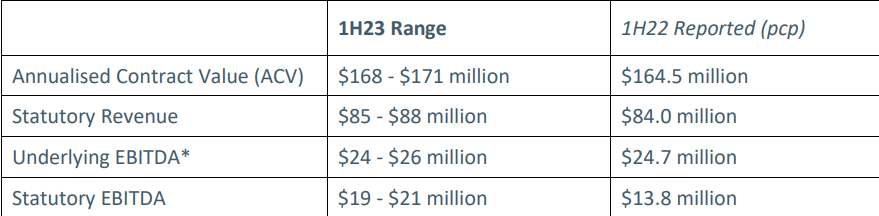

Nuix — the wisdom of underlying EBITDA

Nuix’s 1H23 trading update is the first time where underlying EBITDA is probably more telling than statutory EBITDA.

NXL shares closed 14.6% higher on a ‘materially higher’ expected statutory earnings.

But at a time where adjusted EBITDA figures are the preferred means to obfuscate rather than illuminate, underlying earnings may hold the greater insight in Nuix’s case.

While statutory EBITDA is expected to rise 50% on 1H22, underlying earnings — excluding legal and acquisition costs — are expected to inch 5% higher.

Nuix’s bread and butter income growth is modest.

Nuix one of ASX’s top performers on Thursday following ‘materially higher’ expected EBITDA

Data analytics firm Nuix is up 18% late on Thursday after a positive 1H23 trading update.

If we take Nuix at its word and use the top 1H23 guidance range, the expected 1H23 movement in the key metrics would be as follows:

- ACV up by ~4%

- Statutory revenue up by ~5%

- Underlying EBITDA up by ~5%

- Statutory EBITDA up by ~50%

Why the discrepancy between underlying and statutory EBITDA?

The former excludes legal costs, which were ‘significantly lower during the half compared to the prior period.’

However, Nuix did say that legal fees could spike in the second half, ‘potentially impacting both EBITDA and NPAT in 2H23’.

Nuix ended the half with $37.1 million in cash on hand. The data analytics firm was ‘cash flow neutral before non-operational legal costs and acquisition costs.

In 1H22, Nuix’s cash balance was $52.5 million, down from 1H21’s $70.9 million.

Miners are being forced outward to riskier jurisdictions as assets deplete

With lack of new discovery in established mining districts, companies are forced to explore for new ore in increasingly volatile ‘frontier’ locations.

In a stable, mining friendly jurisdiction with a skilled labour force, such as Australia, development could take around 10 years from discovery to first production.

Yet, mining companies are being forced outward and beyond.

Lack of discovery in established areas means a push into unstable regions.

What few people understand (outside the industry) is the added delays involved in establishing a mine in risky geopolitical environments.

For example, in 2010 when I was working for Barrick Gold [NYSE:GOLD], formally the world’s largest gold producer, the company was looking to develop an enormous copper-gold project on the border of Afghanistan and Pakistan.

At the time, the war in Afghanistan was at its peak. Geologists working on the project regularly watched US fighter jets flying overhead.

They suggested their drill rigs probably looked like enemy anti-aircraft missile to US fighter pilots streaming above.

But it wasn’t a wayward F-18 missile, lack of water, or extreme isolation causing ongoing delays…the real problem was the extreme bureaucracy of the Pakistani Government in allowing the project to proceed.

In what’s one of the world’s largest underdeveloped copper-gold projects, the Reko Diq deposit has now taken almost 20 years for development to proceed.

This is certainly not unusual and will be the future trend for mining as operators are forced into ‘frontier’ locations in an attempt to replace exhausted global reserves of critical metals.

It means a doubling in the development timeline in order to reach maiden production.

This should be the expectation of future supply, yet most analysts have failed to properly account the extreme timelines involved with project development in the new era of ‘frontier mining’.

Ageing operations located in established mining territories will struggle to meet normal demand over the near future. They have zero chance of reaching the energy transition goals set out by political leaders.

While investment in these new regions will be touted as the answer to supply shortages, leaders, economists, and those responsible for this energy transition mess have no first-hand experience of the extreme delays associated with mining in less than friendly jurisdictions.

Delays that can exceed 10 years or more!

We are very much opening a new chapter in human history…an age of scarcity.

You can’t eat an iPhone so embrace the ‘old economy’ — James Cooper

There’s been an enormous misalignment of capital over the last 10 years, focused solely on the ‘new economy’.

The scale of investment into the ‘new economy’ was exceptional.

The period from 2013–21 will perhaps be looked back on as one of history’s most ‘inflated’ bubbles…

At its culmination in early 2022, Apple’s [NASDAQ:AAPL] market cap was an astounding US$3 trillion.

At one point, the size of Apple was larger than 186 countries…only the US, China, Japan, and Germany were bigger.

It’s absurd to think that a single company making some pretty little ‘devices’ could be worth more than France, Italy, the UK, Australia, or Korea.

But that’s the scale of the bubble we’ve just had.

While resource companies have a bright future, I believe there’s much more pain on the way for tech.

You can’t eat iPhones

Let’s turn our attention to the future and the safest place to be investing…the ‘old economy’.

However important the latest iPhone model might appear to be, it doesn’t provide us with any of our basic human needs.

While investors are starting to wake up to their drunken obsession with tech, the makings of a resource crisis is already underway.

The global economy has assumed an endless supply of food, energy, and raw materials would continue indefinitely.

Europeans could soon discover the importance of energy security, not so much in the sense of recharging their smartphones, instead as a matter of life or death.

Northern Hemisphere winter storms are a threat to the sick and elderly in normal times, extreme gas shortages stemming from Russian aggression could threaten the health of vulnerable Europeans on a much larger scale.

But a day of reckoning is fast approaching for all consumers.

Our growing obsession with the latest trends means we’re placing a far greater burden on the planet in sucking out the supply of its critical resources.

Mindlessly replacing perfectly functional electronics with the latest iPhone, laptop, or TV, means we add more pressure to finite resources supposed to fuel the green energy transition.

The last 10 years or more have been mired by increasingly wasteful consumer habits, parents buying cheap plastic toys for their children, made in China, lasting little more than a week. At one point, kids were given quality wooden toys that would be passed through generations.

Knocking down solid brick houses for glass walled heat traps that need continuous artificial cooling in summer and warming in winter…more energy is the answer to extravagant architecture.

All this while the world’s population continues to add another one billion people each and every decade or so.

As Visual Capitalist points out, it took all human history until the year 1803 to reach the first one billion people.

Now, we add one billion people every 12 years!

It’s a sobering statistic if you ask me.

For too long we have lived incredibly wasteful lives, taking for granted the endless supply of materials, food, and energy.

All the while we have done this without securing future raw materials.

https://www.dailyreckoning.com.au/welcome-back-to-the-old-economy/2023/01/19/

Life at Twitter under Musk — code reviews, layoffs, and no toilet paper

This week, the New York Magazine published a cover story on life at Twitter under Musk and his cronies.

Twitter’s staff spent years trying to protect the platform against impulsive billionaires who wanted to use it for their own ends — then one made himself the CEO. @ZoeSchiffer , @CaseyNewton , and @alexeheath report, in collaboration with @verge https://t.co/Trw0ulxWeP pic.twitter.com/JWifgB7zzv

— New York Magazine (@NYMag) January 17, 2023

The whole piece is riveting.

Here are the best bits.

David Sacks, venture capitalist and satellite of Musk’s inner orbit, found himself at Twitter in the early days of Musk’s takeover. But according to the NY Mag, his help wasn’t always needed.

“Just then, David Sacks, a venture capitalist and friend of Musk’s who had advised him on the acquisition, walked into the room. A fellow native of South Africa, Sacks had worked with Musk at PayPal and later led the enterprise social-networking company Yammer to a $1.2 billion sale to Microsoft. “David, this meeting is too technical for you,” Musk said, waving his hand to dismiss Sacks. Wordlessly, Sacks turned and walked out, leaving the engineers — who had gotten little engagement from Musk on anything technical — slack-jawed. His imperiousness in the middle of a session he appeared to be botching was something to behold. (Musk did not respond to multiple requests for comment.)”

Sacks denies this account. Speaking to Business Insider, Sacks said:

“Elon has never kicked me out of a meeting. If anything, he is over-inclusive, and I opt in or out based on where I feel I can add value.”

The NY Mag story also covered Musk’s ‘fail fast’ Twitter experimentation and how it led to an advertiser exodus.

“Musk’s blundering left a deep scar. Twitter Blue was meant to begin shifting Twitter’s sales away from ads toward subscriptions. But while chasing a relatively paltry new cash stream, Musk torched the company’s ad business — the source of the vast majority of its billions in revenue. The Blue disaster accelerated a rush of advertisers abandoning the platform, including Eli Lilly, and by December, what was left of Twitter’s sales team began offering hundreds of thousands of dollars in free ad spend to lure back marketers. (It did not work.) In a series of tweets, Musk blamed the company’s “massive drop in revenue” on “activist groups pressuring advertisers.” To Musk, it was anyone’s fault but his own.”

Yesterday, by the way, tech news site Platformer reported that Twitter’s revenues are down 40% year on year.

There was also a poignant section on how Musk dealt with his own supporters at Twitter.

“Twitter might have had a reputation as a left-leaning workforce, but there had always been a faction that disapproved of its progressive ideals. On Slack, some of these workers had formed a channel called #i-dissent, where they asked questions like why deadnaming a trans colleague was considered “bad.” When Musk announced he was buying the company, one of the more active i-dissenters was thrilled. “Elon’s my new boss and I’m stoked!” he wrote on Linked-In. “I decided to send him a slack message. I figured you miss 100% of the shots you don’t make 😅 🚀 🌕.” This employee was cut during the first round of layoffs. Soon, all the prominent members of the #i-dissent Slack channel would be gone. The channel itself was archived, while bigger social channels like #social-watercooler were abandoned.”

And who could forget Musk’s cost-cutting measures extending to ‘porcelain thrones’?

“Meanwhile, more staff deemed non-essential were let go. In London, receptionists were fired just before the holiday. In San Francisco, the janitorial staff was laid off without severance. At one point, the San Francisco office got so low on office supplies that employees began bringing their own toilet paper.”

At least 50% of my tweets were made on a porcelain throne

— Elon Musk (@elonmusk) November 22, 2021

The Twitter saga is unlikely to end anytime soon. Even though Musk has fired much of Twitter’s workforce, it can continue to cost him:

“The repercussions for Musk’s handling of Twitter are now coming. According to his public-merger agreement and internal Twitter documents, Musk agreed to at least match the company’s existing severance package, which offered two months of pay as well as other valuable benefits. Instead, he laid off employees with the minimum notice required by federal and state law and refused to pay out certain awards. Now more than 500 employees, with Shevat among the highest ranking, are pursuing legal action against Musk for what they are owed, in addition to his alleged discrimination against minority groups in his handling of the layoffs.

Originally, laid-off employees were given a 60-day notice. Now that it is up, they are receiving severance agreements asking them to sign away their right to sue Twitter or say anything negative about the company or Musk for life. In exchange, they get one month of pay before they need to find another job during what is the most difficult hiring market in tech in years.”

The thorny oil problem that could fuel the ‘Big Loss’

US shale oil could be key to markets in 2023. For better or worse, this lucrative source of oil and gas appears to be reaching its end.

Cast your mind back to 2008…

Back when the world was gripped by the global financial crisis that wrought so much investor pain. Because, as bad as it was, it could’ve been far worse…

See, in the aftermath of the meltdown, a US oil and gas revolution likely saved the global economy. Shale oil or ‘fracking,’ as it would eventually be known as, helped turn the US into the world’s largest oil producer.

As a result, the stranglehold over oil production and pricing from OPEC was somewhat disrupted. The cartel couldn’t completely dictate the market now that a new free-market competitor had come into the mix.

There is little doubt that this ensured the rebound to growth following the GFC was far faster than it would’ve been otherwise. Because with an abundant supply of new oil and gas, global production could return without the burden of higher costs.

Shale oil has been a key factor, if not the key factor, in the 15-year-long boom we’ve seen since 2008.

Even with some rocky patches in between, if it weren’t for US oil and gas, things would almost certainly be very different for markets and investors. This is why, now that the shale industry is beginning to slow down, one has to wonder what the consequences might be…

The data shows that shale output may have passed its peak. Just take a look at these charts:

Source: Financial Times

In our post-pandemic era, it seems US production is finally falling. Not by all that much yet, but it is still heading in the wrong direction for anyone who relies on oil and gas.

https://www.moneymorning.com.au/20230119/the-big-oil-problem-that-could-fuel-the-big-loss.html

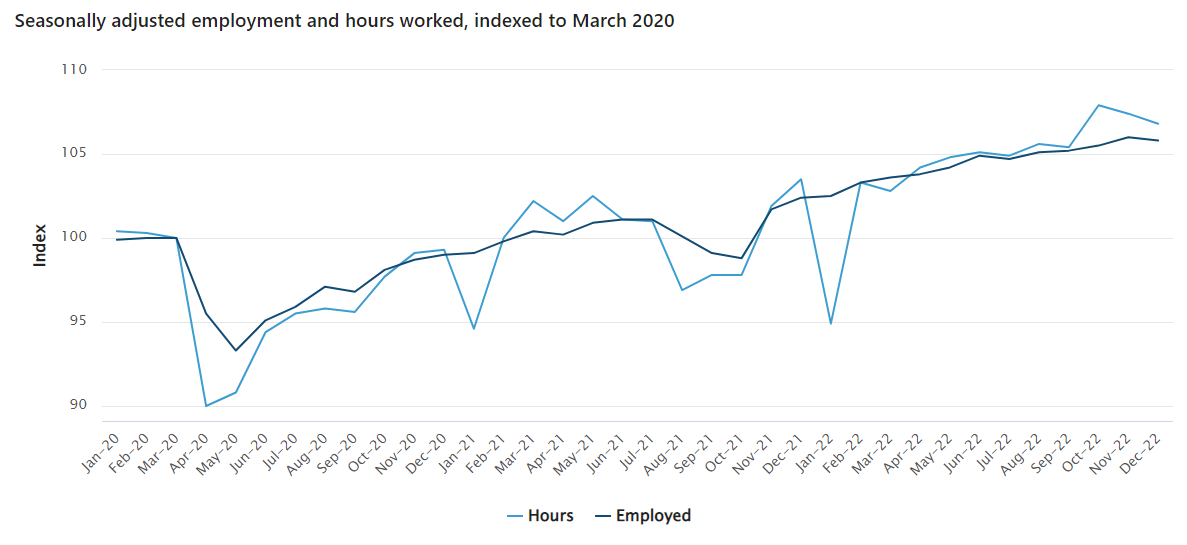

Jobs data weaker than expected

The seasonally adjusted unemployment rate remained at 3.5% in December, in line with November, in the latest release from the Australian Bureau of Statistics.

Employment fell by 15,000 people. The unemployed rose by 6,000 people.

That came in weaker than expected. Consensus forecasts had 25,000 jobs being added at 3.4% unemployment rate.

Lauren Ford, head of labour statistics at the ABS, said:

“The falls in employment and hours worked in December followed strong growth through 2022, with an annual employment growth rate of 3.4 per cent and hours worked increasing by 3.2 per cent.

The strong employment growth through 2022, along with high participation and low unemployment, continues to reflect a tight labour market. Even though hours worked grew during 2022, there continued to be more people than usual working reduced hours due to illness.

In December, we saw the number of people working reduced hours due to illness increasing by 86,000 to 606,000, which is over 50 per cent higher than we would usually see at this time of the year.”

Source: ABS

Crypto broker Genesis to file for bankruptcy

Prominent cryptocurrency broker Genesis is preparing to file for bankruptcy as soon as this week, according to reports from the Financial Times.

Genesis owes creditors over US$3 billion, including US$900 million to customers of big crypto exchange Gemini.

As FT reported:

Genesis and its owner, SoftBank-backed crypto conglomerate Digital Currency Group, have been in negotiations with creditors since mid-November. Genesis owes creditors more than $3bn, the Financial Times previously reported, including $900mn to customers of Gemini, the crypto exchange of Cameron and Tyler Winklevoss, and €280mn to Dutch exchange Bitvavo.

A pre-packaged bankruptcy deal for Genesis is being negotiated with creditors and would include cash and equity in DCG, one of the people said. It could be finalised as soon as this week. Genesis and DCG did not immediately respond to requests for comment. Genesis’ troubles began soon after the collapse of FTX. The company, which was one of the biggest lenders in the crypto market, halted customer withdrawals citing “unprecedented market turmoil” and liquidity issues.

It has since been scrambling unsuccessfully to find fresh funding. Negotiations with creditors burst into public this month after Cameron Winklevoss called for DCG’s board to sack its chief executive, Barry Silbert, accusing him of bad faith tactics in negotiations with creditors. Winklevoss’ exchange, Gemini, used Genesis as its main lending partner on a crypto “earn” programme that gave retail investors high yields in return for lending out their coins. A Genesis bankruptcy would be a significant blow for Silbert’s crypto group, which includes trade publication CoinDesk and asset manager Grayscale.

Allkem: lithium market remains tight

Speaking of lithium, large Aussie producer Allkem provided an update on the state of the lithium market.

Demand for lithium chemicals remained ‘strong’ in the December quarter, with published lithium prices ‘reaching new record highs’, although they have recently cooled.

EV sales ticked over nicely, too. Allkem reported that Chinese EV sales in the December quarter hit 2.3 million units, a 82% YoY increase.

Global EV sales could reach over 14 million units in 2023.

As for supply, Allkem believes the market remains tight despite lithium chemical production in China up 14% QoQ. Spodumene concentrate volumes shipped to China from Australian for October and November 2022 were 23% higher than the prior corresponding period. More supply came from brownfield expansions and restarted idle capacity.

Still, AKE thinks the market isn’t reaching equilibrium just yet:

Despite this increase, the spodumene concentrate market remains tight with limited material available to the open market due to the majority of the product already being locked under existing offtake arrangements or allocated for internal consumption by integrated producers.

4 of the 15 most shorted ASX stocks are lithium stocks

Lithium stocks — disparagingly colloqualised as liffium stocks by Australian fintwitter — were some of the best performing stocks on the All Ords a few years ago.

Now they are some of the most popular targets for shorters.

4 of the 15 most shorted ASX stocks last week were lithium stocks.

- Sayona Mining, with 9.9% short interest

- Core Lithium, with 8.9% short interest

- Lake Resources, with 7.5% short interest

- Vulcan Energy, with 6.4% short interest

Other highly shorted lithium stocks were Liontown Resources with 6% and Novonix with 5.4% .

4 of the 15 most shorted #ASX stocks last week were #lithium stocks.

🔴 $SYA with 9.9% short interest

🔴 $CXO, with 8.9% short interest

🔴 $LKE, with 7.5% short interest

🔴 $VUL, with 6.4% short interestOther shorted lithium stocks were $LTR with 6% and $NVX with 5.4% .

— Fat Tail Daily (@FatTailDaily) January 18, 2023

City Chic opens 13% higher on ‘Blundy bump’

Struggling women’s apparel retailer City Chic continued yesterday’s rally this morning, opening 13% higher after it was revealed that billionaire retail mogul Brett Blundy accumulated a 7.3% stake in the company.

City Chic finished 16% higher on Wednesday — despite at one stage being down as much as 9% — after City Chic’s disclosure documents showed Blundy’s large position.

Blundy is a big name in Australian retail, finding success backing names like Lovisa, Bras N Things, and Honey Burdette.

Despite the ‘Blundy bump’, CCX shares are still down 85% over the past 12 months.

Last week, 3% of City Chic’s shares were held short. Will Blundy’s involvement see the short interest shrink?

ASX opens 0.10% lower

The S&P/ASX 200 opened 0.10% lower.

The biggest decliners at the open:

- Netwealth, down 7.5% following the release of its December quarterly

- Nickel Industries, down 6.5% following the completion of a $264 million institutional placement at $1.02 a share

- Paladin Energy, down 6.4% following the release of its December quarterly

- Alumina, down 5.5% on the release of its fourth quarter earnings

Nanosonics was the only stand-out advancer at the open, rising 10% on higher profit and revenues for 1H23 and a revised outlook.

Only the paranoid survive … and Microsoft aims to survive and thrive

In Microsoft CEO’s memo to staff announcing lay-offs, you could hear the echoes of Intel founder Andy Grove and academic Clayton Christensen about disruptive innovation.

Satya Nadella wrote in the memo that Microsoft must continue to adapt if it wants to remain a ‘consequential company’:

“We are allocating both our capital and talent to areas of secular growth and long-term competitiveness for the company, while divesting in other areas. These are the kinds of hard choices we have made throughout our 47-year history to remain a consequential company in this industry that is unforgiving to anyone who doesn’t adapt to platform shifts.”

In the fast moving tech sector, you adapt or you perish. In Grove’s pithy slogan — only the paranoid survive.

This was formally consolidated by academic Clayton Christensen in his now-famous book The Innovator’s Dilemma. The dilemma lies in the fact that great companies can nevertheless fail by neglecting to position for emerging trends that can upend their industries.

As Christensen wrote in the book:

Simply put, when the best firms succeeded, they did so because they listened responsively to their customers and invested aggressively in the technology, products, and manufacturing capabilities that satisfied their customers’ next-generation needs. But, paradoxically, when the best firms subsequently failed, it was for the same reasons—they listened responsively to their customers and invested aggressively in the technology, products, and manufacturing capabilities that satisfied their customers’ next generation needs. This is one of the innovator’s dilemmas: Blindly following the maxim that good managers should keep close to their customers can sometimes be a fatal mistake.

The question in all this is how does this entrepreneurial paranoia relate to job cuts?

Cutting staff is usually a cost management issue, not an innovation issue. Or does Nadella’s memo imply that the employees let go are those in departments Microsoft thinks don’t have a ‘secular growth’ future?

Microsoft joins tech peers in announcing lay-offs

Even Microsoft isn’t immune to cost pressures. The tech giant intends to retrench 5% of its workforce or about 10,000 employees.

The cull is a tacit admission of miscalculation on the part of Microsoft CEO Satya Nadella, who signed off on a big recruitment push last year thinking customers will still splurge on technology despite rising inflation.

In a memo to staff yesterday, Nadella was more circumspect:

“First, as we saw customers accelerate their digital spend during the pandemic, we’re now seeing them optimize their digital spend to do more with less. We’re also seeing organizations in every industry and geography exercise caution as some parts of the world are in a recession and other parts are anticipating one.

First, we will align our cost structure with our revenue and where we see customer demand. Today, we are making changes that will result in the reduction of our overall workforce by 10,000 jobs through the end of FY23 Q3. This represents less than 5 percent of our total employee base, with some notifications happening today. It’s important to note that while we are eliminating roles in some areas, we will continue to hire in key strategic areas. We know this is a challenging time for each person impacted. The senior leadership team and I are committed that as we go through this process, we will do so in the most thoughtful and transparent way possible.”

Nadella did write that Microsoft will still continue to invest in ‘strategic areas for our future’.

“We will continue to invest in strategic areas for our future, meaning we are allocating both our capital and talent to areas of secular growth and long-term competitiveness for the company, while divesting in other areas. These are the kinds of hard choices we have made throughout our 47-year history to remain a consequential company in this industry that is unforgiving to anyone who doesn’t adapt to platform shifts. As such, we are taking a $1.2 billion charge in Q2 related to severance costs, changes to our hardware portfolio, and the cost of lease consolidation as we create higher density across our workspaces.”

While Microsoft is taking a US$1.2 billion charge in Q2 related to the planned staff cuts, the tech giant is mulling a US$10 billion investment in OpenAI, a trending AI research group gone viral for its ChatGPT product.

$MSFT intends to retrench 5% of its workforce as Big Tech's long summer winds down. #Microsoft's CEO Satya Nadella addressed staff in a memo you can read below. https://t.co/xaahTx6O65

— Fat Tail Daily (@FatTailDaily) January 18, 2023

ASX to open lower … and a robot lends a helping hand

Good morning!

It is shaping up to be a volatile day for the ASX. Aussie stocks are expected to open lower on Thursday following US market action overnight.

All three US indexes finished Wednesday down at least 1%.

- The S&P 500 finished 1.6% lower, with all 11 sectors down

- The Dow finished 1.8% lower

- And the Nasdaq fell 1.2%

If market data is making your eyes glaze over, here’s something a little different.

You may find it amusing — or ominous.

Boston Dynamics, a robot research lab ‘changing your idea of what robots can do’, has just dropped a video showcasing the latest capabilities of Atlas — its bipedal automaton.

Atlas can run, jump — and solve problems.

Hooray?

It’s time for Atlas to pick up a new set of skills and get hands on. pic.twitter.com/osOWiiBlSh

— Boston Dynamics (@BostonDynamics) January 18, 2023

Footer

Fat Tail Daily is brought to you by the team at Fat Tail Investment Research

Copyright © 2026 Fat Tail Daily | ACN: 117 765 009 / ABN: 33 117 765 009 / ASFL: 323 988